MSP Insurance

What Managed Service Providers Actually Need (And What Most Get Wrong)

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

You built your MSP (Managed Service Providers) to solve your clients’ technology problems. You monitor their networks, manage their backups, handle their infrastructure, and show up when things go wrong.

MSP insurance is not a line item to add later. It is the financial barrier between a single bad incident and the end of your business.

Any of these can generate claims in the six to seven-figure range, and if your coverage is wrong, you pay out of pocket.

Most MSP (Managed Service Providers) owners either skip MSP insurance entirely, buy a generic business policy from a broker who does not understand IT service businesses, or end up with coverage that looks good on paper but has enough exclusions to deny the exact claim they would need it for.

This page breaks down exactly what MSP insurance is, what coverage types you need, what your clients expect you to carry, what it costs by business size, and the most common mistakes that leave managed service providers exposed when a real claim hits.

What Is MSP Insurance and Why Is It Different From Standard Business Insurance?

MSP insurance is a bundled set of commercial policies built specifically for managed service providers. It covers professional errors, data breaches, client contract disputes, and technology liability that standard business insurance ignores entirely, but the real difference goes deeper than policy names.

MSP insurance is not the same as a standard business policy, and buying the wrong type is one of the most expensive mistakes a managed service provider can make.

The risks MSPs carry are fundamentally different, and standard policies were not designed to address them. Understanding that difference is the first step to building the right coverage program.

A standard Business Owner’s Policy (BOP) was built for brick-and-mortar businesses. It covers slip-and-falls, property damage, and basic liability.

What it does not cover is what actually threatens an MSP:

When you operate as an MSP, your risk profile includes:

Generic business insurance does not address any of this. MSP insurance needs to be purpose-built for the IT services industry, and placing it correctly requires a broker who understands how technology businesses are underwritten.

Not sure if your current MSP insurance policy actually covers your risks? We will review it in plain language, no jargon.

What Are the Most Common Claims Filed Against MSPs?

The most common claims against MSPs are professional liability disputes over service failures, cyber incidents tied to client data breaches, and contractual disagreements over SLA performance. Ransomware events and failed backups top the list, but one claim type consistently surprises MSP owners the most.

The claim that takes down an MSP rarely comes from the scenario you anticipated. It is usually the routine job that goes sideways, or the client network you have managed for three years that quietly accumulates a vulnerability you did not catch in time. Knowing which claims actually get filed is essential to building the right MSP insurance program.

The most frequently filed claim types in the MSP space include:

None of these scenarios are fully covered by a single policy. An MSP with only general liability is fully exposed the moment a cyber or professional liability claim is filed. The right MSP insurance program layers multiple coverages to close every gap. Understanding which layers you need is exactly what the next section addresses.

What Types of Insurance Do Managed Service Providers Need?

A complete MSP insurance program requires, at a minimum, Technology E&O, Cyber Liability, General Liability, and Workers’ Compensation. Most growing MSPs also need a Business Owner’s Policy, Employment Practices Liability, and Commercial Auto. Each covers a different risk, and the one most MSPs skip is usually the one that hurts them.

Most MSPs need a stack of policies, not just one. The right MSP insurance combination depends on your size, the types of clients you serve, and what those clients contractually require. Each coverage type addresses a distinct risk category, and the gaps between policies are exactly where claims go unpaid. Understanding the full map is what separates genuine protection from paperwork.

Technology Errors and Omissions Insurance (Tech E&O)

Tech E&O is the most critical policy in any MSP insurance program. It is the technology-specific form of errors and omissions insurance and protects you when a professional error in your IT services causes a client to suffer a financial loss. This includes botched configurations, failed migrations, inadequate system monitoring, and service interruptions tied directly to your work product.

Key coverage points:

Cyber Liability Insurance

A cyber insurance policy covers the costs of a data breach or cyberattack, including both first-party costs (your own response) and third-party costs (client or regulatory claims against you). For MSPs managing client networks and data, cyber liability is non-negotiable. According to data from ConnectSecure, 91.7% of MSPs already carry cyber insurance, which reflects how central it has become to operating in this industry.

