Investment Management Insurance

Tailored Coverage for RIAs, Funds, and Family Offices

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Protect Client Assets. Safeguard Your Firm.

Investment Management Insurance (IMI) is a specialized insurance program for firms and professionals that manage third-party assets. It combines Professional Indemnity (E&O), Directors & Officers liability, Crime/Fidelity coverage, and Cyber insurance into a coordinated program that addresses the fiduciary, regulatory, and operational exposures that standard business policies don’t cover.

This coverage is built for investment management firms that manage, advise on, or control client assets, including RIAs, hedge funds, private equity firms, and family offices. If your firm has fiduciary responsibility, regulatory exposure, or authority over client capital, standard business insurance leaves critical gaps. Investment management insurance is designed to protect your firm against professional liability, management decisions, cyber incidents, and financial loss scenarios unique to asset management.

What 40+ Years Taught Me About This Risk

In four decades of helping investment managers navigate insurance challenges, three patterns keep appearing: the same gaps recur, the same mistakes get made, and the firms that get hurt aren’t the ones that skipped insurance; they’re the ones that bought the wrong kind.

Successful investment managers treat insurance as part of their compliance infrastructure, not an afterthought.

The Bottom Line: Key Takeaways

See what coverage you actually need

Investment Management Insurance Pricing

Pricing varies by AUM, client mix, claims history, and cyber controls. Two firms with identical AUM can differ by 40–60% in premiums based on security documentation, client concentration, regulatory history, and prior claims, which is why the ranges below show floors and ceilings rather than averages.

Typical Annual Premium Ranges

These ranges assume a firm with clean claims/regulatory history, standard retentions, and average cyber controls. Premiums can move materially based on strategy complexity (alts/derivatives), investor profile, SEC/FINRA history, prior claims, required limits from custodians/investors, and whether you need enhanced endorsements (informal investigations, social engineering, or broad “professional services” definitions).

Who This Insurance Protects

Registered Investment Advisors (RIAs)

SEC or state-registered firms providing fee-based investment advice, discretionary portfolio management, and financial planning services. Whether you’re managing $50 million or $5 billion in client assets under management (AUM), E&O insurance is typically required by custodians and represents best practice protection.

Hedge Funds & Private Equity Firms

Alternative investment managers face unique exposures from complex strategies, derivatives, leverage, and sophisticated investor relationships. D&O insurance protects fund managers from investor lawsuits, while E&O covers professional services rendered to the fund.

Family Offices

Single and multi-family offices providing comprehensive wealth management, trust administration, and concierge services need combined E&O and D&O protection. Fiduciary liability coverage becomes critical when managing trust assets or serving in trustee capacities.

Broker-Dealers & Dual-Registered Representatives

Firms offering both commission-based and fee-based services require specialized policies covering the full spectrum of activities. Away-from-firm RIA activities demand separate protection beyond broker-dealer coverage.

Mutual Fund Managers & Portfolio Companies

Fund management companies, sub-advisors, and investment portfolio operations teams all require tailored protection for their specific roles in the investment process.

Investment management insurance is part of broader financial services insurance solutions that address the unique risks facing advisors, fund managers, and wealth management firms.

Not sure where you fit?

The Real Risks Investment Managers Carry Daily

Investment managers face a unique combination of professional liability, fiduciary responsibility, regulatory exposure, and cybersecurity threats, often simultaneously, and often involving the same underlying event triggering multiple coverage lines at once.

Professional Services Liability Exposure

Investment management creates continuous exposure to allegations of negligence, errors, or omissions in professional services. Investment managers encounter several common claim scenarios, including:

Trade Execution Errors

Fat-finger trades, timing mistakes, allocation errors, and failure to execute agreed-upon trades create immediate exposure.

Investment Advice Claims

Unsuitable investment recommendations based on client risk profile, failure to properly diversify portfolios, concentrated positions resulting in losses, and misrepresentation of investment risks create liability.

