What Does a Product Recall Cost?

and What Does Recall Insurance Cost to Cover It?

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

You already suspect the answer is “a lot.” What most owners do not realize is how the number is built, and how little of it their current policy will actually pay.

Here is the honest version.

Your general liability policy was never designed to pay most of it. The Coyle Group is a commercial insurance agency that handles the complex, high-value risks other agencies don’t know how to structure, where the details in the policy are the difference between a paid claim and a denied one. Over 40 years, I’ve watched product businesses treat recall as a someday problem, right up until it becomes a this-quarter emergency.

The problem is that you think a recall would cost “a lot,” but you have no real number, and you assume you’re covered. We quantify your true exposure and structure product recall insurance that actually pays first-party recall costs. In the programs we review, most product companies carry either no recall coverage or a sublimit far too small to matter.

Book a call and get a straight answer on your exposure.

What does a product recall actually cost a business?

A product recall typically costs a business around $10 million in direct expenses for food and consumer brands, and that is the floor, not the ceiling. The part that surprises owners is what sits underneath that headline number. Direct cost is less than half the real damage; the rest hides in business interruption, lost contracts, and litigation that unfolds for a year or more after the recall notice goes out.

That $10 million figure comes from a widely cited Grocery Manufacturers Association study, and the same research found that 52% of companies with a major recall reported total impact exceeding $10 million, while 1 in 20 crossed $100 million.

The way I think about it, and the way I’ve counseled clients for four decades, is total cost of risk, not just one line item.

Total cost of risk means everything the event drains from you: the recall operation itself, deductibles, claims you pay out of pocket, higher premiums at your next renewal, lost business from downtime, and reputation damage that suppresses sales long after the product is off the shelf.

A recall attacks every one of those at once.

Not sure what your own number looks like? and we’ll walk your exposure line by line.

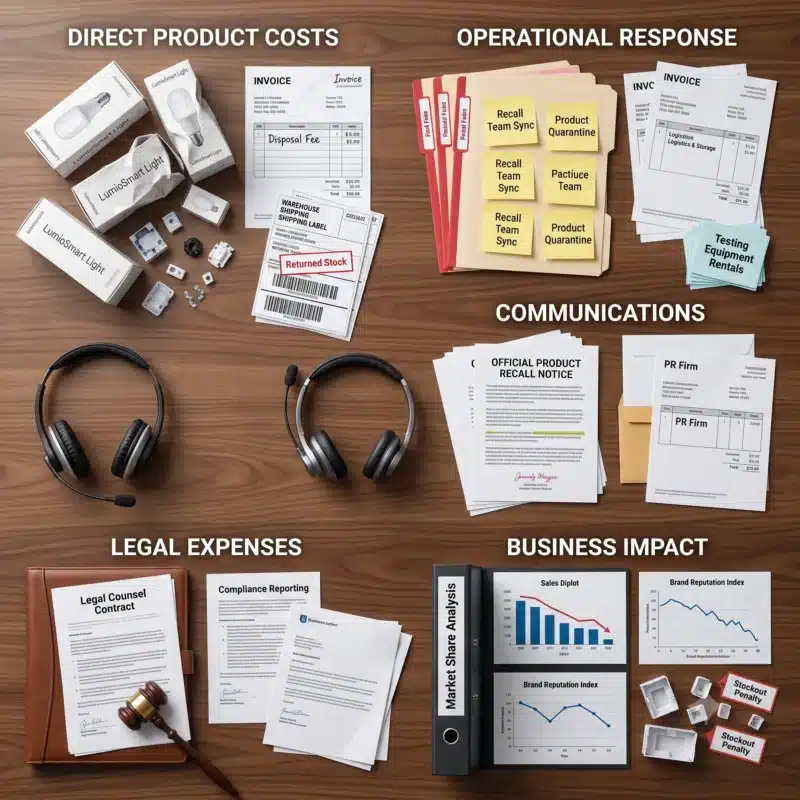

Where does the money actually go in a recall?

The money goes far beyond pulling product off shelves. Notification, retrieval, disposal, and refunds are only the visible layer. The single largest bucket is usually business interruption, the revenue you lose while a line sits idle or a plant is shut for cleaning and investigation. Most cost guides stop at the direct expense and quietly ignore the half of the bill that does the most damage.

A pharmaceutical recall cost analysis breaks the total down cleanly, and the split is worth memorizing:

Cost bucket |

Share of total recall cost |

What it includes |

|---|---|---|

|

Direct recall operation |

~35% |

Retrieval, disposal, customer reimbursement, regulatory response |

|

Business interruption |

~49% |

Lost revenue during shutdowns, halted production, idle lines |

|

Rehabilitation, communications, consulting |

~16% |

PR, brand repair, crisis consultants, legal notices |

Here is the full picture of where recall dollars land:

From what I’ve seen, the owners who get blindsided are the ones who budgeted for the first bullet and forgot the other four.

What are the 3 types of product recalls?

There are three recall classes, and they rank how dangerous the product is, not how much it costs you. Class I means a reasonable probability of serious injury or death. Class II means temporary or reversible harm. Class III means a violation unlikely to cause harm. The twist most owners miss is that even a low-severity Class III recall can still generate serious first-party costs, because notification, retrieval, and downtime do not care how the government graded the hazard.

A few practical points I stress with clients:

Want to know which class your product would likely fall under? and we’ll map it.

How much does a recall cost by industry?

Recall cost swings enormously by industry, from low seven figures for a contained food event to tens of billions across an auto sector in a bad year. The reason is not just product value; it is severity, unit volume, and how life-critical the product is. The mistake I see owners make is benchmarking against the wrong industry, assuming a small product means a small recall, when fixed response costs punish everyone.

