Contract Manufacturer Insurance

What Co-Packers and Contract Manufacturers Need to Know Before a Recall or Claim

You manufacture it. They brand it. When something goes wrong, both companies get named in the lawsuit.

Most co-packers carry standard manufacturing policies that were never built for contract or private-label work. At The Coyle Group, we structure contract manufacturer insurance programs around the real risks: product liability exposure across client relationships, client-owned goods in your facility, contamination events you did not cause, and co-packing agreement requirements that most insurers have never seen.

Ready to close the gaps?

“We thought our general liability covered everything.” That is the phrase contract manufacturers use after their first claim denial.

You spend years building client relationships, refining your production process, and delivering consistent quality for brands you helped launch. Then a contamination issue traces back to your facility, or a product recall sweeps up goods bearing another company’s label that you produced, and your insurer informs you that the claim falls outside your policy.

Contract manufacturer insurance is not a generic product. It requires a specific structure that accounts for who owns the product, who designed the formula, and who bears liability at each stage of the co-packing relationship.

Why Standard Manufacturing Insurance Leaves Contract Manufacturers Exposed

Standard manufacturing insurance does not cover co-packing operations the way most business owners assume, because the underwriting model is built for manufacturers selling their own branded goods, not for businesses producing goods under contract for other brands. The liability structure is fundamentally different, and a policy written for one will leave critical gaps in the other.

The financial consequence is not hypothetical: a joint study by Food Marketing Institute and the group now known as the Consumer Brands Association found the average cost of a food recall exceeds $10 million in direct costs alone, excluding third-party retailer penalties and lost client revenue.

Standard manufacturing policies are underwritten with one core assumption: the insured owns, manufactures, and sells the finished product under their own brand. That assumption creates these specific exclusions for co-packers:

If you co-pack food, personal care products, dietary supplements, nutraceuticals, or any consumer goods, the gap between what your policy says it covers and what it actually pays out in a co-packing claim can determine whether your business survives a recall.

Concerned about your current coverage? Contact The Coyle Group for a gap analysis.

What Is Contract Manufacturer Insurance?

Contract manufacturer insurance is a tailored commercial insurance program that protects businesses producing goods under contract for another brand. It covers your liability as the producing party and accounts for the unique risk-sharing structure of co-packing: you own the process, the client owns the formula, the retailer trusts both parties, and a court can name all three when something goes wrong. This coverage category also applies directly to co-packer insurance; the terms are used interchangeably depending on industry.

“Co-packer insurance” is the common term in the food and beverage, personal care, and dietary supplement industries. “Contract manufacturer insurance” is used more broadly across pharmaceuticals, electronics, consumer goods, and industrial products. Both describe the same underlying need: an insurance program structured for the risk of producing goods on behalf of another brand, where liability does not follow a simple chain of ownership.

Not every co-packing operation requires the same program depth. A sole proprietor producing small batches for one local brand under a simple service agreement carries a different risk profile than a 50-employee facility co-packing for five national accounts. The size of your client base, the contractual requirements in your agreements, and the product categories you produce are the three factors that determine which coverages are essential and which can be scaled.

Key characteristics that define a properly built contract manufacturer insurance program:

The 7 Coverages Every Contract Manufacturer and Co-Packer Needs

A complete co-packer insurance program includes all of the following. Some are standard commercial lines; others require specific endorsements or standalone policies that most generalist brokers overlook when placing manufacturing accounts for the first time. The coverage types, limits, and triggers vary significantly based on your product category, client base, and co-packing agreement requirements.

1. General Liability with Products and Completed Operations

General liability is the foundation of any commercial insurance program. For contract manufacturers, the products and completed operations extension is the critical element: it covers harm caused by goods you produced after they leave your facility. The policy language must explicitly cover products manufactured under contract for other brands.

one question your broker must answer before you bind or renew:

Whether your products liability is written on an occurrence basis or a claims-made basis. Products liability is almost always written on an occurrence basis, but claims-made forms exist, and the difference matters. Occurrence policies cover claims arising from events during the policy period, regardless of when the claim is filed. Claims-made policies only respond if both the event and the claim occur while the policy is active, which means the retroactive date matters enormously. If you switch carriers under a claims-made program without the correct retroactive date, you can be exposed for every product you manufactured before the new policy’s effective date.