Performance & Reporting Issues

Errors in performance calculation or reporting, failure to follow stated investment policy or strategy, benchmark comparison inaccuracies, and fee calculation mistakes trigger claims.

According to FINRA dispute resolution statistics, thousands of cases are filed annually with the largest volume of allegations being breach of fiduciary duty and negligence – precisely what E&O insurance addresses.

Fiduciary Duty Allegations

When you accept discretionary authority over client assets or serve in advisory capacities, you assume fiduciary responsibilities creating distinct liability exposure. Fiduciary duty claims often stem from conflicts of interest not properly disclosed, self-dealing or undisclosed compensation arrangements, failure to act in clients’ best interests, and inadequate due diligence on investments or managers.

Defense costs can quickly exceed tens of thousands, even when claims lack merit. Without proper insurance, these costs come directly from your operating capital.

When investment managers serve as ERISA plan trustees, pension consultants, or in other fiduciary capacities, investment management insurance must include specialized fiduciary liability coverage.

Cybersecurity & Data Breach Threats

Furthermore, investment managers hold treasure troves of sensitive financial data making them prime targets for cybercriminals. Ransomware attacks increased significantly in 2023-2024 with the financial sector experiencing particularly severe targeting.

Common cyber incidents affecting investment managers:

Mid-market cyber incidents routinely reach six figures when forensics, notification, and business interruption are included.

Understanding what cyber insurance actually covers helps you evaluate whether your protection is adequate.

Regulatory Investigation Costs

SEC examinations, FINRA inquiries, and state regulatory investigations create substantial expense even when no violations are found. Legal defense costs for responding to regulators can quickly reach six figures.

Additionally, many E&O policies now include informal investigation coverage (typically sublimited $25k-$100k and varies by carrier/policy) providing reimbursement for attorney fees for regulatory response, document production and review, compliance consultant engagement, and expert witness fees.

Social Engineering & Wire Fraud

Investment managers move large sums regularly, making them attractive targets for sophisticated wire fraud schemes. Social engineering attacks manipulate employees into authorizing fraudulent transfers.

Illustrative Scenario: Wire Fraud Attack

A portfolio manager receives an email appearing to come from a client requesting an urgent wire transfer of $500,000 to a new bank account. The email address looks legitimate, the message references recent conversations, and time pressure is applied. The transfer is authorized.

Hours later, the real client calls asking about their account balance. The fraudulent transfer has been sent to an overseas account and cannot be recovered.

Without proper crime insurance

The firm absorbs the $500,000 loss entirely, potentially triggering E&O claims from the client for negligence in processing the transfer.

With comprehensive crime/social engineering coverage

The insurance policy covers the stolen funds (typically up to the sublimit), and the firm’s financial stability remains intact.

Director & Officer Liability

Moreover, fund managers, GP partners, and RIA principals face personal liability for decisions made in management capacities. D&O insurance protects individuals from investor lawsuits alleging mismanagement, regulatory investigations of leadership, alleged breaches of duty to the fund or firm, and employment practices claims against executives.

Directors and Officers insurance becomes especially critical as firms grow and outside investors or board members join.

The 3 Coverage Mistakes That Leave Investment Managers Exposed

After four decades helping investment managers navigate insurance challenges, I’ve witnessed how overlooked exposures can devastate otherwise successful firms. Three patterns stand out:

1. The $1M Trap

Most RIAs start with $1 million E&O limits because that’s what custodians require. But realistic breach scenarios, combining defense costs, settlement, and business interruption, often exceed $2-3 million. For RIAs managing $100-500M AUM, consider $2-3M as a realistic floor. Firms don’t realize they’re underinsured until a claim depletes their coverage and leaves them personally exposed.

2. Coverage Gaps Between Policies

Many firms assume their E&O policy covers cyber incidents or their D&O policy protects the fund. Critical exposures fall between policies because managers don’t understand which risks each policy actually addresses. Proper structuring ensures overlapping protection without gaps.

3. Late Notice Disasters

Claims-made policies only respond when proper notice is given during the policy period. I’ve seen firms discover potential claims, delay reporting to avoid premium increases, and lose all coverage when the claim materializes months later under a new policy with different terms.

