Contractors Pollution Liability Insurance

What It Covers, What It Excludes, and How to Buy It

Contractors Pollution Liability Insurance Explained in 4 Minutes.

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

If you’ve ever been asked for “pollution coverage” on a certificate of insurance, this is what they mean.

For example, one fuel spill during excavation. One odor complaint from roofing fumes. One concrete washout into a storm drain. Any of these can trigger cleanup costs exceeding $100,000, legal defense fees, and job shutdowns.

The Bottom Line (TL;DR)

Contractors pollution liability (CPL) insurance pays for cleanup costs, legal defense, and damages when your construction work causes pollution problems. Here are the key facts:

Have a contract requiring CPL coverage? Contact us today to get a quote that matches your exact requirements.

What Is Contractors Pollution Liability Insurance?

Contractors Pollution Liability insurance pays for cleanup costs, legal defense, and damages when your construction work causes pollution problems that general liability insurance won’t cover.

For a broader breakdown of what pollution liability coverage protects, including how policies are structured by operation type, see our complete coverage guide.

Specifically, What counts as “pollution”:

Key misconceptions:

Who Actually Needs Contractors Pollution Liability?

High-risk contractor types:

When Contracts Will Require CPL

Specifically, you’ll need to provide proof of coverage when:

What 40+ Years Taught Me About This Risk

However, the contractors who succeed understand that CPL isn’t optional once you’re working near sensitive sites.

The difference becomes clear when a spill happens: one group calls their insurer, the other scrambles for emergency funding while facing regulatory penalties.

Just as workers compensation insurance addresses employee injury risks, CPL handles environmental liability exposures.

Do you fit one of these high-risk categories? Book a consultation to discuss your specific pollution exposure and coverage options.

What Does Contractors Pollution Liability Actually Cover?

Let’s break down the core coverage components:

1. Cleanup Costs (Usually the Largest Expense)

Even small spills can run $10,000–$100,000+ once you factor in response, disposal, testing, and oversight, depending on material and location.

2. Legal Defense

Defense “inside” vs “outside” the limit:

3. Bodily Injury & Property Damage from Pollution

4. Transportation Coverage (If Included)

5. Non-Owned Disposal Site (If Included)

What CPL Usually Doesn’t Cover

Common exclusions:

Need to verify your policy covers gradual pollution or mold claims? Book a consultation to review your specific policy language.

CPL vs Pollution Endorsement: What’s the Difference?

Simple rule: If contracts require pollution coverage or you work near waterways/sensitive sites, you need a standalone CPL. A general liability endorsement usually won’t pass.

Occurrence vs. Claims-Made CPL: Which Should You Choose?

CPL policies are available on either an occurrence or claims-made basis. Occurrence policies cover incidents that happen during the policy period regardless of when the claim is reported, providing permanent protection for past work without needing tail coverage. Claims-made policies only respond if the claim is reported while the policy is active. For most contractors with ongoing operations, occurrence-based CPL is the stronger choice.

CPL is also available as an annual “practice policy” covering all your operations, or as a project-specific policy for contractors who only occasionally need coverage.

