3D Printing Business Insurance

What Additive Manufacturers Need to Know

Why Standard Insurers Reject 3D Printing Businesses

Most insurers reject 3D printing businesses because generalist underwriters lack a classification that accurately reflects additive manufacturing risk, so they default to denial or over-pricing.

The financial cost of that gap is not a nuisance. A single uninsured product liability claim in this space can exceed $500,000, and one intellectual property dispute can run $200,000 to $1,000,000 in legal fees before a verdict. Operating without proper coverage is not a savings strategy. The consequences that follow a denied claim tend to be permanent.

Here is why generalist carriers consistently struggle with 3D printing businesses:

The path forward is working with a broker who has placed manufacturing coverage before and knows which carriers have current appetite for additive manufacturing risks.

Contact us to find out which markets are actively writing 3D printing business insurance programs right now.

What Does 3D Printing Business Insurance Cover?

A properly structured 3D printing business insurance program covers product liability, general liability, professional indemnity, commercial property, business interruption, cyber liability, IP exposure, and workers’ compensation. No single policy covers all of these at once, which is why a packaged program built around your specific business model outperforms any individual off-the-shelf policy. The coverage combination that protects a home-based prototype shop differs significantly from the program required by a commercial facility producing medical-grade components.

Here is a breakdown of the core coverages and what each one protects for 3D printing operations:

Coverage |

What It Protects |

Why It Matters for 3D Printing |

|---|---|---|

|

General Liability |

Third-party bodily injury, property damage, advertising injury |

Covers injury at your facility or damage to client property during operations |

|

Product Liability |

Injury or damage caused by a printed product you sell or deliver |

Critical if a part fails in use; covers legal fees and settlements |

|

Professional Indemnity (E&O) |

Design errors, failed prototypes, professional negligence |

Protects against client claims when design flaws or printing mistakes cause financial loss |

|

Commercial Property |

Printers, workstations, filament, raw materials, inventory |

Covers expensive equipment and materials from fire, theft, or damage |

|

Lost income during operational shutdowns |

Compensates revenue loss when equipment failure or a disaster halts production |

|

|

Data breaches, hacked systems, stolen CAD files |

Protects against digital risks specific to connected 3D printing workflows |

|

|

IP Liability |

Patent, trademark, and copyright infringement claims |

Covers legal defense costs for IP disputes involving designs or processes |

|

Work-related injuries and occupational illness |

Mandatory in most states; covers fume exposure, burns, and material-related illness |