Successful investment managers treat insurance as part of their compliance infrastructure, not an afterthought. They review coverage annually, maintain proper limits, and integrate risk management into daily operations.

Comprehensive Investment Management Insurance Coverage

Investment management firms require coordinated coverage across five distinct exposure categories, not a single policy. The coverages below address professional liability, management decisions, digital threats, employee theft, and operational risks that standard business policies were never designed to handle.

Coverage Definitions & Triggers

Here’s how the core policies interlock and typical starting limits firms choose:

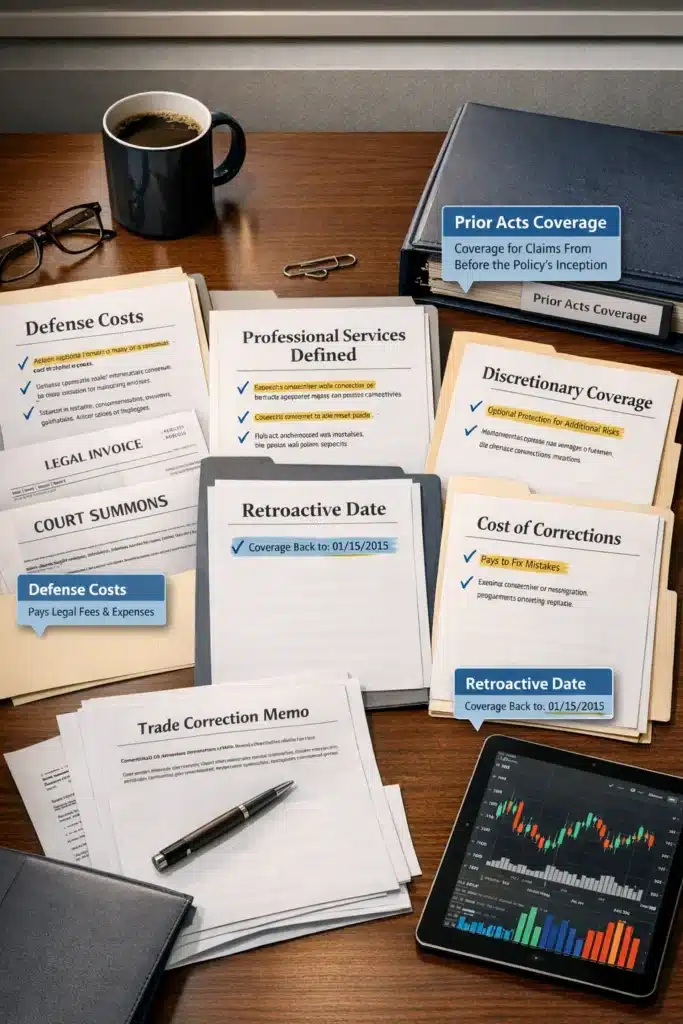

Professional Liability (E&O) for Investment Advisors

E&O (Professional Liability) protects you when a client, investor, or regulator alleges your investment management services caused financial harm, whether or not you actually did anything wrong. In practice, most claims come from trade execution mistakes, suitability/disclosure disputes, performance reporting errors, or alleged failure to follow the stated mandate.

The difference between “covered” and “denied” usually comes down to policy wording, especially how “professional services” is defined, whether discretionary authority is endorsed, and whether defense costs erode your limit.

Key coverage features:

Defense Costs

The policy pays attorney fees, expert witnesses, court costs, and other defense expenses. In most policies, these costs reduce your policy limits (eroding coverage), though some carriers offer defense outside limits as an enhancement.

Professional Services Definition

Careful attention to how your policy defines “professional services” determines what’s actually covered. Strong policies broadly define covered services to include investment advisory and portfolio management, financial planning and consulting, research and analysis, use of sub-advisors or outside managers, and fiduciary services to clients.

