Here’s something most business owners don’t realize: when a customer sues you for discrimination or harassment, your regular business insurance probably won’t cover it. That’s where third party employment practices liability insurance comes in, and trust me, it’s protection you don’t want to be without.

I’ve seen too many businesses get blindsided by customer discrimination lawsuit protection gaps. You might think your employment practices liability insurance (EPLI) has you covered, but here’s the thing: most policies only protect you from employee claims, not non-employee harassment claims, or insurance from customers, vendors, or clients.

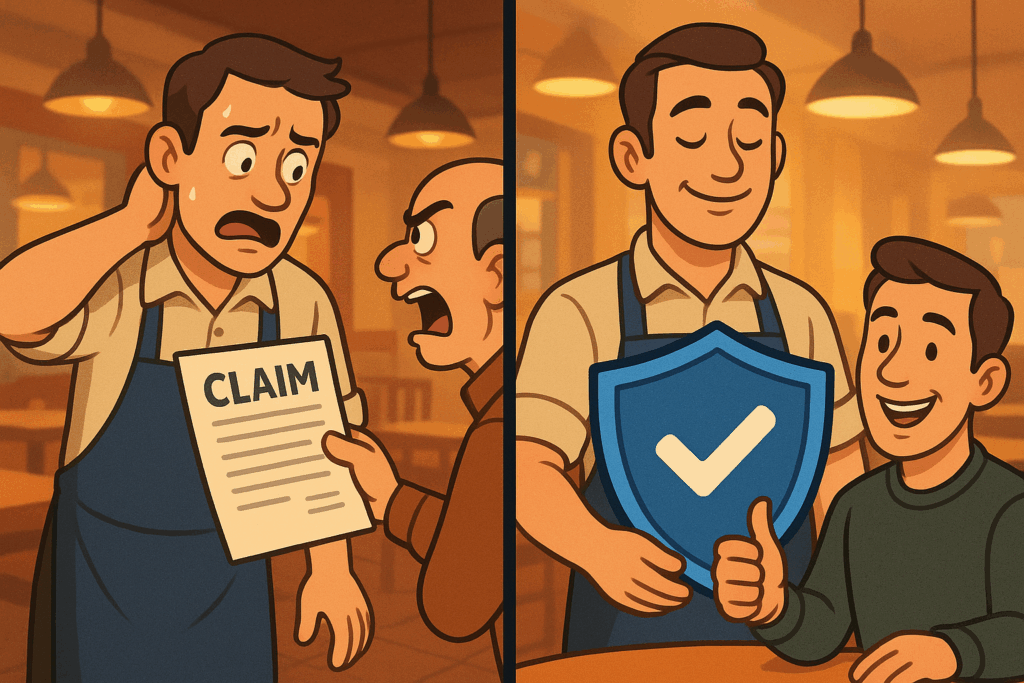

Let’s say a customer feels discriminated against by one of your employees. They decide to sue. Without third party EPLI coverage, you’re looking at potentially massive legal bills and settlement costs, all coming out of your pocket.

Essentials of Third party employment practices liability insurance

- Third party employment practices liability insurance covers claims by customers, vendors, and other non-employees

- Your standard EPLI and general liability policies probably exclude these external discrimination claims

- If you deal with customers regularly, you really need this protection

- You can add third party endorsement EPLI to your existing policies pretty easily

What is third party employment practices liability insurance?

Think of third party employment practices liability insurance as your safety net when people outside your company claim your employees treated them unfairly. Unlike regular employment practices liability insurance that only covers your employees' complaints, this protects you when outsiders get upset.

This customer discrimination lawsuit protection kicks in when customers, vendors, suppliers, contractors, or even visitors claim your employees:

The coverage typically handles your legal defense costs, any settlements you need to pay, court judgments if you lose, and sometimes even crisis management to protect your reputation.

Here’s why this is different from regular Employment Practices Liability Insurance

Your standard employment practices liability insurance is all about employee-versus-employee or employee-versus-company issues.

But third party employment practices liability insurance is about protecting you when someone from the outside world says your people treated them badly.

It’s like the difference between family drama and neighbor complaints; they’re both problems, but they need different solutions. That’s why you need specialized non-employee harassment claims insurance protection.