Key coverage points:

General Liability Insurance

General liability (GL) covers third-party bodily injury, property damage, and personal injury claims, including advertising injury and defamation. For an MSP, this covers scenarios like a client being injured at your office or a lawsuit alleging your marketing damaged a competitor’s reputation. It is a foundational coverage, but it does not stand alone as adequate MSP insurance.

Key coverage points:

Workers’ Compensation Insurance

Workers’ compensation insurance is mandatory in virtually every state once you have employees. It covers medical bills and lost wages for employees injured or made ill on the job, and it protects you from employee lawsuits related to workplace injuries. With approximately 3 million workplace injuries reported annually in the United States, this is a required component of any complete MSP insurance program.

Key coverage points:

Business Owner’s Policy (BOP)

A BOP bundles general liability and commercial property insurance into a single, typically discounted policy. It is an efficient way for small to mid-size MSPs to cover core property and liability risks. The BOP also includes business interruption coverage, which replaces lost income if a covered event forces temporary closure.

Key coverage points:

Employment Practices Liability Insurance (EPLI)

EPLI protects your business from claims made by employees alleging discrimination, wrongful termination, sexual harassment, or other employment-related violations. As MSPs hire and scale, this coverage becomes increasingly important, particularly in states with aggressive employment litigation environments.

Key coverage points:

Commercial Auto Insurance

If your technicians or employees drive vehicles for work purposes, including service calls, equipment deliveries, or client site visits, you need commercial auto coverage. Personal auto policies specifically exclude business use, which means an accident on a client call is uninsured under a personal policy.

Key coverage points:

Explore how these coverage types map to different business structures at the insurance by coverage hub.

Trying to figure out which MSP insurance policies your business actually needs? We will build a coverage map specific to your size, client base, and contract requirements.

Tech E&O vs. Cyber Liability vs. Professional Liability: What Is the Actual Difference for an MSP?

These three coverage types are the most misunderstood part of MSP insurance, and the confusion is expensive. Assuming that one policy covers what another actually handles is one of the most common reasons MSP claims go partially or fully unpaid. The distinction matters more for managed service providers than it does for almost any other business type.

Here is how each one works and where the lines blur:

Coverage Type |

What It Covers |

|

Tech E&O |

Your professional errors in IT service delivery |

|

Cyber Liability |

Breach response costs, ransomware, regulatory fines |

|

Professional Liability |

Broader negligence in your professional capacity |

The overlap that determines your protection:

Human error drives 68% of all data breaches, according to industry research. That statistic is critical for MSPs, because it means a single incident can simultaneously trigger a Tech E&O claim (your error created the vulnerability) and a Cyber Liability claim (a breach occurred and client data was exposed). Carrying only one policy leaves a gap that the other policy’s exclusions will not fill.

What to verify in your policy language before binding:

These details do not appear on a Certificate of Insurance. They are buried in policy language, and a generalist broker who has not placed MSP insurance before will miss them entirely.

Real-World Example

An MSP managing IT infrastructure for a regional healthcare practice pushed a remote update to client workstations. A configuration error in the update disabled a firewall rule, leaving a port open. Three weeks later, a threat actor exploited the open port and accessed patient records, triggering a HIPAA breach notification requirement. The healthcare practice filed claims totaling $340,000 covering breach notification costs, regulatory investigation fees, and lost revenue during system recovery.

The MSP’s general liability policy was silent on the claim. Their cyber liability policy covered the breach response costs. Their Tech E&O policy covered the professional negligence that created the vulnerability. Having both policies meant the claim was fully covered. Having only one would have left a six-figure gap.

How Much Does MSP Insurance Cost? Realistic Ranges by Business Size

MSP insurance cost is not a fixed number, and the ranges published by most online sources are too broad for reliable budgeting. What you actually pay depends on your revenue, employee count, client types, coverage limits, documented security controls, and claims history. Here are realistic benchmarks by business size, along with the factors that push premiums up or down.