Here is how the verified figures stack up:

Industry |

Typical / notable recall cost |

Source |

|---|---|---|

|

Food and beverage |

~$10M average direct cost per event |

GMA study |

|

Fresh-cut produce (contained event) |

>$2M for under 250,000 units, no fatalities |

Documented case |

|

Pharmaceutical |

Direct cost is ~35% of a total that runs far higher |

Pharma cost analysis |

|

Medical device |

Sector spends $7–8.5B annually on quality events; a single event can reach $600M |

McKinsey |

|

Automotive |

>$20B across North American automakers in 2017; ~$500 per vehicle |

AlixPartners |

The automotive tail is instructive.

Those are not freak outliers; they are what happens when a defect reaches scale before anyone catches it.

Children’s items and toys are close behind, thanks to strict federal safety rules, so toy manufacturers face both regulatory complexity and high claim severity.

A real case worth sitting with. In one documented food recall, the recalled product’s own market value was modest, around $33,598 at the median for that year’s recalls. The response still cost more than $2 million once notification, retrieval, testing, and disposal were tallied. The lesson we see in practice: the product on the truck is rarely the expensive part. The machine you have to run to get it back is.

If you make or distribute a high-risk product, before your next renewal, not after your first scare.

How likely is a product recall in the first place?

Likely enough that the question “what does a product recall cost” should be a line in your risk plan, not a hypothetical. The FDA reported nearly 5,000 product recalls in a single recent fiscal year, and recalls now happen somewhere almost every day. The part owners underestimate is not whether recalls happen; it is how easily a supplier or component failure upstream lands the cost on you.

Owners assume a recall is something that happens to sloppy operators, then a raw-material supplier, a co-packer, or a single contaminated lot puts them in the headlines through no fault of their own.

Regulatory pressure has only tightened, which raises both the frequency and the scrutiny.

A few realities worth internalizing:

What expenses are covered under product recall insurance?

Product recall insurance covers the first-party costs of pulling a product from the market: notification, retrieval, disposal, replacement, crisis PR, and the business interruption that follows. In plain terms, it pays for the recall operation itself, the part your liability policy ignores. The nuance that trips people up is that coverage is broad on paper but shaped heavily by exclusions and sublimits, so what you actually collect depends on how the policy is structured.

A well-built recall policy typically reimburses:

Coverage you do not understand is coverage you cannot rely on.

Will my general liability or product liability policy cover a recall?

Almost certainly not for the recall itself. General liability and product liability insurance pay for bodily injury or property damage your product causes to other people. They generally do not pay your first-party cost to recall, retrieve, and destroy that product. This is the single most expensive misunderstanding in the category, and it surfaces at the worst possible moment: after the recall has already started.

The distinction is clean once you see it:

These are two distinct exposures that require two distinct policies.

Frankly, most business owners assume they’re basically the same thing with different labels, and that assumption is exactly what leaves the recall bill sitting on their own balance sheet.

A liability policy might include a token recall sublimit, often small enough that owners only discover its size when they finally read the declarations page.

Treating that inner limit as real recall protection is like treating a spare tire as a second car.

Think your current policy has you covered? and we’ll read the fine print with you.

How much does product recall insurance cost annually?

Product recall insurance premiums usually start in the low thousands of dollars a year and scale up sharply from there based on your risk. As a reference point, some carriers set a minimum recall premium around $5,000, well below their product liability minimums, which shows the coverage is more affordable than most owners fear. The catch is that “minimum” is where pricing begins, not where a real manufacturer lands, and the drivers that move your number are entirely within an underwriter’s judgment.

The factors that actually set your recall premium:

Premium driver |

Effect on price |

|---|---|

|

Annual revenue and sales volume |

Higher exposure, higher premium |

|

Product category |

Food, supplements, toys, auto parts, and medical devices price well above low-risk goods |

|

Distribution footprint and geography |

Wider reach and exports raise cost |

|

Loss history |

Prior recalls or claims increase premiums significantly |

|

Quality control and traceability |

Strong documented controls lower cost |

|

Limits and deductibles |

Higher limits cost more; higher retentions lower premium |

I actually recorded a video years ago answering this exact question, because clients asked it so often.

A cheap policy with a useless sublimit is not a deal; it is a false economy.

You want lower premiums?

How do you figure out how much recall coverage you actually need?

Start by sizing the worst realistic event for your product, then buy a limit that keeps that event from ending the company. The honest goal is not to insure every dollar; it is to make sure a single recall cannot bankrupt you. What most owners want, but rarely get from a form or a portal, is help translating “what could actually happen to us” into a limit and a structure.

Larger firms self-insure more of it by choice; smaller firms often self-insure it by accident and regret it.

To size it well:

From what I’ve seen, the businesses that handle recall well are not the ones with the biggest limits.

They are the ones who did this math before they needed it.

Take the guesswork out of your recall exposure

We can quantify your exposure, show you exactly what your current policy would and would not pay, and structure recall coverage that responds when it matters. or contact us for a no-obligation review of your program.

Questions about What Does A Product Recall Cost?

Get The Right Coverage For Your Product Recall Risk

You have seen the real numbers, the hidden costs, and the coverage gaps. The only question left is a simple one: what would a recall actually cost your business, and who would pay for it?

Find out with The Coyle Group. We size your true recall exposure, read your current limits and exclusions, and show you in plain English what a recall would cost and what your policy would really pay.

No pressure, and no need to leave your current agent to get a straight answer.

Book a short call or reach out, and you will walk away with a clear number and a plan to transfer the risk.

It takes only a few minutes to stop guessing and finally know your business is covered.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

Product Liability Insurance for Importers: What You Need to Know (Video)

How to Protect Your Business From a Product Recall

The Boar’s Head Product Recall – What’s Insured?