Pollution Liability Insurance Cost

What You’ll Pay, What Drives Price, and How to Lower It

How Much Does Pollution Liability Insurance Cost?

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

You just opened a bid package and saw “Contractors’ Pollution Liability” buried in the insurance requirements. Now you’re Googling to figure out what this coverage actually costs so you can decide if the job is worth it.

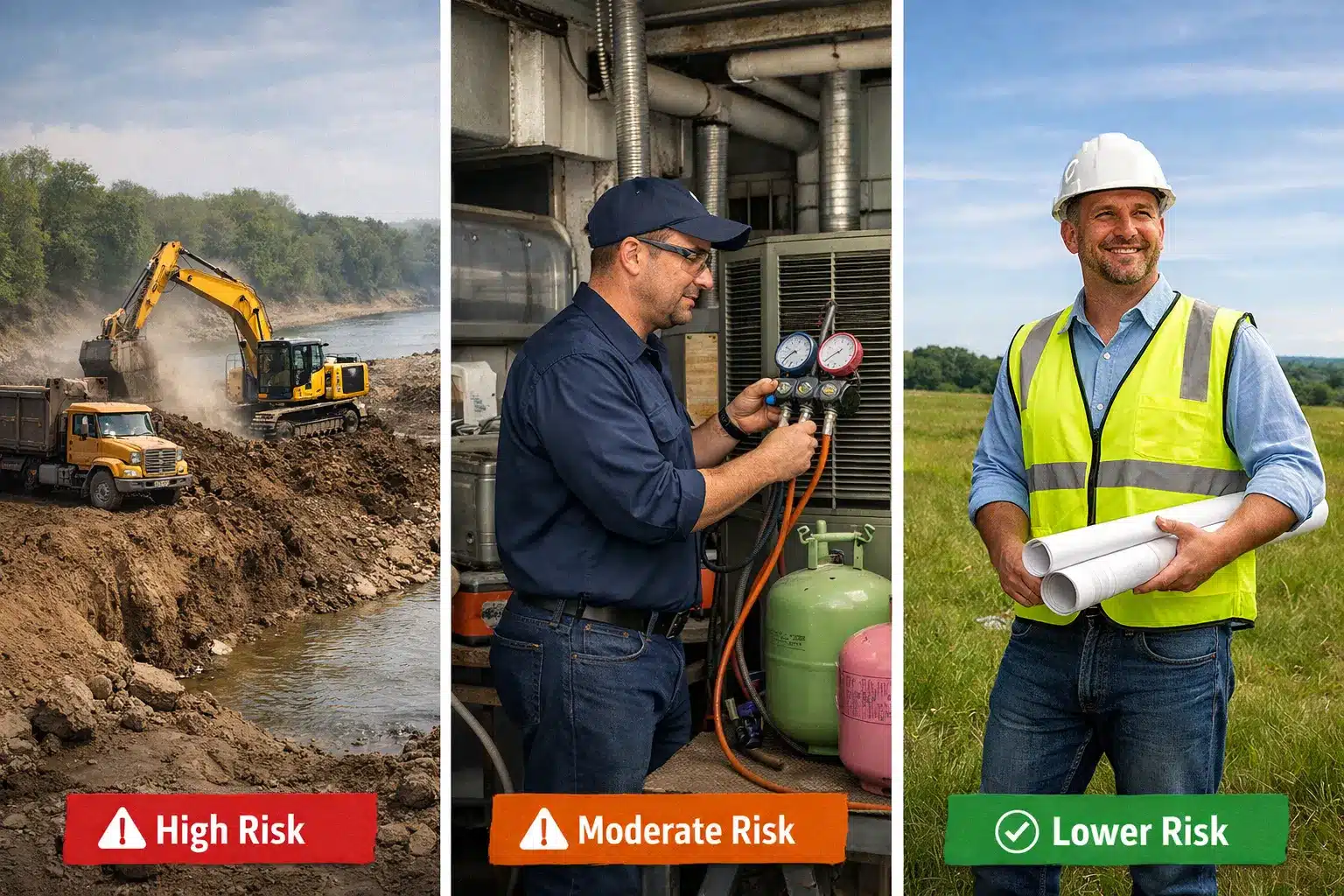

Here’s the straight answer: Pollution liability insurance cost typically ranges from $2,500 to $15,000 annually for most contractors, depending on what you do, where you work, and how much coverage the contract requires.

