What is a Certificate of Insurance? Your Essential Guide to COIs and Additional Insured Status

A Certificate of Insurance (COI) is a standardized one-page document that proves what liability coverages you carry. The form, commonly known as the ACORD 25, was developed by ACORD (Association for Cooperative Operations Research and Development), a non-profit organization responsible for standardizing insurance forms across the industry.

Before ACORD standardization in the 1970s, every insurance company used different formats. Now, when you receive an ACORD 25 certificate, you get consistent formatting regardless of which insurer issued it.

The Bottom Line

What 40+ Years Taught Me About This Risk

Certificate holders often place too much faith in COIs without understanding their limitations. The most successful business owners treat certificates as snapshots, valuable for verification at a specific moment but never as substitutes for actual insurance policies. They verify endorsements, understand coverage triggers, and maintain proper documentation throughout project lifecycles.

Understanding the Critical Limiting Language

A certificate only illustrates liability coverages. The top header on every ACORD 25 Form states: “This certificate is issued as a matter of information only and confers no rights upon the certificate holder.”

The header continues: “This certificate does not affirmatively or negatively amend, extend, or alter the coverage afforded by the policies below. This certificate of insurance does not constitute a contract between the issuing insurers, authorized representative, or producer, and the certificate holder.”

Many certificate holders mistakenly rely on a cert as definitive proof of insurance. While a cert proves insurance at the moment of issuance, policies can be canceled, terminated, or altered at the next moment.

Who Needs a Certificate of Insurance?

General Contractors and Project Owners

Construction contracts require specialty contractors to maintain minimum insurance coverage levels. GCs or owners need proof of liability insurance before awarding contracts.

Commercial Landlords

Landlords require tenants to provide COIs showing adequate coverage to protect the property owner from claims arising from tenant operations.

Government Entities

Government contractors must maintain current insurance while working on projects, with requirements varying by agency and contract type.

Event Venues

Event organizers need certificates from vendors or venues, providing peace of mind to venue owners and ensuring adequate protection for all parties.

What Information Appears on a Certificate of Insurance?

Certificate Section |

Information Displayed |

Why It Matters |

|---|---|---|

|

Producer Information |

Insurance broker/agent name and contact |

Point of contact for questions or changes |

|

Insured Information |

Business name, address, policy details |

Must match contract exactly |

|

Insurance Carrier |

Company names and NAIC numbers |

Verifies financial stability of insurers |

|

Coverage Types |

General liability, auto, workers’ comp, umbrella |

Shows specific protections in place |

|

Policy Numbers |

Unique identifiers for each policy |

Enables verification with carriers |

|

Policy Dates |

Effective and expiration dates |

Confirms coverage during project timeline |

|

Coverage Limits |

Per occurrence, aggregate, other limits |

Ensures adequate protection levels |

|

Certificate Holder |

Entity requesting the certificate |

Identifies who receives notices |

|

Description |

Special provisions, additional insureds, waivers |

Documents specific contractual requirements |

Common Coverage Types on COIs

Commercial General Liability:

Commercial Auto Liability:

Workers’ Compensation:

Excess/Umbrella Liability:

Professional Liability:

Additional Insured Status: What You Need to Know

Certificate holders frequently request additional insured status. Understanding how it works is critical.

Two Ways to Grant Additional Insured Status

1. Blanket Additional Insured Endorsement

Many package policies and business owner policies automatically provide blanket additional insured endorsements. However, the language typically says the insurer will provide additional insured status only when required by written contract.

If there’s no contract between the parties mandating additional insured status, then no status is granted, regardless of what the certificate says.

2. Specific Policy Endorsement

Additional insured status can be granted by specifically endorsing the liability policy with the name of the requesting party. Unless an endorsement is issued, the negotiated risk transfer was not accomplished.

There may be an additional premium for this endorsement type.

The Scope Limitation Most People Miss

Additional insured endorsements grant status as an “insured” but only for the negligent acts or omissions of the named insured.

Additional insured status does NOT:

In the construction industry, contractors add property owners as additional insureds, protecting the owner from claims arising from the contractor’s work. This arrangement reduces disputes and ensures all parties have protection.