MSP Size |

Annual Premium Range (Core Stack: GL, Cyber, Tech E&O, Workers Comp or BOP) |

|

Solo / 1-2 employees |

$2,000 to $8,000 per year |

|

Small (5-10 employees) |

$8,000 to $25,000 per year |

|

Mid-size (20+ employees) |

$25,000 to $75,000+ per year |

Factors that increase your MSP insurance premiums:

How to reduce your MSP insurance costs without reducing coverage:

We do not give ranges. We get you a real number based on your actual business.

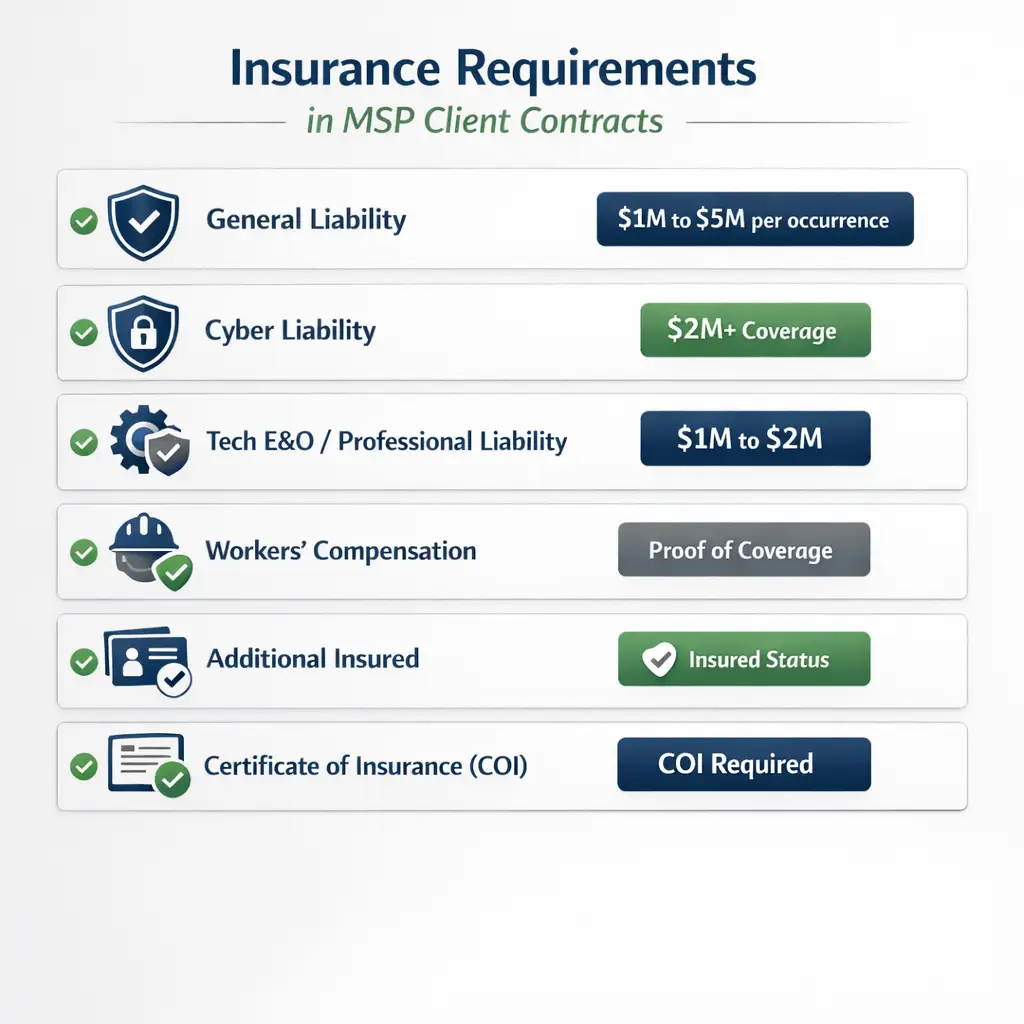

What Do Your Clients Expect You to Have? Understanding Contract Insurance Requirements

Client contracts are one of the most frequently overlooked drivers of MSP insurance decisions. What your clients require in their vendor agreements directly determines the minimum limits your MSP insurance program must carry, and failing to meet those requirements does not just risk losing the contract. It creates coverage gaps that can void your protection at the worst possible moment.