How third party employment practices liability insurance works

When a discrimination or harassment incident occurs involving non-employees, third party employment practices liability insurance follows a systematic process to protect your business:

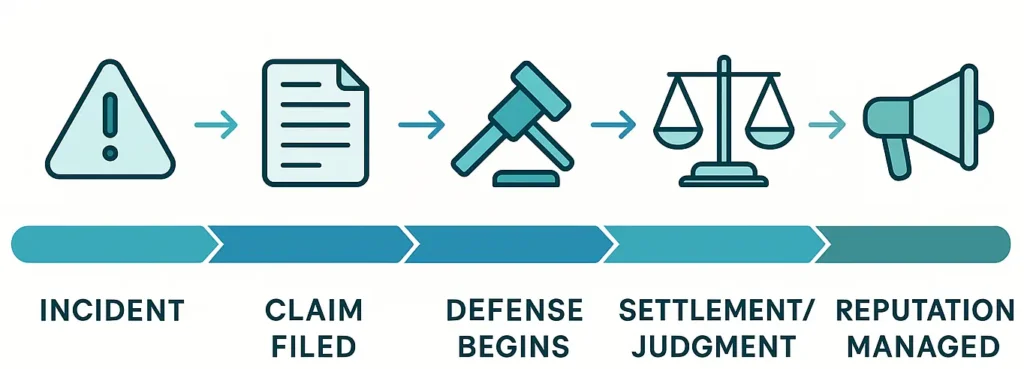

The claims process

- Incident occurs: A non-employee alleges a wrongful act (discrimination, harassment, etc.)

- Claim filed: Your insurer is notified and begins legal defense immediately

- Costs covered:

- Attorney fees and legal defense costs

- Settlements and judgments

- Crisis communication support (sometimes)

- Prevention and risk management:

- Implement policies to reduce inappropriate behavior

- Train staff to de-escalate and respectfully engage with all parties

Policy considerations

When securing customer discrimination lawsuit protection, consider these important factors:

- Choose adequate policy limits based on your industry’s typical claim costs

- Understand deductibles and exclusions that may affect coverage

- Review how the coverage integrates with your existing insurance program

- Ensure coverage includes both defense costs and settlement/judgment amounts

What costs are covered

Third party EPLI coverage typically protects against:

- Attorney fees and legal defense costs from the first dollar, regardless of claim validity

- Settlement amounts negotiated to resolve claims without costly trial proceedings

- Court judgments if cases proceed to litigation and result in adverse verdicts

- Plaintiff attorney fees which defendants must pay when they lose employment-related cases

- Crisis management expenses to protect your business reputation during high-profile claims

According to EEOC enforcement and litigation data, legal defense costs average $120,000 per claim, while settlement amounts for third-party claims typically range from $25,000 to $150,000.

Do you need Third party EPLI?

Look, if you’re running a business where you deal with customers, vendors, clients, or pretty much anyone who’s not on your payroll, you should probably have non employee harassment claims insurance. The more people you interact with, the higher your chances of someone feeling wronged and deciding to sue.

Businesses that need third party employment practices liability insurance

Here are the types of businesses that should definitely consider this protection:

- Retail stores – Customer service interactions can go sideways fast, especially around security and profiling issues

- Restaurants and hotels – Service quality disagreements can turn into discrimination claims quicker than you’d think

- Healthcare and wellness places – Patients are in vulnerable situations and emotions run high

- Schools and daycare centers – Parents can get pretty fired up if they think their kids weren’t treated fairly

- Real estate and property management – Fair housing laws are strict, and one wrong move can cost you big

- Transportation companies – Rideshare, delivery, taxi, you’re dealing with all kinds of people in close quarters

- Bars, clubs, entertainment venues – Mix alcohol with diverse crowds and things can get complicated

Even B2B companies aren’t safe

Think you’re off the hook because you don’t deal with the general public? Think again. If a contractor visits your office and feels harassed or discriminated against, they can absolutely sue you. Same goes for vendors, suppliers, and professional service clients. Understanding your business insurance needs means thinking about all these potential interactions.

Why your current insurance won’t help

Here’s the kicker: your commercial general liability insurance specifically excludes harassment and discrimination claims. It’s right there in the fine print. And your regular EPLI? That’s just for employee-versus-employee issues.

So when a customer claims discrimination, you’re basically on your own unless you have third party employment practices liability insurance.

