TLDR. Key Takeaways

Why Your Claims Keep Repeating. And What Root Cause Analysis Does About It

Root Cause Analysis (RCA) works by systematically asking “why” until you reach the true origin of a problem, not just the surface trigger. Most businesses never get past the first “why”, and that is exactly why the same workers’ compensation claims show up year after year, driving premiums higher with no end in sight.

The instinct to call something “just an accident” is understandable. But in the context of workers’ compensation insurance, it is one of the most expensive habits a business owner can develop. Every unexamined claim is a future claim waiting to happen.

The Accountability Gap That Costs You

When leadership consistently chalks injuries up to bad luck, two things happen in parallel. The same hazards stay in place, generating repeat claims year after year. And your experience modification factor climbs, raising your premiums with it.

Root Cause Analysis closes that gap. It shifts the conversation from “who is to blame” to “what went wrong and why”, and more importantly, “what do we change so it never happens again.”

What Is Root Cause Analysis in Workers’ Compensation?

Root Cause Analysis is a structured investigation method that identifies the underlying cause of a workplace incident – not just the immediate trigger. In workers’ compensation, it targets the systemic conditions that generate recurring injuries, eliminating the problem before it produces another claim.

RCA is not about blame. Think of it the way a doctor approaches diagnosis: the symptom is not the disease. The conditions that created the symptom are the disease. According to the OSHA Safety Pays program, workplace injuries have a direct, measurable impact on profitability – and the financial case for prevention becomes clear once the real numbers are laid out.

How Insurers and Risk Managers Apply RCA

Industries Where RCA Delivers the Strongest Results

How the 5 Whys Method Works in Insurance Claims

The 5 Whys technique drives down to the root cause of any incident by asking “why” five times in sequence. Each answer becomes the basis for the next question. By the fifth answer, you have reached the systemic cause, the one that, when corrected, prevents recurrence across the whole operation. It requires no special software and can be conducted by any trained manager or safety professional.

