Estimated reading time: 14 minutes

Employment Practices Liability Insurance Essentials

- What it covers: Employment Practices Liability Insurance (EPLI) protects businesses from employee-related lawsuits including discrimination, harassment, and wrongful termination claims

- Why it’s critical: Average defense costs can exceed $125,000, with claim frequency rising significantly over recent decades

- Cost for small businesses: Generally ranges from $150-$500 monthly based on industry and risk factors

- Who needs it: Essential for all businesses with employees, regardless of size

Running a business means facing numerous risks, but few are as potentially devastating as employment-related lawsuits. Whether you’re a small startup or an established company, employment practices liability insurance could be the difference between surviving a legal challenge and facing financial ruin.

In today’s litigious environment, even the most well-intentioned employers can find themselves facing costly legal battles. According to the Equal Employment Opportunity Commission (EEOC), the agency received 88,531 new charges of discrimination in fiscal year 2024, reflecting an increase of more than 9% over the previous year. Therefore, understanding employment practices liability insurance isn’t just smart business—it’s essential protection for your company’s future.

What is Employment Practices Liability Insurance?

Employment practices liability insurance (EPLI) is a specialized form of management liability coverage designed to protect companies and their decision-makers from claims arising from employees and third parties alleging wrongful employment acts. Essentially, EPLI serves as a financial shield against the mounting costs of employment-related litigation.

EPLI was first created in the early 1990s as employment litigation began increasing dramatically. Initially, large corporations were the primary purchasers of this coverage. However, today even small businesses with just one or two employees recognize the value of EPLI protection.

The coverage typically addresses claims involving wrongful termination, discrimination, harassment, hostile work environment, failure to hire, failure to promote, and retaliation. Moreover, many employment claims cite violations of federal, state, and local laws, including Title VII of the Civil Rights Act, the Americans with Disabilities Act, and the Age Discrimination in Employment Act.

How Much Does Employment Practices Liability Insurance Cost?

The cost of employment practices liability insurance varies significantly based on several key factors. In my 40+ years of experience helping businesses with insurance decisions, small businesses typically pay between $150 to $500 monthly for EPLI coverage, with most falling in the $200-$350 range depending on their specific risk profile.

Several factors influence your EPLI premium costs. First, your industry plays a crucial role in businesses in hospitality, healthcare, and professional services, which often face higher premiums due to increased claim frequency. Second, your company size matters significantly, as more employees create greater exposure to potential claims.

Additionally, your claims history directly impacts pricing. Companies with previous employment-related incidents will face higher premiums, while businesses with clean records enjoy more favorable rates. Furthermore, your chosen coverage limits and deductible amounts affect your annual costs.

Based on our client experience, a standard $1 million EPLI policy typically costs between $2,000 and $4,000 annually for businesses with five to twenty employees. Larger companies often purchase higher limits and face correspondingly higher premiums. Understanding these business insurance costs helps you budget appropriately for this essential protection.

Do Small Businesses Need Employment Practices Liability Insurance?

Absolutely, small businesses need employment practices liability insurance just as much as large corporations, if not more. According to legal industry research, a significant portion of EPLI claims target small private employers with fewer than 100 employees. This statistic demonstrates that size doesn’t provide protection from employment-related litigation.

Small businesses are particularly vulnerable because they typically lack dedicated HR departments and comprehensive employment policies. Consequently, they’re more likely to make inadvertent mistakes that lead to claims. Additionally, small businesses often can’t afford the substantial costs associated with defending employment lawsuits.

Consider the financial impact: defense costs alone can easily reach tens of thousands of dollars for small businesses, while larger claims may result in six-figure expenses. Furthermore, companies faced with employment lawsuits can incur costs that easily exceed $200,000 per lawsuit. These amounts can devastate a small business’s finances.

Moreover, you don’t need to lose a lawsuit for it to be expensive. Even frivolous claims require legal defense, creating substantial costs regardless of the outcome. Therefore, EPLI provides crucial financial protection that allows small businesses to survive employment-related legal challenges. This coverage becomes even more critical when combined with other essential protections like workers’ compensation and general liability insurance.

What Does Employment Practices Liability Insurance Cover?

Employment practices liability insurance provides comprehensive coverage for various employment-related claims and situations. Primarily, EPLI covers wrongful termination claims, which occur when employees believe they were fired illegally or without proper cause.

Discrimination claims represent another major coverage area. EPLI protects against allegations of discrimination based on age, race, gender, religion, disability, or other protected characteristics. Similarly, the policy covers harassment claims, including sexual harassment and creating hostile work environments.