Understanding the high cost of liability claims explains why proper additional insured status matters.

Common Certificate of Insurance Mistakes

Mistake #1: Assuming the Certificate Provides Coverage

Mistake #2: Not Checking Certificate Holder Information

Mistake #3: Ignoring Policy Dates

Mistake #4: Believing Additional Insured Boxes Equal Coverage

Mistake #5: Using Templates Found Online

For businesses with multiple locations or complex operations, understanding wholesalers distributors insurance helps ensure certificates accurately reflect coverage.

State-Specific and Industry Requirements

New York Construction

New York’s construction laws are some of the most stringent in the country. Between Labor Law 240/241 (the Scaffold Law) and municipal insurance requirements, COIs are heavily scrutinized.

NYC requirements may include:

Minnesota Contractors

Minnesota general contractors must maintain general liability insurance with state-required minimum coverage of $50,000 per occurrence, though most carry $1 million per occurrence limits.

Additional Minnesota requirements:

California (Caltrans) Projects

Contractors must submit insurance documents when they are the apparent low bidder.

Required documentation includes:

How to Get a Certificate of Insurance

Step 1: Purchase Required Insurance Policies

Common policies for contractors and businesses:

Step 2: Contact Your Insurance Agent or Broker

Provide your agent with:

Good insurance providers issue certificates within 24 hours, with some issuing them in minutes.

Step 3: Review Before Submitting

Accuracy Checklist:

Step 4: Maintain Organized Records

Store COI documentation as long as your business exists. Organized records help with audits and distinguish between employee and independent contractor statuses.

Real-World Example: The $5 Million Coverage Gap

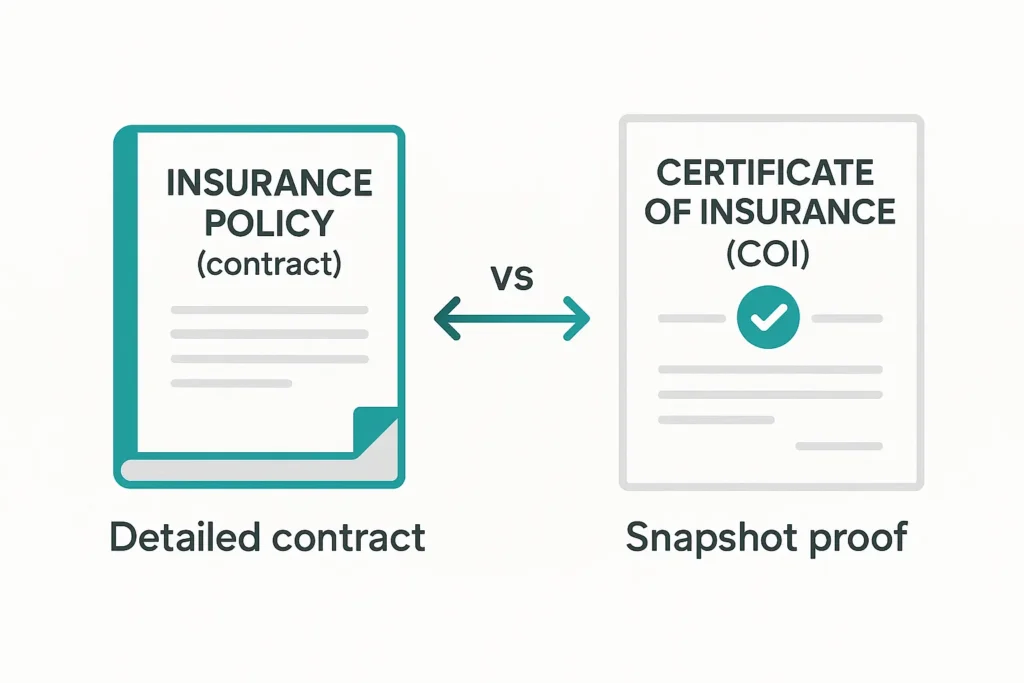

The Certificate vs. The Policy: Understanding the Difference

Certificate of Insurance |

Insurance Policy |

|---|---|

|

Summary document (1 page) |

Complete contract (20-50+ pages) |

|

Shows coverage exists |

Contains all terms, conditions, exclusions |

|

Does not create coverage |

Actual insurance contract |

|

Evidence for third parties |

Legal agreement with insurer |

|

Can be issued quickly |

Requires underwriting and approval |

|

Lists basic information |

Defines detailed coverage provisions |

|

No legal force |

Legally binding contract |

The actual insurance policy is a contract between your business and the insurance company, containing all pertinent information about what perils are covered and what you must do if a potential claim takes shape.