Discretionary vs. Non-Discretionary Coverage

Standard policies cover non-discretionary advisory services. Discretionary management, where you have authority to execute trades without pre-approval – often requires specific endorsement and may limit covered investments to mutual funds and ETFs, publicly traded stocks and bonds, REITs on established exchanges, and covered calls and protective puts.

Alternative investments (private placements, hedge funds, derivatives beyond simple options) typically require specialized coverage with enhanced premiums.

Prior Acts / Retroactive Date

Your policy’s retroactive date determines how far back in time coverage extends. Maintaining continuous coverage with the same retroactive date protects you for services rendered years ago that result in claims today. Changing carriers without negotiating proper prior acts coverage creates dangerous gaps.

Cost of Corrections Coverage

This essential feature reimburses expenses to correct errors before they become claims. Whether it’s a trade error requiring market adjustment or operational mistake needing client notification, cost of corrections coverage allows quick remediation without exhausting policy limits.

Most carriers require written notice within 72 hours of discovery for cost-of-corrections claims. Recent carrier restrictions have limited this coverage to trade errors only with strict notification requirements. Experienced brokers negotiate to maintain broad cost of corrections protection.

Unsure about your retro date?

Management Liability (D&O) Insurance

Many investment managers assume E&O protects them personally. It doesn’t. E&O responds to allegations about professional services (advice, trading, reporting), while D&O responds to allegations about how the firm or fund is governed and managed, and those claims often name partners, principals, and GPs individually.

If an investor, board member, employee, or regulator alleges a “wrongful management act,” D&O is the coverage designed to protect personal assets and leadership decisions.

D&O insurance protects individuals serving as directors, officers, general partners, or managing members from personal liability arising from their management decisions.

Who’s covered

RIA principals and executive officers, general partners of fund management companies, board members and independent directors, advisory board members, and trustees and fiduciaries.

What triggers coverage

D&O claims most often arise when investors allege mismanagement or breach of duty (especially after a drawdown), when regulators scrutinize disclosures, supervision, valuation, or marketing practices, when leadership faces employment-related disputes, or when internal governance/ownership conflicts escalate into formal allegations against principals.

Entity vs. Individual Coverage

D&O policies typically provide:

Priority of Payments

Understanding how your D&O policy allocates coverage between the fund, management company, and individuals prevents unpleasant surprises. Strong policies ensure adequate protection remains for individuals even after entity claims are paid.

Want to confirm Side A/B/C fit?

Cyber Insurance for Investment Managers

Cyber insurance has evolved from optional to essential as digital threats proliferate. Investment managers require coverage addressing both first-party costs and third-party liability.

Most claims touch both sides; right-sizing limits prevents sublimit bottlenecks.

Required Security Controls

Cyber insurers now mandate specific controls as coverage prerequisites:

Firms unable to document these controls face coverage denial or severely limited policies.

Crime Insurance / Financial Institution Bond

Crime insurance protects against employee dishonesty, social engineering theft, and fraudulent wire transfers, exposure areas not covered by E&O or cyber policies.

Coverage Components:

Social Engineering Sublimits

Many crime policies sublimit social engineering coverage to $100,000-250,000. For investment managers moving multi-million dollar sums, these sublimits provide inadequate protection. Negotiate higher dedicated sublimits or separate social engineering coverage.

Required Control Procedures

Carriers mandate specific wire transfer verification procedures:

Failing to follow mandated procedures can void coverage even for legitimate claims.

Understanding the difference between cyber and crime insurance helps ensure you have both protections without assuming one covers the other’s exposures.

Fiduciary Liability Insurance

When investment managers serve as ERISA plan trustees, pension consultants, or in other fiduciary capacities, specialized fiduciary liability coverage becomes critical.

What Triggers Coverage

Breach of fiduciary duty under the Employee Retirement Income Security Act (ERISA), imprudent investment selection or monitoring, prohibited transactions, failure to follow plan documents, inadequate disclosure to participants, and excessive fee allegations.