The coverage also extends to retaliation claims, which arise when employees face negative consequences for reporting workplace violations or participating in investigations. Additionally, EPLI covers failure to hire or promote claims, wage and hour disputes, and employment-related defamation allegations.

Beyond legal costs, EPLI typically covers settlements and judgments awarded against your business. However, most policies exclude coverage for punitive damages, criminal acts, and violations of worker safety laws. Workers’ compensation claims and bodily injury incidents also fall outside EPLI coverage.

How is EPLI Different from Other Business Insurance Policies?

Employment practices liability insurance serves a distinct purpose compared to other business insurance coverages. Unlike general liability insurance, which covers third-party bodily injury and property damage claims, EPLI specifically addresses employment-related allegations from current, former, and prospective employees.

Workers’ compensation insurance covers employee injuries and illnesses occurring on the job, but it doesn’t address discrimination, harassment, or wrongful termination claims. Meanwhile, professional liability insurance protects against errors in professional services, not employment practices.

Directors and Officers (D&O) insurance covers management decisions and fiduciary responsibilities but has a narrower scope than EPLI. Conversely, EPLI provides broader protection for employment-related issues affecting the entire organization.

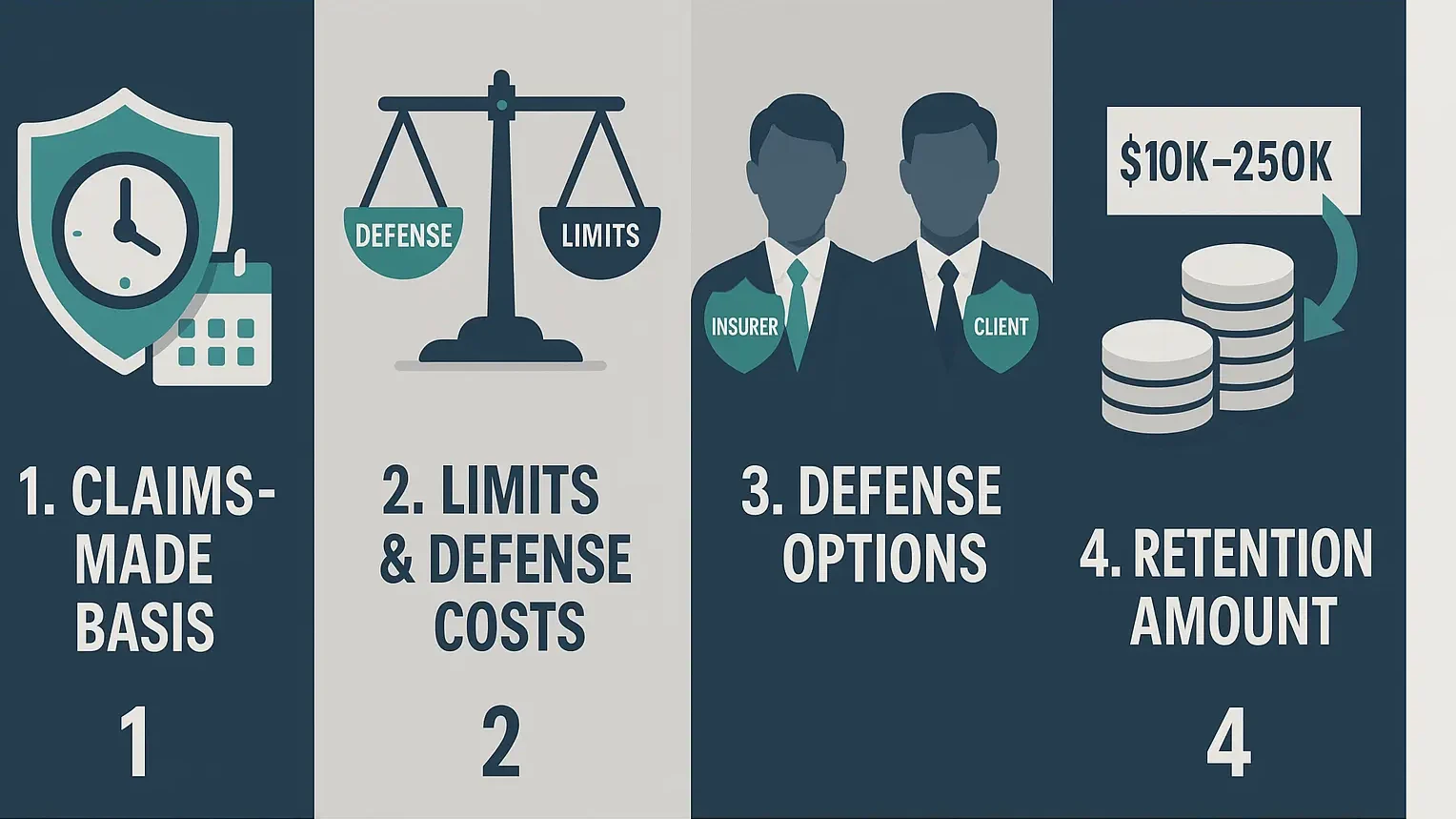

Most importantly, EPLI operates on a “claims-made” basis, meaning the policy must be active when a claim is filed, regardless of when the incident occurred. This structure differs from “occurrence-based” policies that cover incidents happening during the policy period. Understanding this distinction is crucial when designing your comprehensive business insurance program.

What are the Most Common EPLI Claims?

Understanding common EPLI claims helps businesses recognize their exposure and implement preventive measures. According to Equal Employment Opportunity Commission enforcement data, retaliation remains the most frequently cited claim, accounting for more than 47% of all charges filed, followed by claims of discrimination based on disability, race and sex.

Wrongful termination claims also rank among the most frequent categories, often involving allegations that employees were fired for illegal reasons or without following proper procedures. According to recent EEOC litigation analysis, discharge/constructive discharge was raised in over 70% of new employment suits filed.

Sexual harassment claims remain prominent, especially following the #MeToo movement’s impact on workplace culture. Harassment appeared in approximately 35% of new suits filed with federal agencies. Similarly, discrimination claims represent another frequent category, particularly involving age, gender, and racial discrimination.

Additionally, hostile work environment claims occur when employees allege that workplace conditions were so negative that they couldn’t perform their duties effectively. Understanding these trends helps businesses implement better workplace violence prevention strategies and comprehensive employment practice risk management.

Why are EPLI Claims Increasing?

Several factors contribute to the dramatic increase in employment practices liability claims over recent decades. First, employees have become more aware of their workplace rights through increased education and media coverage of employment issues. According to the Equal Employment Opportunity Commission (EEOC), the agency received 88,531 new charges of discrimination in fiscal year 2024, reflecting an increase of more than 9% over the previous year.

