Quick Answer

Shopping for business insurance means identifying the coverages your business actually needs, comparing protection rather than price alone, and working with a broker who helps you avoid costly gaps. For most small businesses, the right process includes reviewing risks, choosing core policies like general liability, property, workers comp, and cyber, and reassessing coverage every year before renewal.

Most business owners approach shopping for business insurance the same way they approach going to the dentist: they put it off, rush through it when they have to, and hope for the best. The problem is that a bad dental visit costs you a crown. A bad insurance decision can cost you your business.

According to a survey published by Insurance Journal, 90% of small business owners lack confidence that they are adequately insured, and 29% have no business insurance at all. Meanwhile, 96% of surveyed owners failed a basic general liability knowledge test. These are not small numbers. They represent real businesses with real gaps that would be devastating in a claim.

This guide walks you through what you need to know when shopping for business insurance: the coverage types that matter, what things actually cost, the mistakes that will hurt you, and how to find a broker who works for you, not the insurance company.

Why Is Shopping for Business Insurance So Confusing?

Shopping for business insurance is confusing because no two businesses face the same risks, policies are written in dense legal language, and most online tools reduce a complex transaction to a price quote that tells you almost nothing useful. The bigger problem is that confusion leads to undercoverage, and undercoverage only reveals itself when it is too late.

The insurance buying process was designed around brokers explaining policies to clients face to face. When that step gets removed, replaced by comparison websites or quick-quote forms, what gets lost is the most important part: understanding what you are actually buying.

Here is what the data shows about where business owners struggle most:

The solution is not a better quote engine. It is a better process. Browse The Coyle Group’s Insurance By Coverage hub to see the full range of commercial coverage types explained in plain language.

What Types of Business Insurance Do You Actually Need?

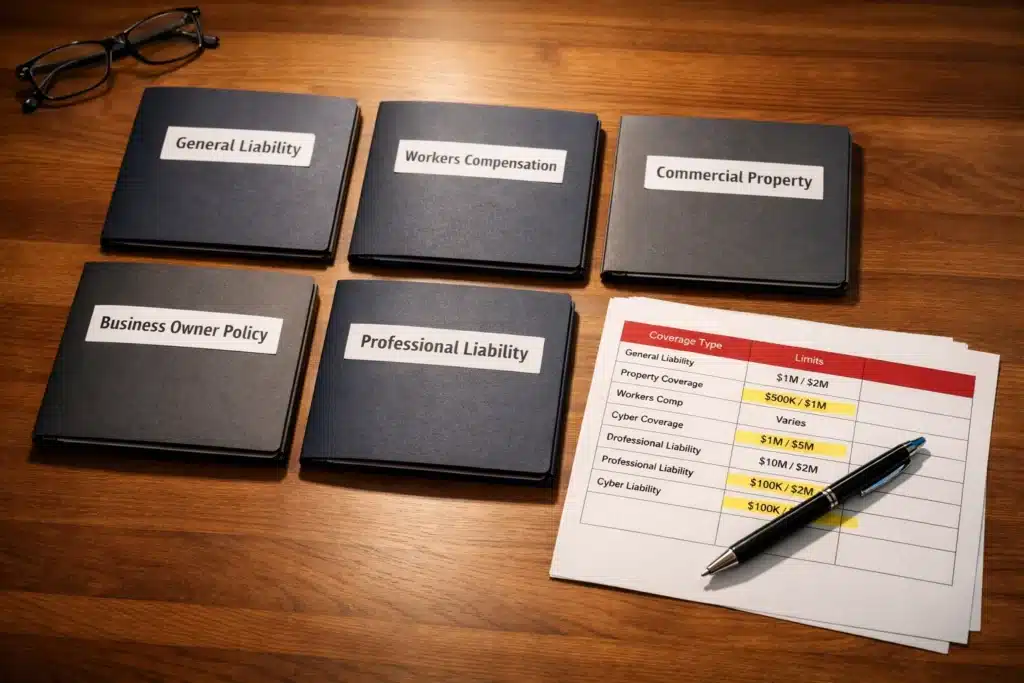

The six core coverage types most businesses need are general liability, commercial property, workers compensation, professional liability (E&O), a business owner’s policy (BOP), and cyber liability. Which ones apply to your business and at what limits depends on your industry, size, and risk profile. Skipping any of them based on cost alone is how claim disasters happen.

The U.S. Small Business Administration identifies the following federal requirements and common coverage types every business owner should understand before shopping for business insurance. The right combination depends on your operations, but the six below form the foundation of any sound commercial program.

General Liability Insurance

Covers bodily injury, property damage, personal injury, and false advertising claims. Any business that interacts with customers, vendors, or the public needs this. Learn more about how general liability insurance works and what it costs.

Workers Compensation Insurance

Required in nearly every state for businesses with employees. Covers medical costs and lost wages for employees injured on the job. Workers compensation is not optional. Operating without it exposes you to direct lawsuits and state penalties.

Professional Liability (E&O) Insurance

If your business provides advice, designs, services, or expertise of any kind, you need errors and omissions coverage. General liability does not cover professional mistakes. That gap has ended businesses that assumed they were fully protected.

Commercial Property Insurance

Covers your building, equipment, inventory, and physical assets against fire, theft, vandalism, and weather. Buying at actual cash value instead of replacement cost is one of the most expensive mistakes business owners make. See how commercial property insurance works for small businesses.

Business Owner’s Policy (BOP)

Bundles general liability and commercial property into a single, cost-effective package. Most low-to-moderate risk small businesses qualify, and a BOP typically costs less than buying the coverages separately. Read our breakdown of what a BOP policy actually covers.