How do I get started on Third Party EPLI?

Don’t overthink this. Here’s how to get third party employment practices liability insurance without making it complicated:

Step 1: Figure out your risk level

Ask yourself these questions:

- Do you deal with customers, clients, or vendors regularly?

- Have you ever had any complaints about how your employees treat people?

- What kinds of outside people come to your business or interact with your staff?

- How often do your employees have face-to-face interactions with non-employees?

Step 2: Look at what coverage you have now

Pull out your insurance policies and see what’s what:

- Do you have EPLI coverage already?

- Does it specifically mention third-party protection?

- What are your limits and deductibles?

- Are there any weird exclusions that might affect your business?

Step 3: Find a broker who gets it

Work with someone who actually understands employment practices risks and can:

- Help you add third party endorsement EPLI to what you’ve got

- Make sure your limits and deductibles make sense

- Set you up with some basic employee training and policies

- Shop around different insurance companies to get you the best deal

Picking the right insurance advisor is super important when you’re trying to figure out all these coverage gaps and get the protection you actually need.

What does third party EPLI coverage include?

Comprehensive third party EPLI coverage provides both financial protection and support services designed to minimize business disruption when external discrimination claims arise.

Core protection elements

- Legal defense coverage includes attorney fees, court costs, expert witness expenses, and investigation costs from the first dollar, regardless of whether claims prove valid or frivolous.

- Settlement protection covers negotiated amounts paid to resolve claims without the time, expense, and publicity of trial proceedings that could damage business reputation.

- Judgment coverage protects against adverse court verdicts if cases proceed to litigation and judges or juries rule against your business.

- Plaintiff attorney fees which federal employment law requires losing defendants to pay, often averaging $200,000 according to industry data.

Additional coverage benefits

- Crisis management support helps protect business reputation through professional communication strategies during high-profile discrimination claims or media attention.

- Training resources that many carriers provide to help prevent future claims through improved employee awareness and customer interaction protocols.

- Risk assessment tools to evaluate your business’s specific exposure levels and implement appropriate prevention strategies.

Industry-specific customer discrimination risks

Different industries face varying levels of customer discrimination lawsuit protection needs based on their interaction patterns and operational characteristics.

Retail and customer service businesses

High-volume customer interactions create frequent opportunities for misunderstandings, profiling allegations, and discrimination claims. Staff training on cultural sensitivity becomes crucial for risk management.

Customer service scenarios that commonly trigger claims include:

- Security procedures that appear to profile customers based on race or appearance

- Service quality variations that customers perceive as discriminatory treatment

- Product access restrictions that may violate disability accommodation requirements

Hospitality and food service

Guest services involve personal interactions that can escalate quickly when customers feel mistreated or discriminated against. Restaurant seating decisions, hotel room assignments, and service quality perceptions all present potential claim scenarios.

According to HUD fair housing information, hospitality businesses face particular scrutiny for accommodation policies and equal treatment standards.

Healthcare and wellness providers

Patient relationships involve vulnerable individuals in stressful situations, creating heightened sensitivity to perceived discrimination or inappropriate conduct. Medical settings require careful attention to cultural competency and respectful patient treatment.

Professional services and B2B interactions

Even businesses with limited public contact need non employee harassment claims insurance for vendor, contractor, and client interactions. Professional service providers hosting external parties must ensure appropriate workplace behavior standards.

Real stories that’ll make you want this coverage

Let me tell you about some situations I’ve seen that really drive home why you need customer discrimination lawsuit protection:

- The restaurant incident: A server allegedly made some racially insensitive comments to a customer. The customer sued the restaurant for discrimination. Without third party employment practices liability insurance, that restaurant had to pay all the legal costs and damages out of their own pocket. Not fun.

- The clothing store nightmare: A customer claimed they were racially profiled and wrongfully accused of shoplifting. Even though the claim was eventually thrown out, the legal defense alone cost the store $45,000. When you dig into what causes these claims, you realize how easily they can happen to any business.

- Hotel success story: A guest complained that a front desk clerk made inappropriate comments. Because the hotel had third party EPLI coverage, their insurance company handled everything—the legal response, the resolution, everything. The hotel didn’t pay a dime out of pocket and the whole thing got resolved quietly.

