Dietary Supplement Product Liability Insurance

What Every Supplement Brand, Private-Label Manufacturer, and Amazon Seller Needs to Know Before a Claim Hits

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

That is one of the most common things supplement brand owners say when they first reach out to us. They went to a standard carrier, got a quote, and were told their ingestible products were too risky to cover under a standard general liability policy. Or they bought coverage, filed a claim, and discovered the adjuster had a very different reading of what their policy actually covered.

Running a dietary supplement business without the right product liability coverage is not a gray area. One consumer injury claim, one FDA-linked recall, one class action over a mislabeled ingredient, and you are paying defense costs, settlements, and recall expenses entirely out of pocket.

The Coyle Group structures dietary supplement product liability insurance for complex, high-value risks that many standard agencies are not equipped to underwrite. Most admitted carriers do not offer standalone supplement product liability programs, so placement often requires access to specialty markets and program carriers that evaluate ingredient risk, GMP status, and channel exposure as separate underwriting considerations.

These are factors that may fall outside the scope of a generalist broker working through standard wholesale channels. If you manufacture, private-label, import, or distribute dietary supplements, this page explains what coverage you need, what it typically costs, and what underwriters evaluate when quoting your risk.

Is Your Supplement Brand Actually Covered?

What this page covers: Dietary supplement product liability insurance protects supplement manufacturers, private-label brands, distributors, and Amazon sellers from lawsuits, recall costs, and regulatory-linked claims tied to their products. Standard general liability policies routinely exclude ingestible products, leaving brands with zero coverage when a claim hits. The Coyle Group works with carriers who specialize in this space and structures programs that cover your actual product mix. Book a call, and we will review your current coverage and identify any gaps in one conversation.

Why Standard General Liability Will Not Protect Your Supplement Brand

Dietary supplement manufacturers face product liability lawsuits, FDA-triggered recalls, and class action exposure at a rate that makes ingestible products one of the most heavily scrutinized categories in the specialty insurance market.

A single adverse-event lawsuit in this space can generate $500,000 to over $2 million in defense and settlement costs. The FDA actively monitors and enforces mandatory dietary supplement recalls, and the operational cost of executing a recall, covering consumer notification, product retrieval, and crisis management, routinely reaches $250,000 to $2 million or more, depending on distribution volume.

The problem most supplement brands discover too late is that standard general liability policies are not built for products people put in their bodies. The standard Commercial General Liability (CGL) form is written for premises and operations liability: slip-and-falls, property damage at your location, and basic advertising injury. When a consumer claims your protein powder caused liver damage, or your pre-workout contained an undisclosed stimulant that triggered a cardiac event, your standard CGL carrier will frequently deny the claim by citing an exclusion you did not know was buried in the policy language. That assumption costs brands hundreds of thousands of dollars.

The exclusion language that trips up supplement companies most often includes:

If you are selling dietary supplements under any of these policies, you need to read your exclusions section carefully. The Coyle Group reviews policies at no cost and flags every gap before a claim makes it relevant. Contact us to schedule a review.

A Real Example of How This Plays Out

A mid-size supplement brand selling a protein powder formula through Amazon and three regional retail chains carried a standard commercial general liability policy with a $1M per-occurrence limit. A customer filed a bodily injury claim alleging contaminated product. The carrier’s adjuster reviewed the policy and cited the consumable products exclusion. The brand was fully responsible for defense costs. By the time the case settled, out-of-pocket expenses exceeded $380,000. The brand had been paying $1,800 per year for a policy that provided zero coverage for its actual product.

What Dietary Supplement Product Liability Insurance Actually Covers

Dietary supplement product liability insurance pays for legal defense, medical expenses, settlements, and court judgments when a consumer, retailer, or third party claims your supplement caused harm. A properly structured policy covers bodily injury and property damage arising from your product at any point in the distribution chain. What most brands do not realize is that the coverage needs to be specifically underwritten for ingestibles, and the endorsements you add determine whether your policy actually pays in real-world claim scenarios.

Here is what a well-structured supplement product liability program covers:

Coverage Feature |

Standard CGL |

|---|---|

|

Bodily injury from ingestible products |

Often excluded |

|

Legal defense for adverse-event claims |

Typically excluded |

|

Mislabeling and false claims |

Often excluded |

|

Recall cost coverage |

Excluded |

|

Amazon additional insured |

May not accommodate |

|

High-risk ingredient coverage |

Excluded |

|

Class action defense |

May be limited |

Contact us to compare your current policy against this checklist. We turn around coverage reviews within 24 hours.

