Multi-Family Office Insurance

The Complete Coverage Guide for Multi-Family Offices

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

Running a multi-family office means you are trusted by multiple wealthy families to protect, grow, and manage their most valuable assets, which creates specialized family office insurance needs. That trust carries legal weight. Every investment decision, piece of advice, and process you manage creates a liability exposure that standard commercial insurance programs were never designed to handle. A properly structured MFO insurance program addresses professional liability, fiduciary exposure, SEC regulatory risk, cyber threats, and internal fraud, all in one coordinated structure built specifically for registered investment advisers.

The Bottom Line. TL;DR

Multi-family offices face a more complex insurance challenge than single-family offices or standard businesses. Your program needs to address professional liability, fiduciary exposure, cyber threats targeting high-net-worth client data, and SEC compliance, all in one coordinated structure. Getting this wrong leaves your principals personally exposed.

Bottom line

The challenge is that most MFOs discover coverage gaps only after a claim surfaces. By then, it is too late to fix them.

Here is what a properly structured multi-family office insurance program looks like, and what is at stake if yours does not measure up.

What Makes Multi-Family Office Insurance Different From Standard Business Coverage?

Multi-family office insurance covers a fundamentally different risk profile than any standard commercial policy. A BOP is primarily designed to cover tangible risks, such as property damage and bodily injury to third parties.

An MFO faces client disputes, wire fraud, SEC inquiries, and fiduciary claims, none of which a standard policy was built to cover. The gap is wider than most operators expect, and it shows up at claim time.

Most MFOs operating on a generic commercial program are relying on a generalist broker who placed coverage that works for a retail company or professional services firm. That is the substitute behavior.

It fails because:

The downstream cost of that gap is not abstract. A single fiduciary breach allegation from one of your client families can cost $250,000 to $5 million in defense costs before any judgment is entered. That reaches your principals personally if the right policy is not in place.

For a no-cost program review, we will tell you exactly where your current coverage falls short.

What Coverages Does a Multi-Family Office Actually Need?

A properly structured MFO insurance program requires at a minimum six core coverages: D&O, E&O, fiduciary liability, cyber, crime/fidelity, and EPLI. Higher limits and broader terms are required across nearly every line compared to a single-family office, and the policy terms matter as much as the limits. The nuances in how each coverage is written determine whether it actually pays when a claim hits.

Here is how each coverage works in practice:

Coverage |

What It Covers |

Why MFOs Need Higher Limits |

|---|---|---|

|

Directors & Officers (D&O) |

Personal asset protection for executives and board members sued for management decisions |

External advisors, client family board members, RIA regulatory exposure |

|

Errors & Omissions (E&O) |

Professional mistakes, negligence, failure to perform contracted services |

Multi-family investment management errors, tax/estate advice, admin failures |

|

Fiduciary Liability |

Breach of fiduciary duty claims related to benefit plans and trust administration |

Multiple client families with potentially competing interests |

|

Cyber Insurance |

Ransomware recovery, wire transfer fraud, business interruption, crisis communications |

Concentrated HNW data + lean IT teams = prime target |

|

Crime/Fidelity |

Employee theft, forgery, social engineering fraud |

Wire transfer losses, internal fraud exposure |

|

Employment Practices Liability (EPLI) |

Wrongful termination, discrimination, harassment |

Even small MFO teams generate these claims regularly |

What 40+ years in commercial insurance has shown us

It is rarely the coverage everyone thinks about that creates a crisis. It is the one nobody thought to ask about.

To review your current program against this framework.

How Does SEC Registration Change Your Insurance Requirements?

SEC registration as a registered investment adviser materially increases your liability exposure and requires explicit policy terms that most off-the-shelf D&O and E&O policies do not include by default. Single-family offices are generally exempt under the Dodd-Frank Act’s family office exclusion. Multi-family offices are not. The policy language differences are not minor adjustments, they are the difference between coverage that responds and coverage that does not.