Social movements like #MeToo have encouraged employees to speak out against workplace misconduct, leading to more harassment and discrimination claims. Additionally, evolving employment laws create new opportunities for claims as legal protections expand.

The rise of social media and online resources has made legal information more accessible, empowering employees to recognize potential violations and seek legal remedies. Furthermore, the increasing diversity of the workforce has highlighted discrimination issues and created more opportunities for claims.

Economic pressures also play a role, as employees facing financial stress may be more likely to pursue legal action against employers. Moreover, the growth of employment law practices has made legal representation more available to workers. Understanding these trends helps businesses implement better workplace violence prevention strategies and comprehensive risk management approaches.

How Can Businesses Prevent EPLI Claims?

Preventing employment practices liability claims is far more cost-effective than defending against them. First and foremost, businesses should develop comprehensive, clearly written workplace policies addressing discrimination, harassment, and employment practices. These policies should be drafted or reviewed by employment attorneys to ensure legal compliance.

Regular training for all employees, managers, and leaders is essential. Training should cover appropriate workplace behavior, anti-discrimination policies, and proper procedures for handling complaints. Additionally, businesses should implement careful hiring processes with clear job descriptions and consistent interview procedures.

Documentation plays a crucial role in claim prevention. Companies should maintain detailed records of all employment decisions, performance reviews, disciplinary actions, and policy violations. Regular performance reviews help establish clear performance standards and document any issues.

Furthermore, businesses should establish clear complaint procedures and investigate all reported incidents promptly and thoroughly. Having an employment attorney available for consultation can help navigate complex situations and prevent minor issues from becoming major claims. Combining these preventive measures with comprehensive business insurance coverage creates a robust protection strategy. Companies should also consider implementing cyber security training to address modern workplace challenges.

How Does EPLI Policy Structure Work?

Employment practices liability insurance operates differently from many other business insurance policies. EPLI policies are typically written on a “claims-made” basis, meaning coverage applies to claims filed during the policy period, regardless of when the underlying incident occurred.

Most EPLI policies include defense costs within the liability limit, meaning legal expenses reduce the available coverage for settlements or judgments. This structure requires careful consideration of policy limits to ensure adequate protection. In my experience, small businesses often purchase $1 million limits, while larger companies may need $2-5 million or higher limits.

EPLI policies can be structured as “duty to defend” or “non-duty to defend” coverage. In duty to defend policies, the insurance company assigns and pays for defense attorneys from their approved panel. Non-duty to defend policies allow businesses to choose their own attorneys and seek reimbursement for legal costs.