|

|

Cost of recalling a defective batch of printed products |

Fills a gap that standard product liability policies leave open |

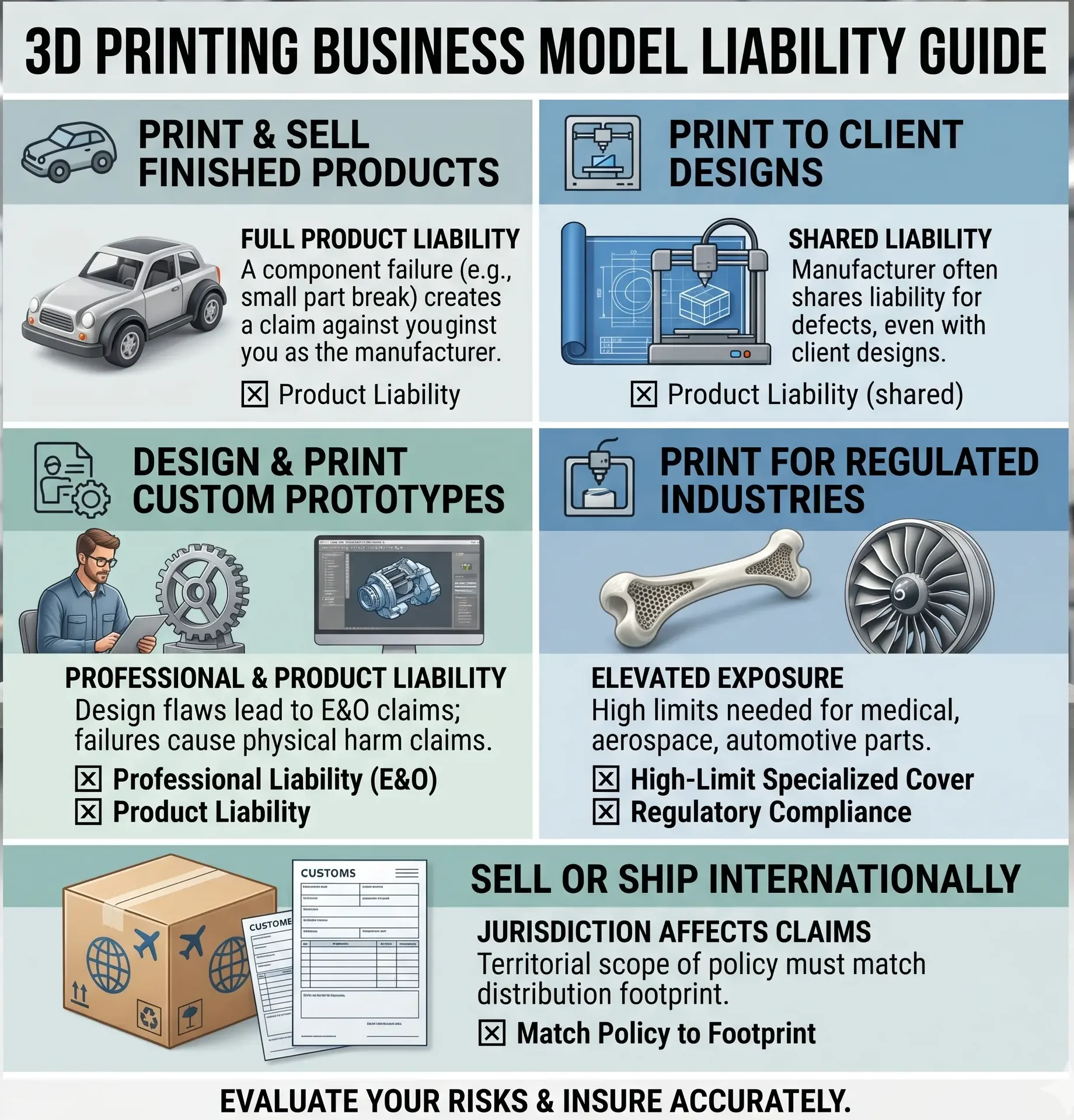

Do You Need Product Liability Insurance for a 3D Printing Business?

Product liability insurance is the single most essential coverage for any 3D printing business that delivers a physical product, and it applies regardless of whether you designed the product yourself. If a 3D-printed part fails and causes bodily injury or property damage, your business faces a lawsuit. According to the Insurance Information Institute, defense and cost containment expenses are among the highest in product liability lines; legal defense alone routinely runs $75,000 to $150,000 before a settlement is reached, and a judgment can go far beyond that. The secondary risk that business owners miss is the manufacturer’s share of liability, which applies even when the design came entirely from the client.

How product liability applies based on your business model:

Real-world example

A 3D printing company produced custom mounting brackets for a commercial lighting manufacturer. The brackets failed during installation at a job site, causing $180,000 in property damage. The printing company’s standard general liability policy excluded manufactured goods under the products-completed operations section. The claim was denied in full. A properly endorsed product liability policy would have covered the entire loss.

Book a call to confirm that your product liability structure actually matches how your business delivers products.

How Much Does 3D Printing Business Insurance Cost?

A 3D printing business insurance program for a mid-size commercial operation typically runs $2,500 to $6,000 per year for a properly structured program combining general liability, product liability, professional indemnity, and commercial property.

High-volume print farm operations and businesses producing medical devices, aerospace components, or automotive parts should budget $5,000 to $10,000 or more annually, depending on revenue, equipment value, and coverage limits. The wide premium range reflects how dramatically additive manufacturing businesses vary in risk profile, and why a specialist broker who codes your business correctly consistently delivers better pricing and better coverage than a generalist who defaults to the wrong classification.