Once registered with the SEC under the Investment Advisers Act of 1940, your firm is subject to:

Your E&O and D&O policies need to explicitly cover:

Not all policies include this by default. It is a term-level distinction that is easy to miss if your broker is not specialized in investment management insurance.

Additionally, pending legislation could require SEC registration for family offices with $750 million or more in AUM, broadening regulatory exposure further. The window to build the right program before those requirements tighten is now.

What Is Fiduciary Liability Insurance and Why Does Every MFO Need It?

Fiduciary liability insurance protects MFO principals from personal exposure when a client, beneficiary, or employee claims you breached your fiduciary duty. It is separate from E&O and D&O, and it addresses a risk that is uniquely elevated for offices serving multiple families simultaneously. The coverage gap between what MFOs assume they have and what they actually have in this category is consistently the most dangerous one we find.

In my experience, fiduciary liability is the coverage that surprises MFO operators most when they review their programs carefully. Most assume their D&O or E&O policy handles fiduciary claims. It does not, not fully.

Fiduciary liability specifically addresses:

The exposure is compounded at the MFO level because you are serving multiple families with potentially competing interests. A decision that benefits one client family could trigger a fiduciary claim from another alleging preferential treatment or unequal management.

Cost comparison: fiduciary liability premium vs. uninsured claim

Scenario |

Estimated Cost |

|---|---|

|

Annual fiduciary liability premium (mid-size MFO) |

$8,000 – $25,000 |

|

Defense costs for a single fiduciary breach allegation |

$250,000 – $5,000,000+ |

|

Potential judgment if defense fails |

Additional $1M – $10M+ |

Without dedicated fiduciary liability coverage, that claim reaches your principals personally.

To review your fiduciary exposure, we work with family offices across the US.