- Grocery store situation: A customer sued after claiming a cashier made homophobic remarks. The store’s third-party EPLI kicked in, covered the defense costs and a small settlement, and they avoided a long, expensive court battle.

- IT consulting close call: A consultant allegedly made some inappropriate jokes during a client visit. The client’s HR department got involved and threatened to sue. Third-party coverage helped protect the business and they even managed to keep the client relationship intact.

Here’s what happens when you don’t have third-party EPLI

Claims like these can seriously mess up your business:

- You’re looking at tens or even hundreds of thousands in legal fees and settlements

- Your reputation takes a hit, and that affects customer trust

- You lose business and deal with major operational headaches

Even if the claims turn out to be completely bogus, you still need lawyers to defend yourself. That costs money, money that could be much better spent growing your business.

Myths that could cost you big time

I hear these misconceptions all the time, and they’re exactly the kind of thinking that gets businesses in trouble:

“We’re too small to get sued”

Actually, small businesses get targeted more often because everyone knows you probably don’t have a big legal department or fancy HR policies. Plus, if you can’t afford to fight a lawsuit, you’re more likely to settle, which makes you an attractive target.

“We already have EPLI, so we’re covered”

Nope. Check your policy carefully—most standard EPLI only covers employee-versus-employee issues. Third-party employment practices liability insurance is usually a separate thing you have to ask for.

“We’ve never had any problems”

That’s great, but it doesn’t matter. One bad interaction is all it takes. According to the latest EEOC data, discrimination charges are actually going up—88,531 new charges filed in 2024, which is a 9.2% jump from the year before.

“Our general liability insurance covers this stuff”

Sorry, but no. The Insurance Information Institute makes it pretty clear—general liability specifically excludes harassment and discrimination claims. It’s all about slips, falls, and property damage, not employment issues.

Cost considerations for third party protection

Third party employment practices liability insurance costs vary significantly based on industry risk, business size, and coverage limits, but typically represent a fraction of potential claim costs.

Premium factors

Prevention strategies for customer interactions

While third party EPLI coverage provides essential financial protection, proactive risk management helps prevent claims and reduces overall business liability exposure.

Comprehensive employee training programs

Implement regular training covering appropriate customer interactions, cultural sensitivity, and de-escalation techniques. Include specific scenarios relevant to your industry and customer base.

Training should address:

- Cultural competency and respectful treatment of diverse customers

- De-escalation techniques for handling customer complaints or conflicts

- Appropriate boundaries in customer service interactions

- Incident reporting procedures when problems arise

Clear policies and procedures

Establish written guidelines for customer service interactions, complaint handling, and incident documentation. Ensure all staff understand expectations, consequences, and proper escalation procedures.

Policy areas should include:

- Customer service standards emphasizing equal treatment

- Complaint resolution processes that address concerns promptly

- Incident documentation requirements for potential legal protection

- Training requirements and regular refresher schedules

Technology and monitoring considerations

Consider security cameras in customer service areas to provide objective evidence of interactions, while ensuring compliance with privacy laws and informing employees and customers of monitoring practices.

Data breach prevention strategies should also consider employment practices implications when implementing customer interaction monitoring systems.

The business case for third party employment practices liability insurance

Beyond financial protection, third party employment practices liability insurance provides strategic business advantages that support long-term success and growth in customer-facing markets.

Reputation protection during claims

Professional claims handling and legal representation help minimize negative publicity and social media backlash during claim situations. Insurance carriers often provide crisis communication support to protect brand image during legal proceedings.

Operational continuity benefits

Coverage prevents business disruptions from lengthy legal proceedings, allowing management to focus on core operations rather than litigation management while insurance professionals handle legal defense.

Competitive market advantages

Companies with comprehensive customer discrimination lawsuit protection can confidently pursue diverse customer bases and enter new markets without fear of catastrophic liability exposure from discrimination claims.

Enhanced customer confidence

Demonstrating commitment to inclusive business practices through proper insurance protection can attract customers who value diversity and social responsibility in their business relationships.

Don’t wait until it’s too late

Look, nobody wants to think about getting sued by customers or vendors, but it happens more than you’d think. Third party employment practices liability insurance isn’t just nice to have—it’s protection that could literally save your business from financial disaster.

Whether you’re running a restaurant, retail store, healthcare practice, or any other business that deals with people, this coverage could be the difference between a minor headache and a major catastrophe.