Who Needs Dietary Supplement Product Liability Insurance

Any business whose brand name appears on a dietary supplement label, or that participates in the manufacturing, private-labeling, importing, distributing, or selling of dietary supplements, has direct exposure to product liability claims. The manufacturer is not the only party that gets sued. Everyone in the chain does.

The businesses that need dietary supplement product liability insurance include:

One of the most common misconceptions in this space is the belief that holding a co-manufacturer agreement transfers liability to the contract facility. It does not eliminate your exposure. If your brand name is on the label, you will be named in the lawsuit regardless of your manufacturing arrangement.

Who May NOT Need a Standalone Supplement Product Liability Policy

Retailers that sell only factory-sealed, nationally-branded supplements they have no labeling or formulation involvement with may have coverage under the brand manufacturer’s policy, provided they have a current vendor agreement in place. That said, a policy review is still recommended before assuming you are covered; many retail vendor agreements do not extend the manufacturer’s product liability to the reseller in all claim scenarios. When in doubt, a quick policy audit will confirm your actual exposure.

Explore the full range of insurance coverage available to supplement manufacturers and see how product liability fits within a complete risk program.

Book a call if you are unsure which category applies to your business. The underwriting classification you fall into directly determines what policies are available to you and at what price.

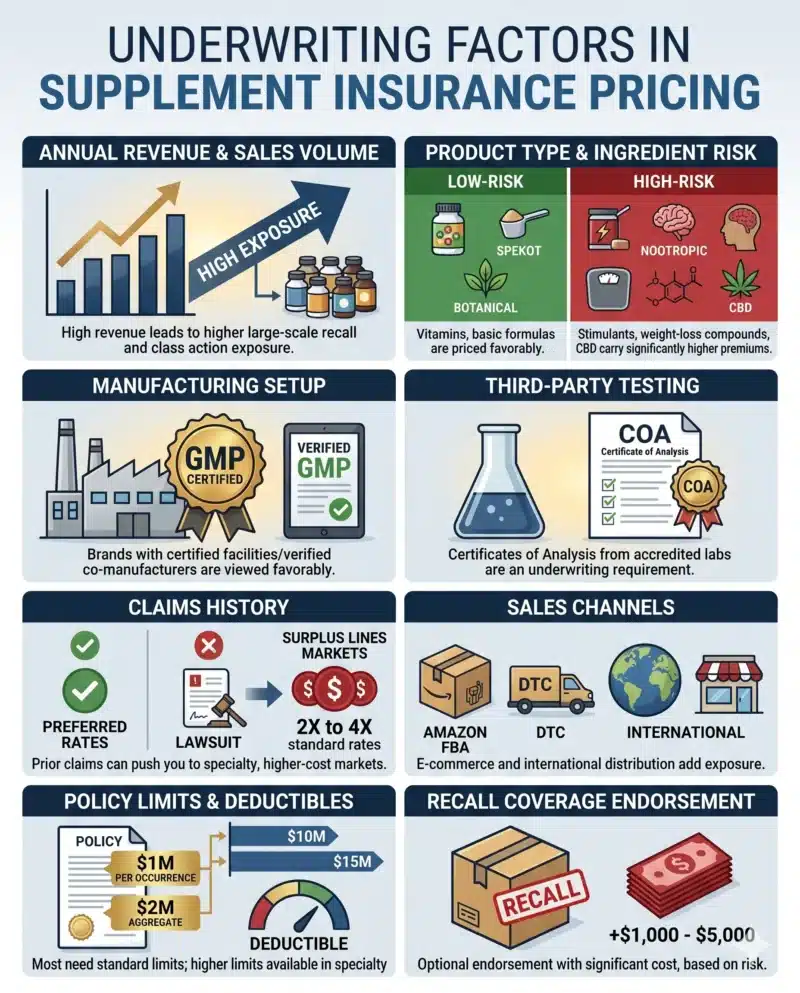

What Dietary Supplement Product Liability Insurance Costs

Dietary supplement product liability insurance typically starts at $2,500 per year for small brands with limited distribution and low-risk ingredient profiles, and scales significantly based on revenue, product type, ingredient risk, claims history, and sales channels. Understanding what drives cost is more useful than a single average number, because the range is genuinely wide: a basic vitamin brand with clean ingredients and under $1M in revenue may pay $3,000 to $6,000 per year, while a sports nutrition brand with stimulant-based pre-workouts and $10M in revenue may pay $25,000 to $50,000 or more.