2. Product Recall Insurance

Product recall insurance is a standalone policy type, not an add-on to general liability. It is the coverage most contract manufacturers do not carry and most urgently need. A properly structured product recall policy for co-packers covers:

The Insurance Information Institute is clear on this point: product liability insurance and product recall insurance are distinct coverages that serve different purposes. One responds to the legal claim after harm occurs. The other covers the logistical and financial cost of removing product from the market. Without both, a co-packer is exposed on two separate fronts.

3. Cyber Liability Insurance

Contract manufacturers operate production control systems, ERP platforms, and connected equipment that are prime targets for ransomware and data breaches. A network attack that shuts down your production line is not covered by your commercial property policy, it requires separate cyber liability coverage.

For food and beverage co-packers, the risk runs deeper than downtime. Under FDA’s FSMA Preventive Controls rule, food facilities must maintain written food safety plans, hazard analysis records, and verification records available for FDA inspection on demand. A ransomware attack that destroys those records puts you out of compliance before an inspector arrives.

A properly structured cyber liability policy for a contract manufacturer covers:

Your broker must confirm that third-party data liability, covering client-owned formulas and specifications in your systems, is explicitly included. Most standard cyber policies do not contemplate this exposure for co-packers.

4. Commercial Property Insurance

Commercial property coverage protects your building, production equipment, and inventory. For contract manufacturers, the policy must be structured to account for:

5. Bailee Coverage (Inland Marine)

Bailee coverage protects property belonging to others that is in your care, custody, or control. For co-packers, that means client-owned raw materials and ingredients delivered to your facility, client-owned proprietary packaging and labels, and client-owned finished goods awaiting pickup or shipment. Standard commercial property policies sharply limit coverage for third-party property.

Inland marine policies with a bailee endorsement close this gap directly.

6. Workers’ Compensation

Workers’ compensation is required in virtually every state for businesses with employees. Manufacturing operations carry above-average workers’ compensation risk due to equipment exposure, chemical handling, repetitive motion, and slip-and-fall hazards in production environments. Accurate classification of production employees is critical: errors in class codes can result in audit-driven premium adjustments after a claim. A broker with manufacturing experience will review your class code assignments, not just accept what the prior carrier assigned.

7. Umbrella and Excess Liability

Co-packing agreements from major retailers and national brands routinely require $5 million or $10 million in total liability limits. An umbrella policy sits above your general liability, products liability, and employer’s liability to provide those higher limits at a fraction of the cost of raising each underlying policy individually. If your co-packing clients are mid-market or larger, an umbrella is not optional: it is a contract requirement.

Not sure if your limits meet your client’s requirements? Book a call and we will review your agreements.