Lighter-risk trades often land in the lower end of that range, while high-exposure operations can exceed $20,000.

The range is wide because pollution risk varies dramatically across construction trades, and every carrier prices differently based on what they think could go wrong.

The Bottom Line (Key Takeaways)

How Much Does Pollution Liability Insurance Cost?

You got hit with an insurance requirement, and now you’re trying to budget it. You need a number that helps you decide whether to pursue the contract, adjust your bid, or walk away.

Here’s what contractors typically pay:

According to industry data, 38% of small businesses pay less than $150 per month ($1,800 annually), while the median sits at $223 monthly ($2,675 annually).

Why the Range is Wide

The spread exists because insurers price based on:

If you do excavation near waterways or handle refrigerants in schools, expect the higher end of these ranges. If you’re a general contractor managing subs on greenfield sites, you’ll likely land in the middle.

Quick Price Estimate

Want a ballpark for your situation? Consider these five factors:

Based on these factors, most contractors land between $3,000 and $18,000 annually.

Want exact pricing for your situation? We provide accurate quotes in 48-72 hours and handle all certificate of insurance requirements to satisfy contract exhibits fast.

Why is Pollution Coverage So Expensive Compared to General Liability?

Your general liability insurance typically costs $500 to $3,000 per year for similar limits. So why does pollution liability cost more?

Most GL policies exclude pollution entirely through the “absolute pollution exclusion” added in the 1980s. That means even if you think you’re covered, you’re not when pollution incidents happen.

The real reason for the cost difference

Cleanup expenses are mandated by government agencies, not negotiable settlements. A diesel spill can trigger $50,000 to $150,000 in cleanup costs before legal defense, third-party claims, or regulatory fines. According to EPA regulations, construction sites with one or more acres of land disturbance must comply with stormwater discharge requirements, and violations can carry penalties of tens of thousands of dollars per day.

The takeaway

Pollution insurance costs reflect catastrophic risk. One incident can bankrupt a contractor.

Learn more about general liability insurance coverage limits and how they compare.

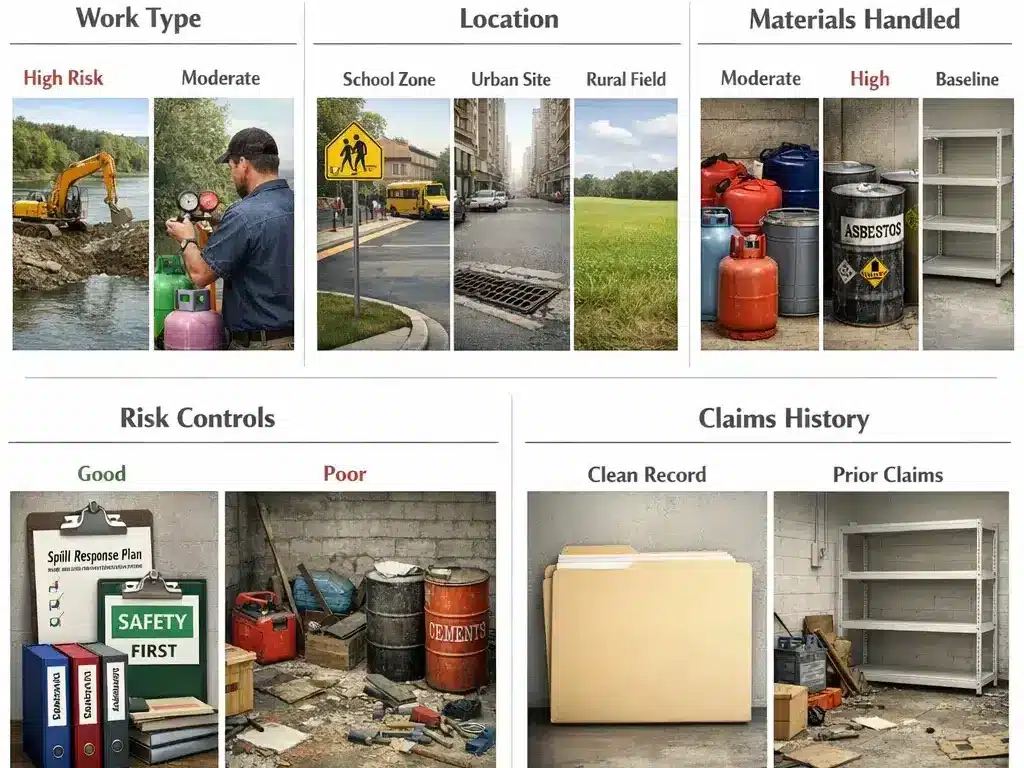

What Are Insurers Actually Pricing When They Quote This?