Retention amounts, similar to deductibles, typically range from $10,000 to $250,000 or more for larger firms. The retention represents the amount the business pays before insurance coverage begins. Understanding claims-made policy structures is crucial for maintaining continuous protection.

What Should You Look for in an EPLI Policy?

When selecting employment practices liability insurance, several key features deserve careful consideration. First, examine the policy’s definition of covered claims and ensure it includes all relevant employment practices issues your business might face.

Coverage territory is important to ensure the policy covers claims in all jurisdictions where your business operates. Additionally, review the policy’s retroactive date, which determines coverage for past acts that might generate future claims.

Settlement provisions warrant attention, as some policies require insurer consent for settlements while others allow more flexibility. Furthermore, examine exclusions carefully to understand what situations the policy won’t cover.

Consider whether you need third-party coverage for claims from customers or vendors alleging harassment or discrimination. Additionally, evaluate the insurer’s financial strength and claims-handling reputation to ensure they can fulfill their obligations.

The Role of Employment Law in EPLI

Employment practices liability insurance exists because of the complex web of federal, state, and local employment laws. Title VII of the Civil Rights Act of 1964 prohibits discrimination based on race, color, religion, sex, or national origin and forms the foundation for many EPLI claims.

The Age Discrimination in Employment Act protects workers over 40 from age-based discrimination, while the Americans with Disabilities Act requires reasonable accommodations for disabled employees. The Equal Pay Act mandates equal compensation for equal work regardless of gender.

Additionally, the Family and Medical Leave Act provides job protection for certain family and medical situations. State and local laws often provide additional protections beyond federal requirements, creating a complex regulatory environment.

Understanding these laws helps businesses recognize their obligations and potential exposures. However, the complexity of employment law makes professional guidance essential for proper compliance and risk management. The U.S. Small Business Administration recognizes EPLI as essential coverage for evolving businesses, highlighting its importance in comprehensive business insurance strategies.

EPLI Claims Process and Best Practices

When facing a potential EPLI claim, immediate action is crucial. First, notify your insurance carrier as soon as you become aware of any potential claim, including EEOC charges, demand letters, or lawsuit filings. Early notification preserves your coverage rights and allows the insurer to provide guidance.

Preserve all relevant documentation and avoid destroying any records related to the claim. Additionally, avoid making statements about the situation without consulting your insurance carrier or attorney. Cooperate fully with your insurer’s investigation and follow their guidance throughout the process.

Consider implementing immediate remedial measures if appropriate, such as additional training or policy clarifications. However, avoid admitting liability or taking actions that might prejudice your defense. Professional guidance from employment attorneys and your insurance carrier is essential throughout the claims process.

Understanding when to file an EPLI claim can help protect your business interests. Additionally, maintaining proper claims documentation supports successful resolution.