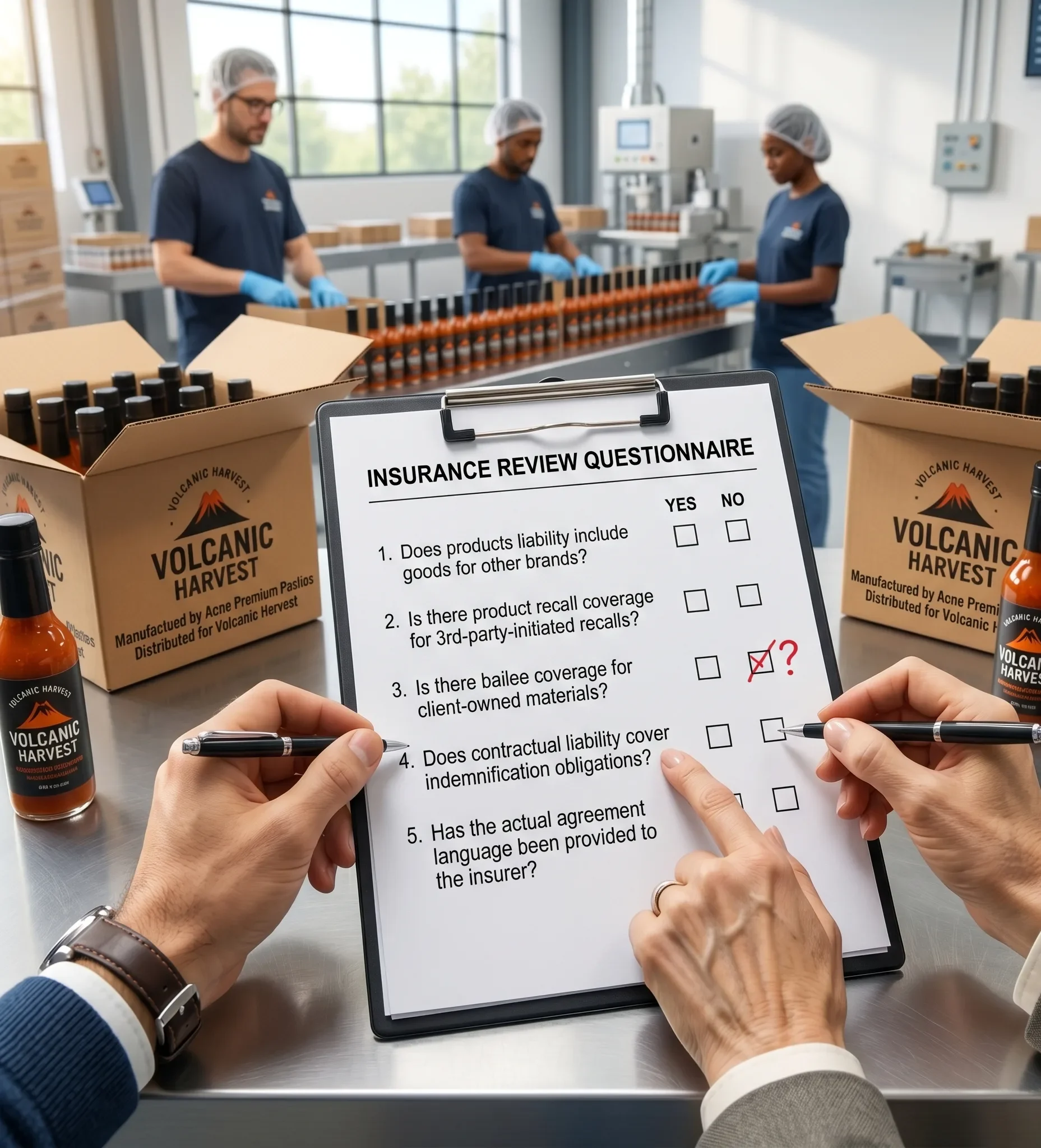

What Contract Manufacturer Insurance Does NOT Cover

A well-structured co-packer insurance program covers a lot of ground. But knowing the exclusions is just as important as knowing the coverages. Standard exclusions that appear across most contract manufacturer insurance programs are predictable, but only if you know to look for them before binding coverage. Standard exclusions include the following:

These exclusions are why the underwriting process matters. A specialist broker who understands co-packing will ask the right questions upfront and structure your program so that exclusions do not create gaps in the coverage areas most likely to generate claims.

What Co-Packing Agreements Actually Require from Your Insurance Program

Most contract manufacturers focus on coverage types and premiums when buying insurance. Their clients are focused on contractual compliance. A certificate of insurance that does not match the requirements spelled out in your co-packing agreement can delay contract execution, trigger a notice of default, or leave you personally liable under an indemnification clause you never fully read. These are the specific insurance provisions that appear routinely in co-packing agreements from national brands and major retailers.

Additional Insured Status

Your client (the brand) will require that they are named as an additional insured on your general liability and products liability policy. This means if a consumer sues the brand for a defect that originated in your production, the brand can access your insurance directly. Not every insurer grants additional insured status for contract manufacturing relationships without a specific endorsement request.

Primary and Non-Contributory Language

The brand’s legal team will require that your coverage responds first, before any policy the brand carries. A standard additional insured endorsement does not include primary and non-contributory language automatically. It must be specifically added and confirmed on your certificate of insurance.

Waiver of Subrogation

After your insurer pays a claim, they normally have the right to pursue the party responsible for the underlying loss. Co-packing agreements require you to waive that right against the brand. This must be endorsed onto your policy and reflected on your COI.

Indemnification Clauses

Most co-packing agreements include mutual indemnification: you indemnify the brand for manufacturing defects and contamination events; they indemnify you for formula and label claims. Your contractual liability coverage must be structured to respond to these indemnification obligations. Standard general liability excludes many categories of assumed contractual liability unless specific coverage is added.