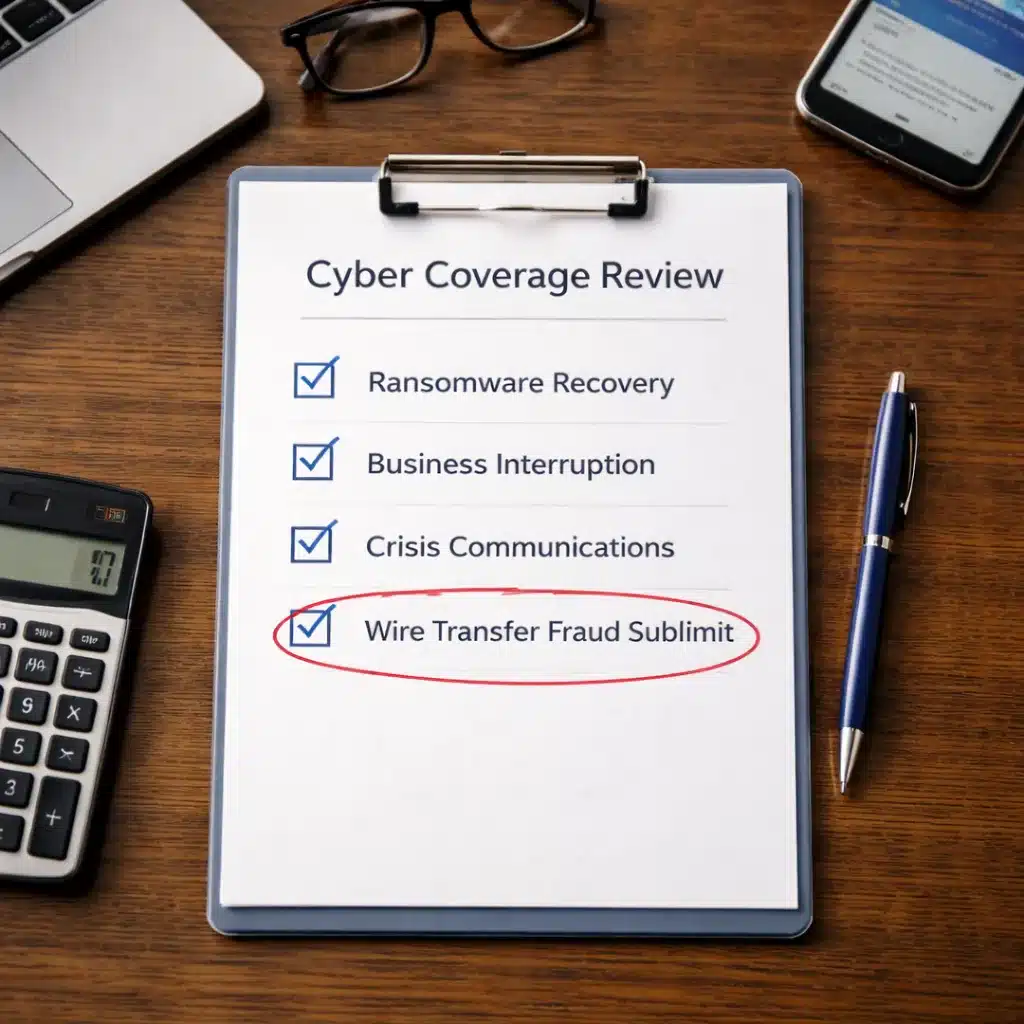

Why Cyber Insurance Is Non-Negotiable for Multi-Family Offices

Multi-family offices are prime targets for cybercriminals because they combine high-value financial data, lean IT infrastructure, and high-stakes wire transfer activity. A single successful attack can cost $100,000 to $3 million or more in recovery costs, and that is before accounting for the reputational damage to client families who trusted you with generational wealth. But the real danger is that most MFO cyber policies do not cover what MFOs actually lose money on.

Real-world example

A mid-sized MFO in the Northeast discovered this the hard way.

Business Email Compromise – $500,000 Wire Fraud

A fraudster compromised a senior employee’s email account and sent a wire transfer request for $500,000 to an overseas account. An employee, believing the request was legitimate, wired the funds without verbal confirmation. The MFO discovered the fraud three days later. That single event triggered three simultaneous claims: cyber, crime/fidelity, and EPLI when the employee was subsequently terminated. Three coverages from one incident, and the cyber policy had a sublimit on social engineering fraud that left $175,000 unrecovered.

MFO cyber coverage needs to go beyond basic breach notification.

Look specifically for policies that cover:

Many standard cyber policies exclude wire transfer fraud or sublimit it to $100,000 or less. Confirm yours does not before you need to find out.

For a cyber coverage gap analysis specific to family office operations.

What Does Multi-Family Office Insurance Actually Cost?

MFO insurance program costs range from $15,000 to $150,000 or more annually, depending on AUM, number of client families, investment complexity, employee headcount, and claims history. Multi-family offices with SEC registration and higher AUM sit toward the upper end of that range. The right question is not how to minimize the premium; it is whether your limits match your actual exposure.

Premium range by MFO profile:

MFO Profile |

Estimated Annual Premium |

|---|---|

|

Early-stage MFO, 2-4 families, AUM under $250M |

$15,000 – $35,000 |

|

Mid-size MFO, 5-10 families, AUM $250M – $750M |

$35,000 – $75,000 |

|

Established MFO, 10+ families, AUM over $750M, SEC-registered |

$75,000 – $150,000+ |

An MFO with $500 million in AUM carrying $1 million D&O limits is underinsured by almost any measure. Bundling coverages with a single specialty carrier that understands family office operations can reduce total program cost while simultaneously increasing limits and broadening terms.

Key cost drivers to discuss with your broker:

To get a program built around your actual AUM and structure, not a templated quote.

How Does The Coyle Group Build Multi-Family Office Insurance Programs?

The Coyle Group has spent over 40 years building insurance programs for businesses where the stakes are personal, including family offices managing generational wealth across multiple families. Our process starts with a full exposure review across your AUM, entity structure, regulatory status, and operational risk profile before we approach any carrier.

We work exclusively with specialty carriers that understand financial services firm insurance and MFO exposures. Our process:

Our goal is a program where nothing falls between the cracks at claim time, because that is the only time the program truly matters.