When disputes arise, courts look to the policy language, not the certificate, to determine coverage.

Industry-Specific Certificate Considerations

Technology Companies

Cyber insurance adoption among construction firms shot up by 26% in 2025, showing contractors are recognizing modern threats like data breaches and ransomware.

Technology companies should ensure COIs reflect:

Learn more about cyber insurance for technology startups.

Manufacturing and Distribution

Food distributors and manufacturers face unique exposures requiring specialized certificates showing:

Professional Services

Consultants, accountants, engineers, and other professionals should highlight:

Frequently Asked Questions

Good insurance providers issue COIs within 24 hours, with some issuing them in minutes if you have all required information ready. At The Coyle Group, we typically issue certificates within an hour of being requested, or faster if needed, but always by the end of the day.

Many insurance companies charge fees for each certificate copy. However, the cost of actual insurance coverage depends on numerous factors including your industry, revenue, claims history, and coverage types.

No. Only authorized insurance representatives can legally issue ACORD certificates. Using unauthorized templates may void your certificate and could impact your coverage in the event of a claim.

Request updated certificates whenever:

– Your insurance policies renew or change

– You begin a new project or contract

– A certificate holder requests updated information

– Your coverage limits increase

– You add or remove coverage types

– Business operations or locations change significantly

The certificate holder is simply the entity receiving the certificate as proof you have insurance. This status provides no coverage.

An additional insured is a party specifically added to your policy (via endorsement) who receives certain liability protection under your policy, typically only for claims arising from your work.

This depends entirely on your contract requirements. Many contracts require one party to name the other as an “additional insured” under its liability insurance policy. Unless an additional insured endorsement is issued, the negotiated risk transfer was not accomplished.

Always review your contract carefully and discuss requirements with your insurance broker before signing.

Even though a COI may expire, tracking those certificates holds value. An insurance claim can be filed many years into the future for an incident that occurred years in the past.

The evidence of insurance typically provides that no cancellation, lapse, or reduction of coverage will occur without 10 days prior written notice. This cancellation notice provision protects certificate holders by alerting them to coverage changes.

While some general contractors have their insurance cover subcontractors by including them as additional insureds, another option is for subcontractors to carry their own coverage. Having subcontractors maintain their own insurance typically provides better protection and prevents your loss history from being impacted by their claims.

Why Working with The Coyle Group Makes a Difference

What We Provide |

Your Benefit |

|---|---|

|

Expert guidance on contract insurance requirements |

No surprises or rejection of certificates |

|

Fast certificate issuance (typically within 1 hour) |

Never miss project deadlines |

|

Verification of additional insured endorsements |

Actual coverage, not just paper documentation |

|

Proactive renewal reminders |

Avoid coverage gaps |

|

Multi-carrier access |

Competitive pricing on quality coverage |

|

Claims advocacy |

Expert support when you need it most |

|

Ongoing policy reviews |

Coverage evolves with your business |

Our Approach to Certificates

We ensure certificates accurately reflect proper coverage that meets your contractual obligations. Our process includes:

Your Next Step

If you need Certificates of Insurance or want to verify your current coverage properly protects you, let’s connect. Many businesses discover coverage gaps only after problems arise, but proactive review prevents costly surprises.

Have questions about certificates or business insurance? Call us or schedule an appointment. We love working with business owners and look forward to chatting about your concerns.

Author’s Experience

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping businesses understand complex insurance requirements, navigate certificate demands, and secure comprehensive protection that supports their growth objectives.