Certificate of Insurance (COI) Requirements

Brands, retailers, and distributors request annual COIs showing all of the above. COIs must reflect actual policy endorsements, not generic descriptions.

Review your co-packing agreement with The Coyle Group.

How Much Does Contract Manufacturer Insurance Cost?

Contract manufacturer insurance cost depends on your revenue, the products you produce, your claims history, the number of co-packing clients you serve, and the specific coverage types and limits your agreements require. A food co-packer with $3 million in annual revenue producing for five clients will pay a different premium than a pharmaceutical contract manufacturer with $20 million in revenue and a prior recall. Understanding the cost structure helps you make informed decisions about where to invest coverage dollars.

General cost factors:

Factor |

Impact on Premium |

|---|---|

|

Annual revenue |

Higher revenue increases the premium base across all lines |

|

Product category |

Food, pharma, and personal care carry higher product risk ratings |

|

Prior claims or recalls |

History of claims increases cost significantly across all lines |

|

Number of co-packing clients |

More clients = broader products liability exposure |

|

Product recall and contamination coverage |

Typically adds $5,000 to $25,000+ annually depending on revenue and product risk |

|

Umbrella limits |

A $5M umbrella typically adds $3,000 to $8,000+ for most manufacturing accounts |

|

Bailee coverage limits |

Depends on the maximum value of client-owned property in your facility at any time |

What Drives Product Recall Insurance Premium Specifically

Product recall insurance is priced separately from your general liability and property program.

Underwriters evaluate:

What You Should NOT Do on Price

Do not strip product recall coverage, bailee coverage, or contamination coverage to reduce premium. These are the three lines most specific to co-packing risk and the three most likely to respond in an actual loss event. Reducing limits on your umbrella to save a few thousand dollars per year while carrying $10 million in contractual exposure to a national brand client is the wrong trade-off.

Real-World Scenario: What a Coverage Gap Looks Like

The financial exposure in a co-packing coverage gap is not theoretical. The combination of a contamination trigger, client-owned property, and a missing recall policy can create a six-figure uninsured loss from a single event. A real-world example illustrates how this happens and what the premium difference would have cost.

Situation

A food co-packer producing private-label sauces for three regional brands received a recall notice after a contamination issue traced back to one client’s formula specifications. The co-packer’s general liability policy excluded contaminated products claims. Their commercial property policy did not cover the client’s ingredients destroyed during the recall. They carried no product recall insurance. Out-of-pocket exposure exceeded $340,000.

What a properly built program would have done

A co-packer insurance program with contaminated products coverage, product recall insurance, and bailee inland marine would have transferred the majority of that loss to the insurer. The total annual premium difference between what they carried and what they needed was approximately $8,400.

What to Look for When Choosing a Broker for Contract Manufacturer Insurance

Most commercial insurance brokers have never placed a dedicated co-packer insurance program. They know how to write a standard manufacturers package, but the specific endorsements, standalone recall policies, bailee provisions, and contractual liability structures that a co-packing account requires are outside their daily experience. Choosing the wrong broker is the first step toward being underinsured.

When evaluating a broker for contract manufacturer insurance, ask these questions directly:

How to Evaluate Whether Your Current Coverage Is Built for Co-Packing

If you currently carry a standard manufacturers package or BOP, these are the questions to ask your broker before your next renewal or before signing your next co-packing agreement. If your broker cannot answer each of these specifically, that is a signal that your program was not built for co-packing operations.

Contact The Coyle Group with your current declarations pages and one co-packing agreement. We will identify the gaps in one call.

Frequently Asked Questions About Contract Manufacturer Insurance

Get the Right Coverage for Your Contract Manufacturing Business

Contract manufacturer insurance is not a commodity purchase. The right program requires a broker who understands co-packing operations, can read your co-packing agreements, and has placed recall and contamination coverage for businesses like yours.

The Coyle Group has structured insurance programs for contract manufacturers, food co-packers, dietary supplement manufacturers, and private-label producers across the US. Our approach starts with your agreements, not a generic application.

Contact us with your current declarations pages and one co-packing agreement. We will identify every gap in one call.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?