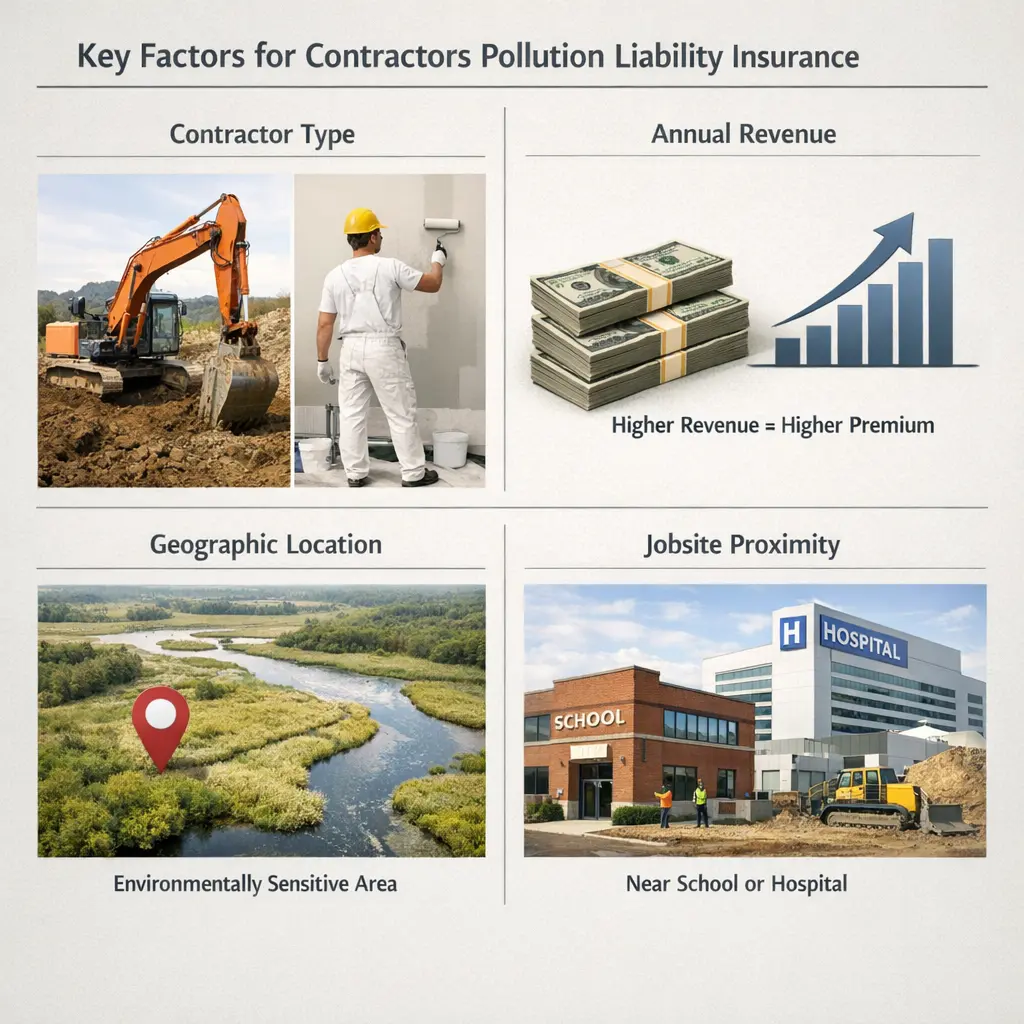

How Much Coverage Do Contractors Actually Need?

Start With Contract Requirements

Critical: Review insurance exhibits in contracts before you bind coverage. Verify that your policy actually provides the required wording.

Risk Factors That Increase Your Exposure

Calculate Your Realistic Worst-Case

Example: Diesel spill during excavation

Even minor incidents easily reach $75,000–$100,000. A $1M limit seems less excessive when you run these numbers.

Real-World Example: When $1M Almost Wasn’t Enough

A mechanical contractor punctured an underground fuel tank during HVAC excavation. The tank had been abandoned decades earlier, but still contained residual petroleum.

Actual costs incurred:

Their $1M policy covered it, but if groundwater contamination had spread further, they would have faced exposure beyond their limit. This contractor now carries $2M limits.

Most Common Contractor Pollution Claims

1. Fuel Tank Punctured During Excavation

What happened: Excavator struck unmarked underground fuel storage tank

Typical costs: $100K–$400K for soil removal, groundwater testing, regulatory reporting, property damage claims

Prevention strategies:

2. Hydraulic Line Failure

What happened: Hydraulic hose burst, releasing fluid into storm drain

Typical costs: $25K–$75K for drain cleaning, water treatment, municipality fines, environmental testing

Prevention strategies:

3. Concrete Washout Into Storm Drain

What happened: Concrete truck driver washed chute near drain; pH-altered water entered waterway

Typical costs: $15K–$100K+ including potential EPA or state fines, waterway testing, and remediation. The EPA actively enforces Clean Water Act violations, with civil penalties that can escalate significantly depending on violation severity and duration.

Prevention strategies:

4. Roofing Fumes Trigger Complaints

What happened: Hot tar fumes entered neighboring building’s HVAC; tenants complained of illness

Typical costs: $50K–$150K for ventilation cleaning, tenant relocation, legal defense, bodily injury claims

Prevention strategies:

5. Solvent Fumes From Flooring

What happened: Adhesive fumes migrated to adjoining offices; employees reported illness

Typical costs: $30K–$100K for air quality testing, HVAC cleaning, tenant business interruption, medical evaluations

Prevention strategies:

6. Sewage Spill During Utility Work

What happened: Contractor damaged sewage line; sewage contaminated adjacent property

Typical costs: $40K–$200K for sewage cleanup, property decontamination, temporary bypass, health department oversight

Prevention strategies:

Seeing your operations in these examples? Book a call to discuss prevention strategies and proper coverage for your specific risks.

