Pollution Liability Coverage

What’s Actually Protected (And What’s not)

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

Your general liability claim was just denied. The reason? Pollution exclusion. Or maybe you’re bidding on a contract that requires pollution coverage you’ve never heard of. Either way, you’re discovering what thousands of business owners learn the hard way: standard insurance won’t protect you from environmental liability.

At The Coyle Group, we’ve helped hundreds of contractors, manufacturers, and property owners navigate this coverage gap. Pollution liability coverage isn’t optional for many businesses. It’s the difference between surviving an environmental claim and facing financial devastation.

The Bottom Line (TLDR)

If any of this sounds familiar, it’s worth a short conversation.

What Is Pollution Liability Coverage?

Pollution liability coverage is a specialized insurance policy that protects businesses from financial losses arising from pollution events, including the release, discharge, or escape of pollutants into the environment.

It covers third-party bodily injury, third-party property damage, environmental cleanup and remediation costs, legal defense expenses, and regulatory fines where insurable by law.

Businesses need this coverage because standard general liability and property insurance policies exclude pollution-related claims.

What Is Contractors Pollution Liability (CPL)?

Contractors Pollution Liability (CPL) is an insurance policy that protects contractors from claims arising from pollution incidents caused by their work at third-party job sites. CPL covers third-party bodily injury, property damage, cleanup costs, and legal defense for pollution events resulting from contracting operations, transportation of materials, and completed work. It does not cover pollution at locations the contractor owns or leases.

Who needs CPL:

What CPL covers:

What Is Pollution Legal Liability (PLL)?

Pollution Legal Liability (PLL) is an insurance policy that protects property owners and facility operators from claims arising from pollution conditions at, on, under, or migrating from locations they own, lease, or operate. PLL covers third-party bodily injury, property damage, on-site and off-site cleanup costs, and legal defense. Unlike CPL, PLL can often cover pre-existing contamination discovered after policy inception.

Who needs PLL:

What PLL covers:

Does General Liability Cover Pollution?

No. Standard general liability insurance does not cover pollution claims. The “absolute pollution exclusion” found in 98% of GL policies eliminates coverage for virtually any environmental event. According to the National Association of Insurance Commissioners (NAIC), many business owners mistakenly believe their general liability covers pollution, but it does not.

The only narrow exceptions in most GL policies are smoke from a hostile fire or fumes from a faulty HVAC system. Everything else falls outside your GL coverage:

For a deeper look at what your GL policy excludes, see our guide to general liability insurance exclusions.

If this exclusion surprised you, you’re not alone.

What Happens If I Don’t Have Pollution Liability Coverage?

Without pollution liability coverage, you pay all cleanup costs, legal fees, and damages out of pocket. Environmental claims typically range from $50,000 to $500,000+, and your general liability policy will deny the claim under the pollution exclusion.

Real-World Example: The Underground Tank Discovery

A general contractor excavating for a commercial foundation hits an abandoned underground storage tank. Contaminated soil spreads across the site and neighboring property. The contractor’s GL policy? Denied under the pollution exclusion.

Final cost without CPL coverage: $175,000 in cleanup, 6-week project delay, and a lawsuit from the neighboring property owner that settled for $85,000. Total exposure: $260,000. See more pollution insurance claims examples.

With a $1M CPL policy costing $2,800/year, the entire incident would have been covered minus deductible.

What Triggers a Pollution Liability Claim?

Pollution claims are triggered by the discovery of contamination, third-party complaints, regulatory enforcement, or lawsuits alleging pollution-related injury or damage. You don’t have to cause the pollution to face a claim. Property owners can be held liable for contamination from previous owners under federal Superfund law.

Common claim triggers include:

What Is the Difference Between CPL and PLL?

CPL covers contractors for pollution from their work at job sites they don’t own. PLL covers property owners for pollution at locations they own or lease. Contractors typically need CPL. Property owners need PLL. Some businesses need both.

Our manufacturing insurance and wholesalers and distributors insurance programs address industry-specific pollution exposures.

Is a GL Pollution Endorsement Enough?

A GL pollution endorsement may be sufficient for low-risk businesses, but it provides significantly less protection than standalone pollution liability coverage. Endorsements typically only cover “sudden and accidental” pollution with low sublimits ($25,000 to $100,000), while standalone policies cover both sudden and gradual pollution with limits of $1M or more.

A GL endorsement might be enough if:

A standalone policy is necessary if:

According to industry research, 9 in 10 insurance placements fail to meet contract pollution insurance specifications, even when the certificate of insurance claims the coverage exists.

If you’re on the fence, a short conversation can clarify it.

What Pollutants Am I Liable For?

You are liable for any substance that causes environmental damage when released, including common materials like fuel, dust, sewage, and even water in certain circumstances. Liability depends on your industry and operations.

Contractors (General, Excavation, Demolition):

HVAC/Plumbing Contractors:

Manufacturers:

Property Owners/Distributors:

How Much Does Pollution Liability Coverage Cost?

Pollution liability coverage costs $2,500 to $15,000 annually for most small and mid-sized businesses. According to Insureon, the median cost is $223 per month ($2,675/year). Costs vary based on business type, operations, location, and coverage limits.

What Do I Need to Get a Quote?