What Happens When a Claim Occurs at a Multi-Family Office?

The claims process at an MFO involves multiple coverages responding simultaneously, and the order of operations matters more than most operators realize. When a claim event occurs, the sequence your broker manages can determine whether you recover fully or absorb significant uninsured losses. Most MFOs have never walked through this with their broker, which means the first time they do, it happens under the worst possible conditions.

Claim Event |

Primary Coverage |

Secondary Coverage |

What Gets Missed Without Planning |

|---|---|---|---|

|

Client family alleges investment mismanagement |

E&O |

D&O (if management decision is involved) |

Fiduciary gap if trust assets are involved |

|

Wire transfer fraud via spoofed email |

Crime/Fidelity |

Cyber (if network was compromised) |

Cyber sublimits often cap recovery below the loss |

|

SEC examination initiated |

D&O (regulatory defense) |

E&O (if advisory practices are reviewed) |

Policies without explicit SEC defense cost coverage leave you exposed |

|

Ransomware attack on client data |

Cyber |

Business interruption rider |

Standard cyber often excludes client notification costs above a sublimit |

|

Employee wrongful termination claim |

EPLI |

D&O (if management decisions are implicated) |

Without EPLI, principals are personally named in the claim |

The key insight

Claims at MFOs rarely involve a single coverage. They cascade. Your broker needs to have pre-mapped how your policies interact before an event occurs, not after.

What to confirm with your broker before a claim happens:

To pre-map your coverage response before you need it.

Common Mistakes Multi-Family Offices Make With Insurance

Most coverage gaps at MFOs are not caused by negligence. They are caused by working with brokers who do not specialize in this space. These are the patterns we see most consistently, and the ones that show up in claims:

Using the same policy structure as a single-family office.

Single Family Office programs are built for one set of interests and one family’s liability exposure. MFOs require separate limits, broader terms, and policy language that explicitly addresses multi-client operations. An SFO program does not transfer cleanly to an MFO structure.

Assuming D&O covers fiduciary claims. It does not.

D&O and fiduciary liability are separate products covering separate exposures. D&O covers management decisions; fiduciary liability covers obligations under ERISA, state trust law, and the management of benefit plans and trust structures. The exclusion language in most D&O policies will leave a fiduciary claim exposed.

Buying cyber insurance without reviewing the wire fraud sublimit.

Many policies cap wire transfer fraud at $100,000 to $250,000. MFOs regularly process wire transfers 10 to 100 times that size. The sublimit needs to match your actual wire transfer exposure, not the carrier’s default.

Not disclosing SEC registration status to the carrier.

If you are a registered investment adviser and your policy application did not ask about it explicitly, your coverage may not respond to regulatory claims. This is a material fact that must be disclosed at application.

Reviewing the program only at renewal.

AUM growth, new client families, and expanded services such as trust administration and real estate management all create mid-year coverage gaps that annual renewals frequently miss. An MFO that doubled its AUM mid-year is carrying last year’s limits until renewal.

Treating the insurance program as a commodity purchase.

The difference between a specialty broker and a generalist is not the premium – it is the policy terms. Exclusions, sublimits, and coverage triggers written into a policy at inception are negotiated, not standardized. A generalist broker often cannot access or negotiate the specialty market terms that MFO programs require.

The Insurance Information Institute consistently reports that commercial insurance buyers underestimate professional liability exposure by a significant margin. For an MFO, that underestimate is not a budget problem. It is a personal liability problem for your principals.

Questions about Multi-Family Office Insurance

Get the Right Multi-Family Office Insurance Program

The Coyle Group has spent over 40 years building insurance programs for businesses where the stakes are personal – including family offices managing generational wealth across multiple families. Our process starts with a full exposure review across your AUM, entity structure, regulatory status, and operational risk profile before we approach any carrier.

We work exclusively with specialty carriers that understand financial services firm insurance and MFO exposures. Our goal is a program where nothing falls between the cracks at claim time – because that is the only time the program truly matters.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

For a no-cost program review, we will tell you exactly where your current coverage falls short.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?