The factors underwriters weight most heavily when pricing dietary supplement product liability insurance are:

Explore product liability insurance cost data to understand how limits, deductibles, and industry classification affect your final number.

The Exclusions That Catch Supplement Brands Off Guard

Dietary supplement product liability insurance policies can have exclusions that eliminate coverage for your most likely claim scenarios. These are the gaps that generate the forum complaints about insurers who “have entire teams dedicated to denying your orders.” Understanding what your policy excludes before a claim happens is not optional.

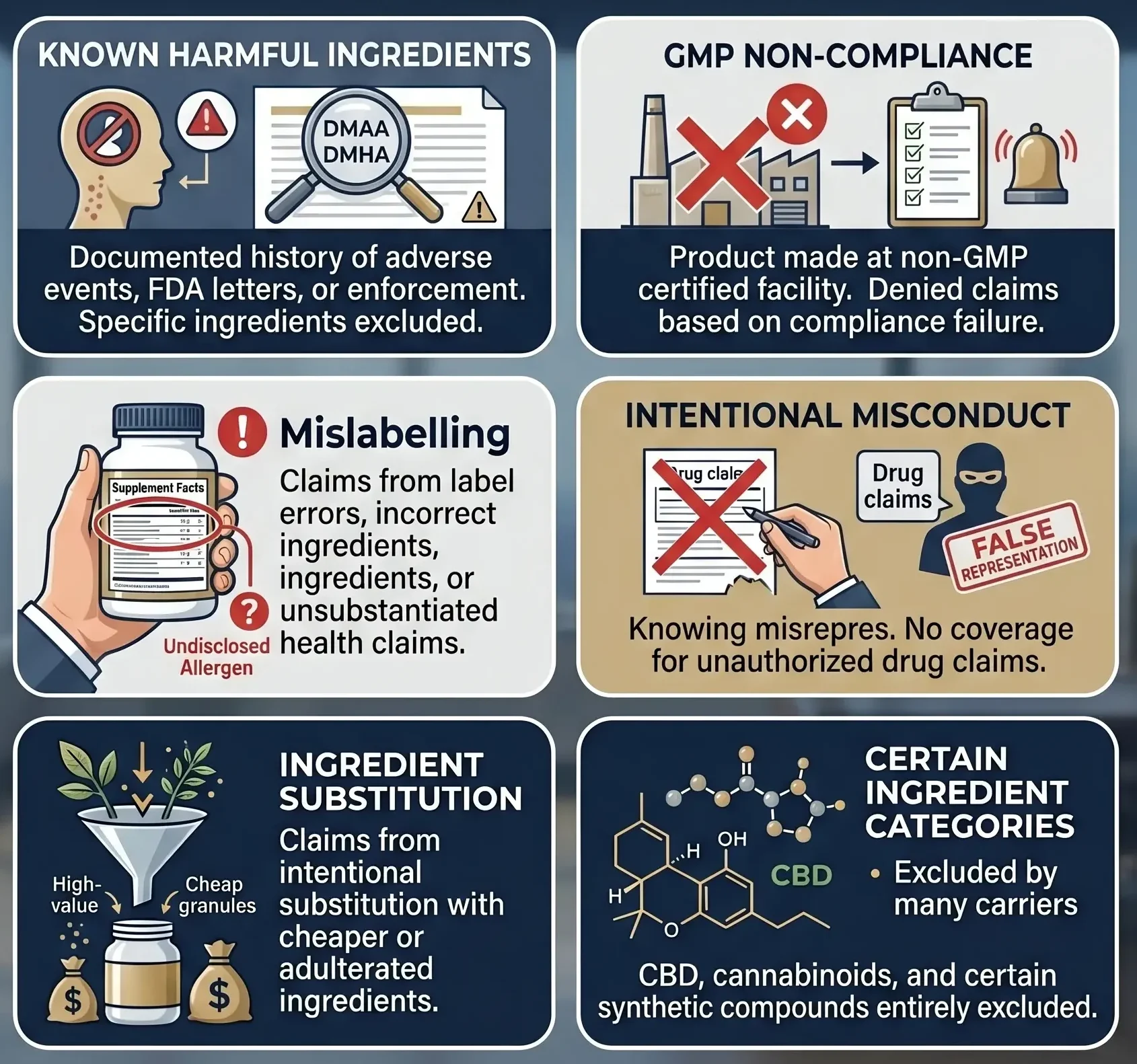

The most common exclusions to review in any supplement product liability policy are:

Known harmful ingredient exclusion:

If an ingredient in your formula has a documented history of adverse events, FDA warning letters, or NY AG enforcement actions, your carrier may specifically exclude claims related to it; this is common with stimulants like DMAA, DMHA, and certain botanical extracts

GMP non-compliance exclusion

If your product was manufactured at a facility that is not GMP-certified or cannot produce documentation of GMP compliance, the carrier may deny bodily injury claims on the basis that the harm arose from a compliance failure rather than a covered product defect

Recall cost exclusion

Base product liability policies do not cover the cost of executing a recall; if you need to notify consumers, pull product, and manage FDA correspondence, those costs are out of pocket unless you added a product recall endorsement; review the full scope of supplement recall exposure to understand what that endorsement actually covers

Mislabeling exclusion

Some policies cover manufacturing defects but exclude claims that arise from label errors, including incorrect ingredient amounts, undisclosed allergens, or structure/function claims that are not substantiated

Intentional misconduct exclusion:

If a claim arises from a knowing misrepresentation of your product’s contents or effects, the carrier will exclude coverage; this also applies to FDA enforcement actions if your labels are found to contain unauthorized drug claims

Ingredient substitution exclusion

Adulteration claims where a cheaper ingredient was substituted for the labeled one may fall outside standard coverage if the substitution is deemed intentional

Certain ingredient categories

CBD, hemp-derived cannabinoids, and certain synthetic compounds are excluded by many specialty carriers entirely; if these are in your formula, you need a carrier who writes this risk specifically

The cleanest way to audit your exclusions is to send your current policy and your product list to a broker who specializes in this space and have them cross-reference the two.

What Underwriters Actually Look For: How to Get Approved and Keep Your Rates Down

Getting this coverage approved by a specialty carrier requires documentation that most standard agents never ask for. Knowing what underwriters need before you apply speeds up the process and significantly affects your quoted rate.

The underwriting information and documentation most specialty supplement carriers require includes:

What Makes Certain Supplement Brands Uninsurable in Standard Markets

These brands can still get coverage through surplus lines markets, but rates are significantly higher and exclusions are broader. The earlier you address these underwriting factors, the more favorable your market options will be.

How to Evaluate Your Supplement Coverage Program Before a Claim Hits

A complete dietary supplement insurance program is not just one policy. Product liability is the foundation, but several coverage lines interact with it and fill gaps that your product liability policy alone will not cover.

Before reviewing the components of your program, confirm one critical policy-structure detail your broker should address at the application stage: whether your product liability policy is written on an occurrence basis or a claims-made basis. An occurrence policy covers any claim arising from a product sold during the policy period, even if the lawsuit is filed years after the policy expires.

A claims-made policy only covers claims filed while the policy is active. If you stop renewing a claims-made policy, every lawsuit filed after cancellation is uninsured, even if it involves product you sold years ago when the policy was in force. Supplement brands that eventually sell the company or exit the market are particularly exposed by claims-made policies without extended reporting period (tail) coverage. Ask your broker which form your program uses, and confirm the retroactive date goes back to when you first launched your product line.

When reviewing the coverage components of your supplement insurance program, confirm you have addressed each of these:

The Council for Responsible Nutrition publishes industry safety standards, GMP guidance, and regulatory compliance resources that directly inform both your risk management practices and your underwriting conversations. Brands that align their internal quality controls with CRN and industry standards are viewed more favorably by specialty carriers and can often demonstrate lower risk profiles that support better premium pricing.

Contact us to run a full coverage gap review. We review supplement brand programs at no cost and identify every gap before it becomes a claim.

Book a call and we will walk through your product list, your distribution channels, and your current policy in one focused conversation. Most supplement brands we work with are underinsured in at least two areas they did not know about.

Frequently Asked Questions About Dietary Supplement Product Liability Insurance

Get the Right Coverage for Your Supplement Brand

Supplement product liability is not a standard placement. The Coyle Group works with specialty markets that understand the ingestible risk category and structures programs that actually cover your product mix. Whether you manufacture, private-label, import, or distribute dietary supplements, we review your current coverage at no cost and identify every gap before a claim makes it relevant.

Your job is to know your products and your distribution. Our job is to build the right policy around both.

We turn compliant quotes around in 24 hours, or 2 hours if urgent. We review existing policies at no cost. And we work with brands at every stage, from startup SKUs to multi-channel wholesale operations with complex ingredient profiles.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s how to take the next step

Schedule Your Supplement Coverage Review

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage.”

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?