Most carriers need:

Timeline

You can typically get quoted in 24 to 48 hours. Binding coverage usually takes 3 to 5 business days once you accept a quote.

What Is the Difference Between Claims-Made and Occurrence Policies?

Claims-made policies cover claims reported during the policy period. Occurrence policies cover incidents that happen during the policy period, regardless of when the claim is filed. Most pollution liability policies are claims-made, which requires careful attention to retroactive dates.

What Is the Retroactive Date Trap?

Claims-made policies have a “retroactive date” that determines how far back coverage extends. If you switch carriers and the new policy has a later retroactive date, you lose coverage for incidents that occurred but weren’t discovered before that date.

Example

You’ve had CPL coverage since 2020 with Carrier A. In 2025, you switch to Carrier B, who sets your retroactive date as 2025. In 2026, a property owner discovers contamination from work you did in 2022. Neither policy covers you. Carrier A says the claim wasn’t made during their policy. Carrier B says the incident predates their retroactive date.

How to avoid this: When switching carriers, always negotiate to maintain your original retroactive date.

Learn more about tail coverage and how to protect yourself when changing carriers.

What Are the Red Flags When Comparing Pollution Liability Quotes?

Watch for sublimits that reduce coverage, exclusions for common pollutants, defense costs inside limits, and retroactive dates that create gaps. Not all pollution policies provide equal protection.

Sublimits that gut your coverage:

Exclusions that matter:

Questions to ask your broker:

What Are Standard Contract Requirements for Pollution Liability?

Most contracts require pollution liability with $1M to $5M limits, additional insured status, primary and non-contributory language, and waiver of subrogation. Project owners and general contractors increasingly audit these requirements.

Standard requirements include:

Project-Specific vs. Annual Policies:

Understanding waiver of subrogation requirements helps subcontractors meet contract specifications.

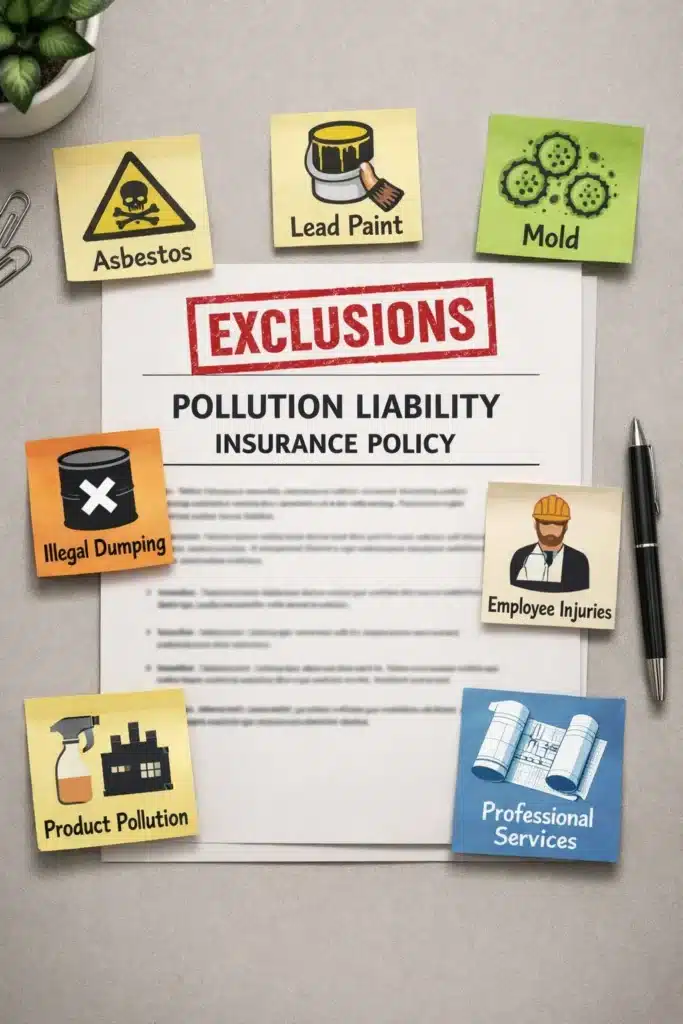

What Does Pollution Liability Coverage Exclude?

Pollution liability policies typically exclude intentional acts, known pre-existing conditions, employee injuries, and certain named pollutants unless specifically endorsed. Always review exclusions before binding coverage.

Common exclusions:

Have questions about how exclusions actually work in practice?

Questions about Pollution liability Coverage?

What 40+ Years Taught Me About This Risk

In four decades of helping businesses navigate insurance challenges, I’ve seen the same pollution coverage mistakes repeatedly. The businesses that avoid devastating environmental claims aren’t the ones who never face incidents. They’re the ones who have the right coverage when incidents happen.

The most common mistake: relying on a “limited pollution” endorsement when the contract requires standalone CPL. Project owners are auditing certificates more aggressively, and contractors are losing jobs over inadequate coverage.

At The Coyle Group, we access excess and surplus lines markets where most pollution coverage is written. We verify your coverage actually meets contract specifications in the policy language, not just on the certificate.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the United States, solving their insurance challenges. Gordon specializes in helping contractors, manufacturers, and property owners develop comprehensive pollution liability programs that protect their operations and support their growth objectives.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?