Who Needs This Coverage

Firms managing 401(k) or pension plans, trustees of benefit plans or trusts, investment committees for retirement plans, 3(21) and 3(38) fiduciaries, and family office trustees.

Employment Practices Liability (EPLI)

Employment Practices Liability Insurance (EPLI) defends claims by employees, former employees, or job applicants alleging discrimination, harassment, wrongful termination, retaliation, and wage and hour violations.

Comprehensive investment management insurance programs include EPLI because investment managers with high-compensation employees face heightened risk. Single claims can easily exceed $250,000 when factoring defense costs and settlements.

Excess Liability / Umbrella Coverage

Excess policies provide additional limits that sit above underlying E&O, D&O, Cyber, and GL coverages. As your firm grows and exposure increases, umbrella protection prevents catastrophic scenarios from exhausting primary coverage.

Many investment management insurance programs include excess policies as a cost-effective way to increase total protection without dramatically raising base coverage limits.

Why Standard Business Insurance Falls Short

Generic business owner policies fundamentally fail to address investment management exposures. Investment management insurance differs significantly from standard policies because it’s designed for firms providing professional advisory services, not businesses with product sales, physical inventory, and customer injuries.

Most critically, standard policies exclude professional services of any kind, errors or omissions in advice provided, fiduciary responsibilities, financial losses suffered by clients, and regulatory compliance costs.

Attempting to protect an investment management firm with standard business insurance is like wearing a raincoat in a hurricane – technically clothing, completely inadequate for the actual threat.

See where your current program falls short

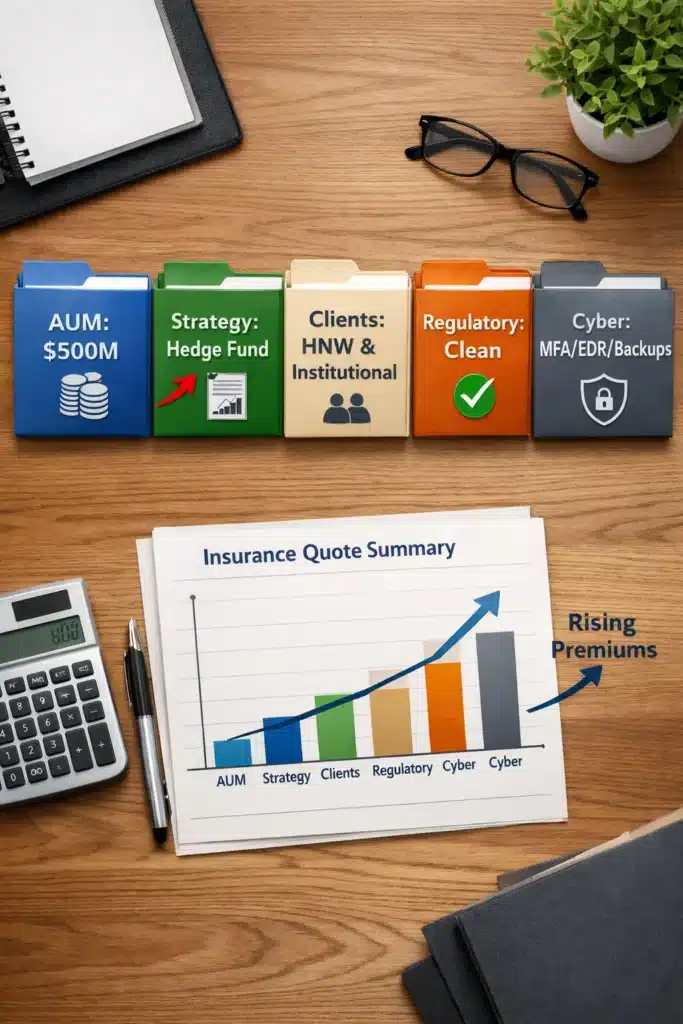

Key Cost Drivers

Investment management insurance premiums vary based on several factors that underwriters evaluate carefully:

Assets Under Management

Higher AUM typically correlates with higher premiums since potential loss severity increases. However, the relationship isn’t linear; firms with $1 billion AUM don’t pay 10x more than $100 million AUM firms.