Typical insurance requirements in MSP client contracts include:

What “Additional Insured” actually means in practice:

When a client requires Additional Insured status, they are asking to be covered under your liability policy if a claim arises from your work affecting them. This is a standard and reasonable requirement, but it only functions correctly if your policy includes a blanket additional insured endorsement. Without it, you must add each client individually, and gaps can form if a client is not properly endorsed.

The prior acts clause that most MSPs miss:

Many E&O and Tech E&O policies are written on a claims-made basis. This means the policy only covers claims that are both filed and reported during the active policy period. Without a retroactive date or prior acts coverage, a claim filed today for work you performed two years ago may not be covered, even if you had insurance continuously throughout that time.

This gap typically surfaces only when a claim is actually filed, which is the worst possible moment to discover it. Before binding any claims-made policy, confirm the retroactive date in writing with your broker.

The 5 Biggest Insurance Mistakes MSPs Make

In my experience working with commercial insurance clients across technology and professional services businesses, certain patterns repeat. These five MSP insurance mistakes are the ones that leave managed service providers financially exposed at precisely the moment they need coverage most.

Carrying limits below what your client contracts require

If your client contract requires $2M in cyber liability and you carry $1M, you are in breach of contract from the day you sign, and you are personally liable for any gap above your policy limit. Audit your coverage limits against every active client contract every time your policy renews.

Using a broker who does not specialize in MSP insurance

A generalist insurance agent may place your MSP into a standard commercial BOP and consider the job done. Standard policies frequently contain exclusions for technology services, unattended software installations, and cyber events that make them nearly worthless for a managed service provider. An experienced MSP insurance broker knows exactly which exclusions to test for and which carriers write the coverage correctly.

Missing the prior acts clause in your E&O policy

As described above, claims-made policies without a retroactive date leave you exposed for all prior work. This detail does not appear on the certificate of insurance. It is in the policy documents, and it is easy to overlook unless your broker specifically confirms it.

Failing to fully disclose your risk profile at application

If you manage healthcare clients and do not disclose that, or if you handle financial data and omit it from your application, your insurer can deny a claim on the grounds of material misrepresentation. Disclose your full client base, the types of data you handle, and the industries you serve at application. This may increase your premium, but it prevents a denial at claim time.

Not reassessing your MSP insurance as your business grows

The policy you purchased when you had three clients will not adequately cover the risks you carry with thirty. Limits that were appropriate for a solo MSP are typically insufficient once you are managing healthcare networks or enterprise clients. Review your coverage at every renewal, not just when your broker sends the paperwork.

Connect with The Coyle Group to review your current insurance program and get an expert second opinion before your next renewal.

How to Find the Right Insurance Broker for Your MSP

Not every commercial insurance broker is equipped to handle MSP insurance correctly. The MSP insurance market is specialized enough that the broker you choose has a direct impact on whether you are actually protected when a claim happens, or whether you find out on the worst day of your business life that your policy has an exclusion that changes everything.

What to look for in an MSP insurance broker:

Questions to ask a broker before you bind any MSP insurance policy:

If a broker cannot answer those questions clearly and specifically, that is important information. The right answers come from someone who has navigated MSP claims before.

The MSPAlliance and CompTIA both publish guidance on risk management for managed service providers that can help you benchmark what a properly structured MSP insurance program looks like before you have that conversation.

Ready to build the right MSP insurance program? We specialize in commercial insurance for technology businesses. We will review your current program, identify gaps, and show you exactly what a complete coverage stack looks like for your size and client base.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

Frequently Asked Questions About MSP Insurance

Get the Right Coverage for Your MSP

With over 40 years of experience placing commercial insurance for technology service businesses, Gordon B. Coyle understands the specific risks MSPs carry: professional errors in IT service delivery, cyber incidents tied to client network management, and the contract requirements that determine whether a policy actually pays when a claim happens.

At The Coyle Group, we specialize in commercial insurance for technology businesses. We know which carriers write MSP insurance correctly, which exclusions to test for before binding, and how to structure a coverage stack that satisfies client contract requirements while protecting your business from the claims that actually happen.

If you are ready to review your current MSP insurance program or build the right coverage from the ground up.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?