When you submit an application, underwriters build a risk model of how likely a pollution event is and how expensive it could get.

What Underwriters Evaluate

What 40+ Years Taught Me About This Risk

The contractors who understand what underwriters are pricing get better rates. If you can show documented safety programs, equipment maintenance, and subcontractor controls, you’ll consistently beat contractors who just fill out applications without context.

What Factors Raise Your Premium the Fastest?

Let’s be direct about what moves the needle on pollution liability insurance cost.

Biggest Premium Drivers

Type of Operations (Major Impact)

These trades consistently pay more:

Jobsite Sensitivity (Substantial Impact on Premium)

Work in these locations drives premiums up:

According to EPA stormwater regulations, construction sites must maintain buffers around surface waters to reduce downstream impacts. Failing to comply adds both regulatory risk and insurance cost.

History of Losses or Regulatory Issues (Severe Impact)

See real pollution insurance claims examples to understand how incidents impact pricing.

Higher Limits or Broader Coverage (Incremental Increases)

Multiple Locations or Multi-State Work (Moderate Impact)

Subcontractor Exposure (Can Vary Significantly)

If you’re responsible for subcontractor work:

The good news? Understanding these drivers lets you know which factors you can control (safety programs, sub management) to reduce pollution liability insurance cost and which are just the cost of doing business (trade type, jobsite location).

What Lowers the Cost (Without Gutting Coverage)?

You can’t change your trade or magically move jobsites away from water. But you can control how underwriters view your risk management, which directly impacts pollution liability insurance cost.

Practical Cost-Reduction Checklist

Let’s talk about the two levers you can pull when getting quotes: how much coverage you buy (limits) and how much you pay out-of-pocket before insurance kicks in (deductible).

Coverage Limits

Most contracts require $1M to $5M per occurrence. Here’s how premiums typically scale:

Rule-of-thumb budgeting framework:

For example: If you’re doing $2M excavation contracts near luxury homes or commercial developments, carrying only $1M in coverage means a single major claim could exhaust your policy and expose your business assets.

Deductibles

Contractors pollution liability policies typically offer deductibles from $2,500 to $25,000. Here’s how it works:

Don’t Do This

Don’t buy a huge deductible you can’t actually fund mid-project.

I’ve seen contractors choose $25,000 deductibles to save $2,000 on premium, only to face financial strain when a $75,000 claim hits and they need to come up with $25K immediately before the carrier pays anything.

Better approach

Choose a deductible you could write a check for tomorrow without disrupting payroll, subcontractor payments, or material purchases.

→ Read about commercial insurance deductibles and how they impact your financial planning.

Is Claims-Made Cheaper and What’s the Hidden Cost?

You’ll see two policy structures: claims-made and occurrence.