The factors that drive your premium:

Benchmark premiums by business type:

Business Type |

Estimated Annual Premium |

|---|---|

|

Freelance or light commercial prototyping |

$1,200 to $2,500 per year |

|

Mid-size commercial operation or print farm (6 to 25 employees) |

$2,500 to $6,000 per year |

|

Large-scale manufacturer or high-volume print farm |

$5,000 to $10,000 per year |

|

Regulated industries (medical, aerospace, automotive, children’s products) |

$7,500 to $15,000+ per year |

Some sources cite $1,500 to $4,000 per year for basic coverage; those figures typically reflect bare-minimum general liability placements for light operations, not the full-program structure a commercial additive manufacturer actually needs.

A mid-size facility or print farm running production volume, handling client designs, and supplying regulated industries requires coverage across multiple lines, and the premium reflects that.

Contact us for an accurate estimate based on your actual operations, equipment, and products.

Does Standard Business Insurance Cover 3D Printing Operations?

Standard business insurance rarely covers 3D printing operations adequately, and the gap almost always shows up at claim time rather than when the policy is purchased. The most common failure point is the products-completed operations exclusion inside a standard commercial general liability policy, which eliminates coverage for injury or damage caused by products the business manufactured. Because most standard underwriters classify additive manufacturing as a manufacturing activity, that exclusion directly eliminates coverage for your core business output.

Common exclusions and coverage gaps in standard business policies for 3D printing operations:

Understanding these exclusions before binding any policy is the minimum standard for protecting a 3D printing business.

Cyber Liability Insurance for 3D Printing Companies

Cyber liability insurance covers data breaches, network intrusions, ransomware, and digital theft, and 3D printing businesses have specific cyber exposures that are larger than most owners recognize. If you store customer CAD files, client design specifications, or proprietary manufacturing data on networked systems, you have a target that ransomware operators and IP thieves actively pursue.

A breach that exposes a client’s design files can produce a liability claim against your business even if you were the victim of the attack, not the cause. That specific exposure is why cyber coverage for additive manufacturing businesses is not optional.

Key cyber risks specific to 3D printing operations:

Policies vary significantly in what they cover, particularly around social engineering and data restoration.

Working with a broker who reviews cyber policy language rather than simply comparing premiums makes a material difference in what you actually receive when a claim occurs.

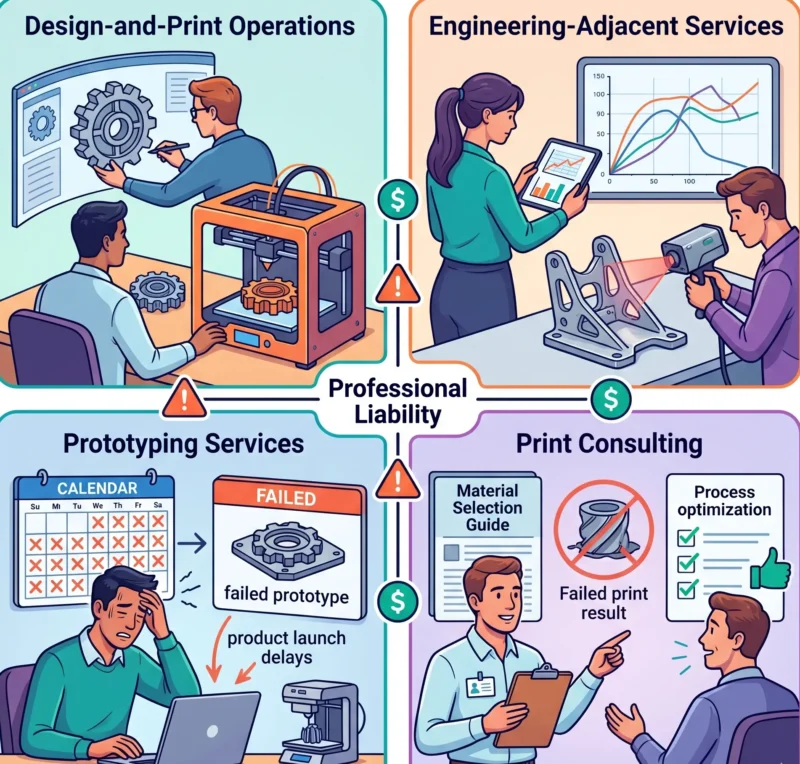

Professional Liability (E&O) Insurance for 3D Printing Businesses

Professional liability insurance, also called errors and omissions coverage, protects 3D printing businesses against claims arising from design errors, failed prototypes, and professional negligence, and it applies even when no physical injury or property damage occurs.