Investment Strategy & Complexity:

Client Composition:

Regulatory & Claims History:

Cybersecurity Controls

Demonstrable security measures reduce cyber premiums. MFA, EDR/MDR, backup testing, security training, and incident response testing can earn up to 10-15% credits each with some carriers:

Strong controls can reduce premiums by 30-40% compared to firms with inadequate security.

Premium Comparison: Good vs. Better vs. Best

Good: Minimum Acceptable Protection

Better: Industry Standard Protection

Best: Comprehensive Protection

Ranges are indicative; carrier appetite, claims history, and strategy complexity drive final pricing.

Coverage Pitfalls Investment Managers Must Avoid

Understanding common mistakes in investment management insurance selection helps you avoid expensive coverage gaps. Each of the pitfalls below has a documented track record of causing coverage denials or partial recoveries. Here are seven critical pitfalls:

1: Using Generic E&O Not Tailored to Investment Advisory

Many RIAs purchase generic “professional liability” policies not designed for investment advisory services. Solution: Obtain E&O policies explicitly designed for SEC/state-registered investment advisors with clear professional services definitions, discretionary endorsements, and cost of corrections coverage.

2: Inadequate Social Engineering / Wire Fraud Protection

Standard crime policies sublimit social engineering coverage to $100,000-250,000. For firms moving multi-million dollar sums, a single incident exhausts this coverage. Solution: Negotiate dedicated social engineering coverage of $500,000-$1,000,000+ with documented verification procedures.

3: Retroactive Date Resets When Changing Carriers

Switching E&O carriers without negotiating prior acts coverage creates gaps for claims from services rendered before the new policy’s retroactive date. Solution: Maintain continuous coverage with the same retroactive date or purchase extended reporting period (tail) coverage.

4: Assuming Cyber Policy Covers All Technology Risks

Cyber policies exclude professional errors delivered electronically (E&O needed), employee theft via computer systems (Crime needed), and vendor contract penalties. Solution: Coordinate multiple policies to avoid gaps.

5: Late Notice / Wrong Policy Reporting

Claims-made policies require notice during the policy period. Delayed notice destroys coverage. Solution: Report all potential claims immediately when first discovered. “When in doubt, report” should be your guiding principle.

6: Vendor Risk Not Scheduled or Addressed

Many cyber policies exclude coverage for breaches originating from third-party vendors unless specifically scheduled. Solution: Conduct vendor security due diligence and ensure your cyber policy covers vendor-originated breaches through scheduling or broad third-party coverage.

How The Coyle Group Structures Investment Manager Protection

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

Questions about Investment Management Insurance?

These common questions about investment management insurance help you understand coverage requirements, costs, and protection strategies:

Your Next Steps: Getting Protected

If you’re questioning whether your current investment management insurance actually protects your firm, let’s have a direct conversation about your specific situation.

Three Ways We Help

1. Comprehensive Coverage Review

We audit your existing policies against your actual operations, identifying gaps, inadequate limits, and potential claim denial scenarios. You’ll receive a clear assessment of where you’re protected and where exposure exists.

2. Program Design & Market Access

Based on your risk profile, we design integrated protection and access specialized investment manager carriers you can’t reach directly. You’ll receive competing proposals allowing informed decision-making.

3. Implementation & Ongoing Advocacy

After placement, we ensure proper execution, certificate issuance, and annual review as your firm evolves. When claims arise, we advocate for you with carriers to maximize recoveries.

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, with 40+ years helping investment managers design and maintain effective insurance programs. Gordon specializes in helping RIAs, hedge funds, private equity firms, and family offices develop comprehensive insurance programs that protect their operations, satisfy regulatory and custodial requirements, and support their growth objectives.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

VC Insurance: 4 Essential Coverages Every Venture Capital Firm Needs

How to Get the Best Venture Capital Insurance: A Practical Guide for Fund Managers

Business Insurance for Financial Advisors