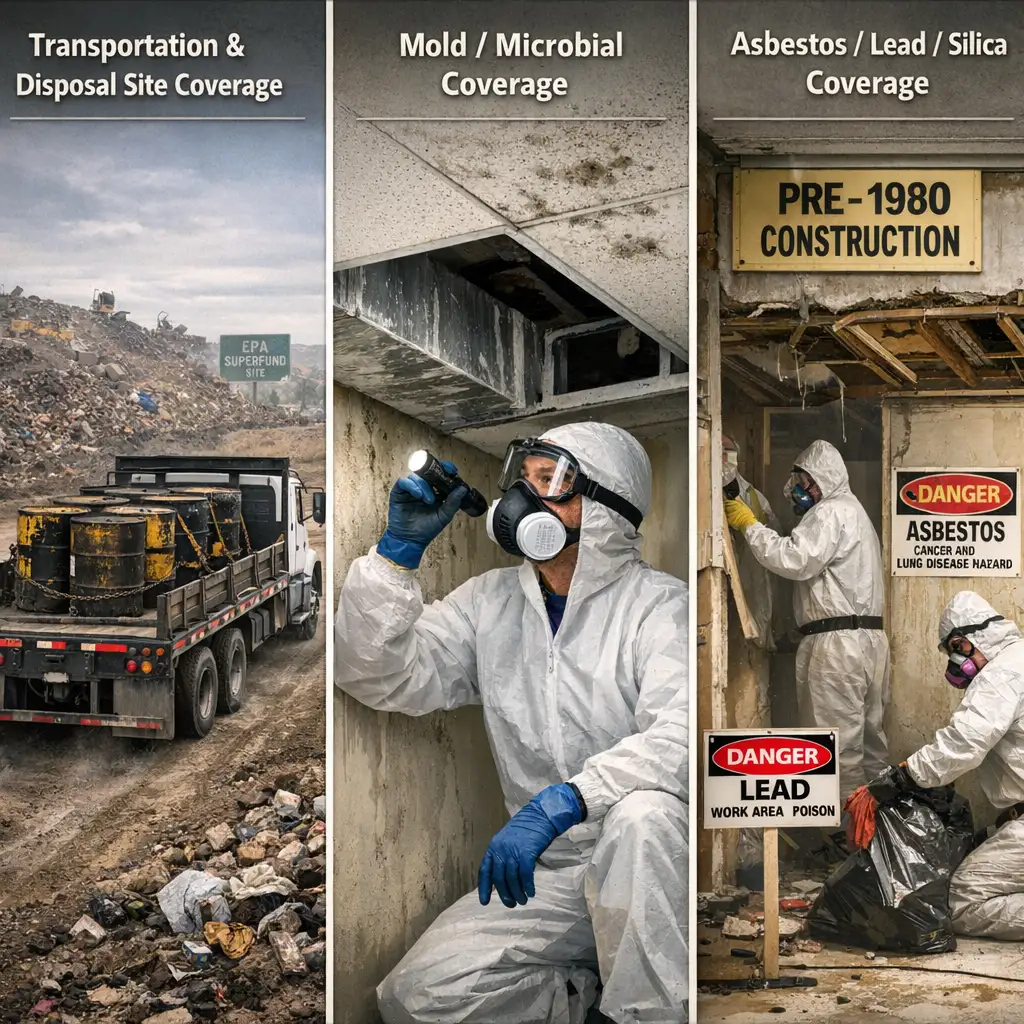

What Add-Ons Move the Price (and When You Actually Need Them)?

Standard CPL policies cover jobsite pollution. Most contractors need additional endorsements:

Why Two Quotes Differ

If you get quotes of $4,500 and $8,000, ask: Does it include transportation? Disposal sites? Gradual pollution or only sudden/accidental? Mold coverage? What deductible? These differences explain pricing gaps. Learn more about coverage options in our pollution liability insurance complete guide.

What Does a ‘Normal’ Quote Look Like by Business Type?

Let’s get specific. Here’s what contractors in different trades typically pay, based on industry data and our experience working with contractors nationwide.

Premium Ranges by Trade

Light Consulting / Office-Only Operations

General Contractor Managing Subs

HVAC/Mechanical Contractors

Roofing/Coatings Contractors

Excavation/Site Work Contractors

Manufacturing/Facility Runoff Exposure

Environmental Remediation Specialists

These ranges assume:

If you’re outside these parameters (higher limits, multi-state, significant sub exposure), expect adjustments.

What Documents Do You Need to Get an Accurate Cost Fast?

Speed matters when you’re under a bid deadline. Here’s what to have ready before you request quotes so you can get accurate pricing in days, not weeks.

Quote-Ready Checklist

Contract Insurance Exhibit (If Any)

Description of Operations + % of Revenue by Type

Typical Jobsites + Any Near Water

Past 5 Years of Claims/Incidents (If Any)

Subcontractor Controls / Certificates Process

Any Environmental Plans Already in Place

The more documentation you provide upfront, the faster underwriters can quote and the better pricing you’ll receive.

How Do You Avoid Overpaying for Pollution Liability Insurance?

After four decades helping contractors, I’ve seen the same mistakes repeatedly. Here’s how to avoid them:

→ Learn about reducing general liability costs for additional savings strategies.

Questions About Pollution Liability Insurance Cost

Ready to Get Pricing That Makes Sense?

If you’re bidding on projects requiring pollution liability, let’s talk.

What makes The Coyle Group different:

To discuss your requirements.

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners across the US, solving their insurance challenges. Gordon specializes in helping contractors develop comprehensive insurance programs that protect their operations without unnecessary complexity or cost.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?