Certificates of Insurance: What You Need to Know

What Owners Require on Contractors’ Pollution Liability Certificates

Certificates of insurance must show:

How to Avoid Certificate Failures That Kill Project Starts

The problem: You sign a contract requiring specific CPL coverage, buy a policy, then discover your certificate doesn’t match the owner’s exhibit. Project start gets delayed while you scramble to fix what’s often unfixable without changing policies entirely.

The solution 5 preventive steps:

1. Send insurance exhibit to broker BEFORE binding

Don’t wait until after you’ve purchased coverage. Give your broker the project’s insurance requirements during the quote process so they can find carriers that can actually meet the specifications.

2. Ask the critical question

“Can we provide a certificate and endorsements exactly as this exhibit requires?” If your broker hesitates or says “probably,” that’s a red flag.

3. Get samples for owner pre-approval

Request sample certificates and draft endorsements showing exactly how coverage will appear. Send these to the project owner’s risk manager for approval before you bind the policy.

4. Verify endorsements are actually added

Policies don’t automatically include endorsements. Confirm with your broker that additional insured, primary and noncontributory, and any other required endorsements are:

5. Don’t assume GL endorsements pass

A pollution endorsement on your general liability policy is almost never equivalent to standalone CPL. Project owners know the difference and will reject inadequate coverage.

Understanding Additional Insured on Contractors Pollution Liability

What it provides

When you name a project owner or GC as additional insured on your CPL policy, they’re covered under your policy for pollution claims arising from your work. This gives them defense and indemnity if they’re sued alongside you.

Why owners require it

It’s a risk transfer mechanism. If pollution from your work causes a claim, your insurance protects them rather than forcing them to use their own coverage or pay out of pocket.

Two endorsement types:

Scheduled additional insured:

Blanket additional insured:

Important limitations:

Primary and Noncontributory Language Explained

Project owners want your insurance to pay first, before theirs.

Without this language

If a pollution claim involves both you and the owner, insurance companies could argue about which policy should pay and in what proportion. This creates delays and coverage disputes.

With primary and noncontributory language

Most CPL policies can add this language via endorsement, but always verify before binding coverage.

What Drives Contractors Pollution Liability Costs (and How to Lower Them)

Pricing You Can’t Change

Cost Levers You Control

1. Written spill response plan + onsite spill kits

Savings: 5–15% premium reduction

2. Employee training documentation

Regular environmental awareness training reduces rates

3. Equipment maintenance logs

Hydraulic inspections, fuel tank tests, service records

4. Subcontractor requirements

Hold harmless agreements + their own CPL coverage

5. Claims history

Clean loss history = biggest cost control

Typical Annual Premiums

According to NAIC market data, environmental liability premiums have stabilized as contractors implement stronger risk management.

Ready to implement safety programs that reduce your rates? Contact our team for guidance on what insurers actually reward.

How to Buy Contractors Pollution Liability Without Overpaying

6-Step Process

1. Gather contract requirements

2. Document your top 5 risk scenarios

3. List materials that could cause pollution

4. Choose coverage structure

5. Select limits and deductible

6. Verify certificate wording BEFORE binding

Quick Contractor Pollution Liability Checklist

Coverage Verification:

Contract Compliance:

Claims Readiness:

Subcontractor Management:

Don’t want to navigate this alone? Contact The Coyle Group, we’ll handle the entire process from quote to certificate.

Questions about Contractors Pollution liability?

Next Step: Get the Right Coverage Before You Need It

Contractors pollution liability isn’t something you want to think about after a spill happens. If you’re bidding projects that require CPL, working near waterways or sensitive sites, or using materials that could cause environmental harm, securing coverage now prevents expensive surprises later.

At The Coyle Group, we help contractors:

Don’t wait until you’re scrambling to get a certificate three days before project start. Most CPL policies take 2-4 weeks to bind once underwriters review your operations.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping contractors navigate complex insurance requirements, secure appropriate coverage, and build risk management programs that protect their operations while controlling costs.

Discuss your specific operations and get customized recommendations

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?