Cyber Liability Insurance

Data breaches, ransomware, and phishing attacks are not exclusive to large enterprises. Any business that stores customer data, processes payments, or relies on technology is exposed. Explore The Coyle Group’s cyber insurance hub to understand what is covered and what is not.

Coverage Type |

Who Needs It |

What It Covers |

|---|---|---|

|

General Liability |

All businesses |

Bodily injury, property damage, slander |

|

Workers Compensation |

All businesses with employees |

Employee injuries, medical costs, lost wages |

|

Commercial Property |

Businesses with physical assets |

Building, equipment, inventory |

|

BOP |

Small to mid-size, low-medium risk |

GL + property bundled |

|

Professional Liability |

Service and advice businesses |

Errors, omissions, malpractice |

|

Cyber Liability |

Any business using technology |

Data breaches, ransomware, business interruption |

|

Umbrella / Excess |

Businesses with significant assets |

Additional limits above primary policies |

Ready to find out which coverages your business actually needs? Our team will walk through your specific situation at no pressure.

How Much Does Business Insurance Cost?

Business insurance costs vary significantly by industry, revenue, payroll, claims history, and location, which is exactly why online quote tools produce numbers that rarely match reality. Here are the benchmarks most business owners are working with when shopping for business insurance in 2025.

Premiums have risen approximately 12% since 2022, driven by inflation, rising claim costs, and a tighter underwriting environment. This makes annual policy reviews more important than ever. What was adequate coverage two years ago may now be underinsured.

Factors that drive your premium up or down:

What Are the Most Common Mistakes Business Owners Make When Shopping for Business Insurance?

The most costly mistakes when shopping for business insurance are not about picking the wrong carrier. They are about structuring the wrong coverage. Underinsurance is invisible until a claim, and by then there is nothing to fix. Here are the six mistakes that create the most expensive surprises.

Mistake 1: Actual Cash Value Instead of Replacement Cost

Depreciation will decimate your payout. A $200,000 piece of equipment with 10 years of depreciation may be settled at $60,000, leaving you $140,000 short of getting back to operational.

Mistake 2: Using Outdated Property Values

If you have not updated your commercial property values since 2019 or 2020, you are almost certainly underinsured. Construction costs have increased dramatically. Your policy limit needs to reflect today’s replacement cost, not what you paid years ago.

Mistake 3: Ignoring Cyber Exposure

“We are too small to be a target” is the most expensive sentence in small business insurance. Most cyberattacks target small businesses precisely because their defenses are weaker.

Mistake 4: Choosing the Lowest Price Without Comparing Terms

Two policies with the same limit can perform completely differently in a claim. Exclusions, sub-limits, and conditions matter as much as the premium. Shopping for business insurance on price alone is like buying a car based only on color.

Mistake 5: Not Reviewing Coverage After Business Changes

Adding employees, buying equipment, expanding locations, or changing operations all affect your coverage needs. Policies do not update themselves. A change in your business that is not reflected in your policy is a coverage gap waiting to happen.

Mistake 6: Using Multiple Competing Brokers

This feels like a smart negotiating tactic. It is not. Three brokers submitting your account to the same markets simultaneously flags your account as “shopped,” reduces carrier appetite, and turns the transaction into a price war. No broker is spending the time needed to build your program correctly.

Concerned about gaps in your current coverage? Our team will give you a straight answer.

How Do You Choose the Right Insurance Broker?

The right broker for shopping for business insurance is one who asks more questions than they answer in the first meeting, who works with multiple carriers so they can actually shop the market for you, and who will tell you when your business is a poor fit for their expertise. A broker who is primarily interested in closing a sale is structurally misaligned with your interests.

Questions to ask any broker before you engage:

The commissions brokers earn are paid by insurance carriers, not by you. That structure is not inherently a problem, but it means asking the right questions upfront matters. A good broker will welcome that conversation.

What Are the 4 Steps to Buy Business Insurance the Right Way?

The SBA outlines four steps for buying business insurance that hold up in practice: assess your risks, find a reputable licensed agent, shop around with that agent’s guidance, and reassess every year. The practical version of this process looks like this.

Step 1: Map Your Risks First

List your physical assets, payroll, employee count, services provided, and any contracts that specify required coverage minimums. Do this before you talk to anyone.

Step 2: Work With One Independent Broker

Give one qualified broker your complete picture and let them build a program across multiple carriers. An independent broker has no loyalty to any single insurance company.

Step 3: Compare Programs, Not Just Prices

Ask for side-by-side comparisons of what is covered, what is excluded, limits, and deductibles. A lower premium with narrower coverage is not a better deal.

Step 4: Review Every Year Without Exception

Schedule an annual review call with your broker 90 days before renewal. Not at renewal. Your business changes, and your coverage needs to keep pace.

Real-World Example: Why Annual Reviews Matter

A mid-size service business in New York had not updated its commercial property values in five years. After a fire loss, they discovered their insured value was 40% below replacement cost. A coinsurance penalty cost them over $180,000 out of pocket on top of the loss itself. An annual review would have caught it before the claim.

Let us do this work for you. We will handle the review, the shopping, and the comparison so you do not have to.

Frequently Asked Questions About Shopping for Business Insurance

Common questions about shopping for business insurance come down to three themes: how much coverage you need, how much it costs, and how to find the right broker. Here are the most frequent questions we hear from business owners.

The Bottom Line on Shopping for Business Insurance

Shopping for business insurance does not need to be a frustrating exercise in comparison shopping across websites that cannot understand your business. The process works when you treat it as a professional advisory relationship.

One where a qualified independent broker earns your trust by asking the right questions, explaining your options clearly, and putting together a program built around your actual risks. The statistics are clear: most business owners are underinsured, underprepared, and unsupported when it comes to insurance. You do not have to be one of them.

About the Author

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.