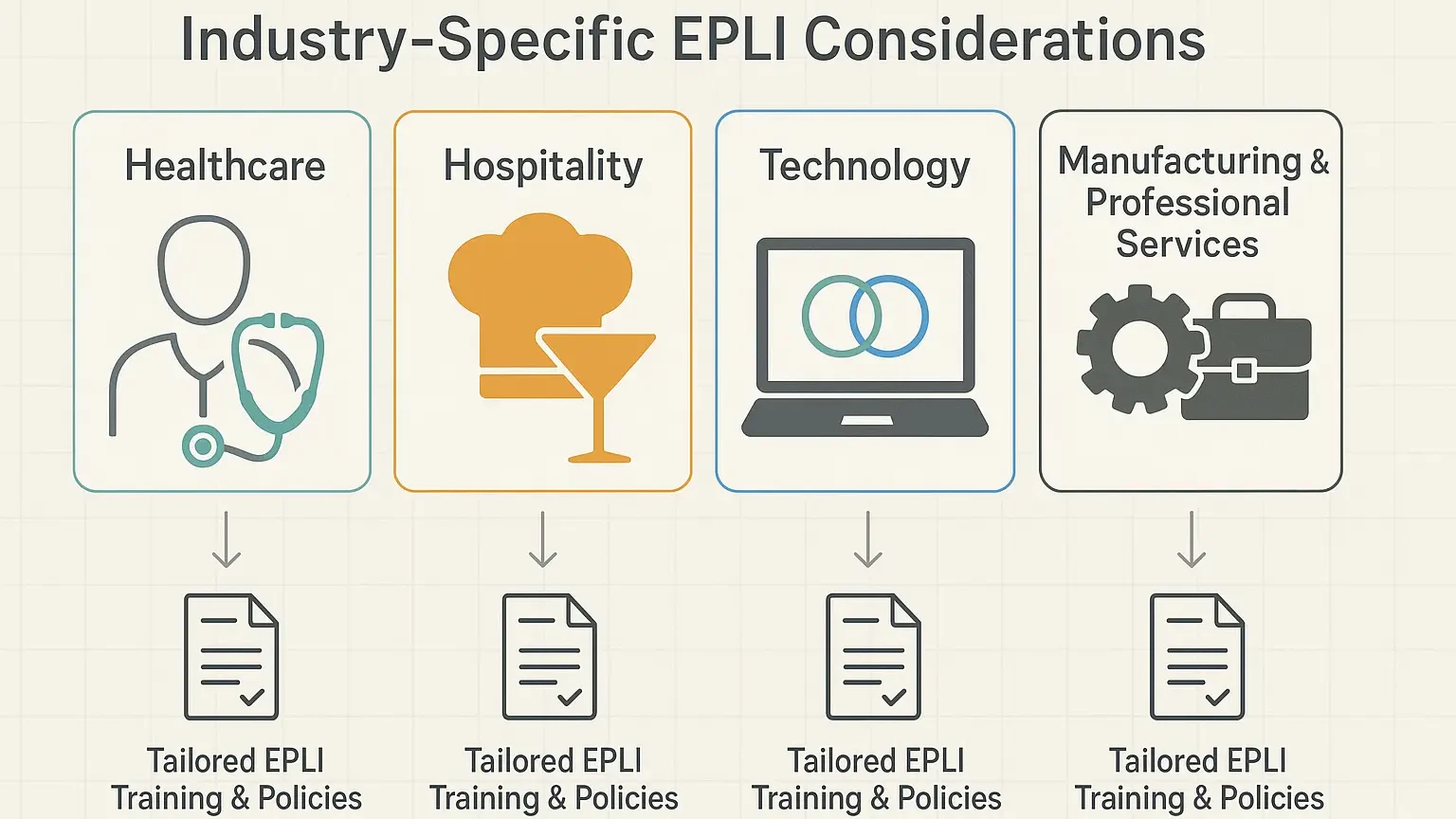

Industry-Specific EPLI Considerations

Different industries face varying levels of employment practices liability exposure. Healthcare organizations often face higher risks due to high-stress environments and frequent patient interaction. Restaurant and hospitality businesses typically see elevated harassment claims due to workplace culture and customer interaction.

Technology companies may face discrimination claims related to hiring practices and workplace culture. Manufacturing businesses often deal with safety-related retaliation claims and union-related issues. Professional services firms frequently encounter partnership disputes and client-related harassment allegations.

Understanding your industry’s specific risks helps tailor your EPLI coverage and risk management strategies. Additionally, industry-specific training and policies can help address common exposure areas.

The Future of Employment Practices Liability

Employment practices liability continues evolving as workplace dynamics change. Remote work arrangements create new challenges for harassment prevention and investigation. Social media use by employees raises questions about workplace behavior and company liability.

Artificial intelligence in hiring and employment decisions introduces potential discrimination issues that may not be covered by traditional policies. Additionally, evolving definitions of protected classes and workplace rights continue expanding potential claim areas.

Mental health awareness and workplace wellness programs create new obligations and potential liabilities for employers. Furthermore, generational differences in workplace expectations may lead to new types of claims. The EEOC’s focus on emerging issues, including the Pregnant Workers Fairness Act, demonstrates how employment law continues expanding.

Businesses should stay informed about employment practice insurance trends and consider working with experienced business insurance brokers who understand evolving risks.

Is EPLI Right for Your Business?

The decision to purchase employment practices liability insurance shouldn’t be taken lightly. Consider your business’s financial ability to handle a $125,000 lawsuit without insurance coverage. Additionally, evaluate your current HR policies and training programs to assess your risk level.

Think about your industry’s typical claim frequency and your company’s growth plans. Furthermore, consider the peace of mind that comes with knowing you have protection against employment-related lawsuits.

Remember that even businesses with excellent employment practices can face claims. Disgruntled employees, misunderstandings, and changing legal standards can all lead to litigation regardless of your intentions. Having comprehensive business insurance protection provides crucial security for your company’s future.

Consider consulting with experienced business insurance brokers who can assess your specific needs and design appropriate coverage solutions.

Protect Your Business Today

Employment practices liability insurance represents a critical component of comprehensive business protection. With claim frequency rising and average costs exceeding $125,000, can your business afford to go without coverage?

The statistics are clear: one in five businesses under 500 employees will face employment charges. Moreover, defense costs alone can devastate small business finances, making EPLI coverage an essential investment rather than an optional expense.