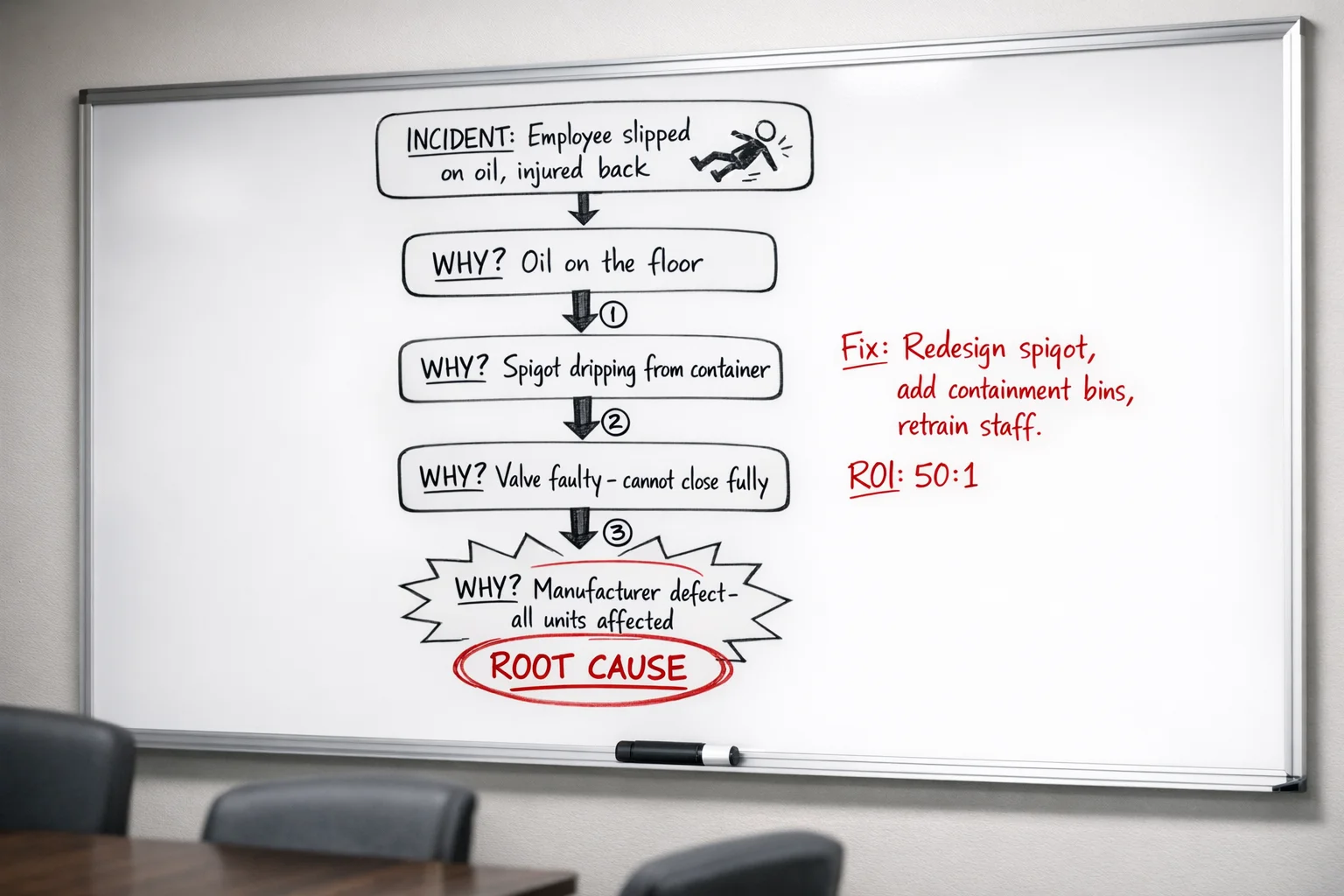

Real-World Example: Slip and Fall at a Food Manufacturing Plant

An employee slipped on a cement floor and injured their lower back, one of the most expensive categories of workers’ compensation claims. The initial explanation was simple: “It was an accident.” Root Cause Analysis told a very different story.

Why? |

Answer |

|---|---|

|

Why did the employee slip? |

Oil was on the floor |

|

Why was there oil on the floor? |

A spigot was dripping from a bulk storage container |

|

Why was the spigot dripping? |

The valve could not be closed tightly |

|

Why could the valve not close? |

It was faulty and difficult to turn fully shut |

|

Why was the valve faulty? |

Root cause: Every spigot from this supplier had the same manufacturing defect |

Conducting a thorough workplace incident investigation is the foundation that makes Root Cause Analysis produce lasting results. Without a complete investigation, you are guessing at causes rather than identifying them.

The Financial Case for Root Cause Analysis

Root Cause Analysis converts a reactive cost into a proactive investment. The CDC’s National Institute for Occupational Safety and Health (NIOSH) estimates that workers’ compensation and medical expenses associated with workplace falls alone cost U.S. businesses $70 billion annually. That figure excludes indirect costs: lost productivity, replacement labor, management investigation time, and premium increases that follow every claim.

The 50:1 ROI From One Corrective Action

Cost Category |

Amount |

|---|---|

|

Average workers’ comp slip-and-fall claim |

$150,000 |

|

Indirect costs (productivity loss, retraining, premium impact) |

~$38,000 |

|

Total exposure avoided |

~$188,000 |

|

Spill containment bins |

$1,300 |

|

Extra cleaning and maintenance |

$2,500 |

|

Total prevention investment |

$3,800 |

|

Return on investment |

50:1 |

Why Claim Frequency Damages Premiums More Than Severity

Most business owners worry about catastrophic claims, the large, rare events. But claim frequency drives the experience modification factor harder than severity does. A business with three moderate claims is penalized more aggressively than one with a single large claim of the same total dollar value.

Understanding what indirect loss costs actually represent changes how you view every small, preventable incident. A $12,000 sprained wrist claim is not trivial, it signals a systemic hazard that Root Cause Analysis can eliminate before it becomes a $150,000 back injury.

What Corrective Actions Come Out of Root Cause Analysis?

Root Cause Analysis does not just identify problems; it generates specific, layered corrective actions that address each level of the 5 Whys chain. From the food manufacturing example, five actions came out of a single investigation.

Spigot Redesign

The manufacturer was pushed to redesign the component, eliminating the defect at the source for all future containers used at the facility.

Containment Bins

Spill containment bins were added beneath all bulk storage containers to catch any drips before they reached the floor and created a hazard.

Storage Relocation

Bulk oil storage was moved away from high-traffic employee walkways, eliminating the overlap between spill risk and employee movement patterns.

Maintenance Protocol Update

Cleaning schedules were updated to include regular inspection and sign-off on all spigot areas, catching future drip issues before they accumulate on the floor.

Employee Spill Training

Staff were trained to report small spills immediately and clean minor leaks themselves before they become floor hazards requiring full maintenance response.

How Root Cause Analysis Reduces Your Workers’ Comp Premiums

Root Cause Analysis is not just a safety practice; it is a premium reduction strategy with a direct, measurable mechanism. Every time RCA eliminates a recurring claim driver, it lowers the frequency number that feeds your experience modification factor calculation.

The Experience Modification Factor Connection

Your experience modification factor (EMF) compares your actual claim history over the past three years to the expected history for a business of your size and industry. An EMF above 1.0 means your claims are worse than average; your premium reflects that. An EMF below 1.0 means you are performing better than the benchmark, and carriers reward that with lower rates.

RCA directly reduces the numerator in that calculation: your actual claims. Businesses that investigate every recordable incident and apply corrective actions consistently typically see meaningful EMF improvement within two to three years. The math is straightforward; it just requires discipline. Reviewing the most common workers’ compensation mistakes shows just how much premium is being overpaid by businesses that skip this step.

The Broader Business Case Beyond Premiums

How to reduce your workers comp experience mod – what actually moves the number

Frequently Asked Questions About Root Cause Analysis

Author’s Expertise

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.