If a client hires you to design and print a custom component and the finished product fails to meet specifications, causing the client to miss a production deadline and lose revenue, that loss generates a professional liability claim. Your general liability policy will not respond. Only professional liability applies to pure financial loss claims of this type, which means 3D printing businesses that offer design services alongside printing carry a gap in their coverage if they only hold a CGL policy.

Who specifically needs professional liability coverage in the 3D printing space:

Maintaining continuous coverage and securing tail coverage when switching carriers protects against gaps in older claims that surface after a policy change.

Book a call to review how professional liability should be structured alongside your product liability program.

Workers’ Compensation for 3D Printing Operations

Workers’ compensation is mandatory in most U.S. states for any business with employees, and 3D printing facilities have specific occupational hazards that make this coverage more consequential than business owners typically expect.

Additive manufacturing exposes workers to ultrafine particles, chemical fumes, heat sources, and, in some operations, hazardous metal powders, all of which create injury and long-term illness risk that can generate claims years after initial exposure.

Key occupational health risks in 3D printing facilities:

NIOSH’s publication on 3D printing health and safety outlines recommended engineering controls, ventilation standards, and PPE requirements for additive manufacturing environments, including specific hazard assessments for filament emissions and thermal contact risks.

Facilities that operate without compliant ventilation and PPE programs face regulatory fines alongside the workers’ compensation claims that follow an incident.

Incorrect classification is a common underwriting error that leaves businesses either overpaying or, more dangerously, holding a policy with classification-based exclusions that surface at claim time.

How to Evaluate a 3D Printing Insurance Policy

A 3D printing insurance policy is only as complete as its exclusions allow, and the exclusions most likely to eliminate coverage are the ones buried in endorsements rather than visible on the declarations page.

Most coverage disputes in additive manufacturing trace back to policies that looked adequate at purchase but contained manufacturing exclusions, IP carve-outs, or cyber event gaps that stripped coverage from the claims that actually occurred. Reviewing a policy before binding it is not optional for a 3D printing business. It is the moment when gaps are fixable.

What to verify before binding any 3D printing business insurance policy:

Working with a broker who has placed additive manufacturing coverage before is the most efficient way to avoid these gaps.

Quick Reference: 3D Printing Business Insurance at a Glance

Everything a 3D printing business owner should have clear before buying coverage. If any of these points describe a gap in your current program, it is worth a specialist review before your next renewal.

Book a call to walk through your current coverage against this checklist.

The Coyle Second Opinion

9 out of 10 business insurance policies we review have a gap that would sink a claim

Yours might be one of them, and the only time you find out is when you file a claim and it gets denied. Send us your policy for an independent, confidential read: what’s covered, what’s missing, what you’re overpaying for. We never contact your broker or shop the market. Flat $2,500, refunded in full if you don’t get real value.

The team that reads your policy, line by line.

Questions about 3D Printing Business Insurance?

Get the Right Coverage for Your 3D Printing Operation

3D printing business insurance is not a policy you pick off a shelf. The right program requires a broker who understands additive manufacturing risk, can read your client agreements and production workflows, and has placed product liability and cyber coverage for businesses like yours.

The Coyle Group has structured insurance programs for commercial additive manufacturers, print farm operations, contract prototyping services, and businesses supplying the medical, aerospace, and automotive industries across the US. Our approach starts with your operations and your products, not a generic application.

Contact us with your current declarations pages and a description of what you print and who you print it for. We will identify every coverage gap in one call.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?