Insurance for Investment Banking Firms

What You Need, What Clients Require, and How to Buy It

How To Get The Right Insurance For Investment Banking Firms

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

If you run a boutique investment bank, M&A advisory firm, or placement agent, your fee-based work creates liability exposures that standard business insurance simply doesn’t address.

TL;DR. The Bottom line

Put simply, Investment banking combines high-stakes advice with complex transactions. Consequently, every fairness opinion, every engagement letter, and every deal document creates potential legal liability. Meanwhile, clients require specific insurance certificates before they’ll sign, lenders demand proof of coverage, and counterparties expect your firm to be financially protected.

Yet most investment banks struggle to understand what insurance they actually need versus what they can skip. Furthermore, they’re unclear about which policies respond to which claims, and how to satisfy contract requirements without buying redundant coverage.

The Coyle Group specializes in building insurance programs for financial services firms. As a result, we understand the difference between transaction risk and operational risk, and we know how to structure coverage that protects your leadership while satisfying your strictest client requirements. Our approach to financial services insurance addresses the unique exposures investment banks face.

To identify gaps in your current coverage before your next deal closes.

Why Do Investment Banking Advisors Need Specialized Insurance?

Investment banking advisors operate in a unique risk environment. Your work revolves entirely around professional judgment: the fairness opinions you render, the valuations you prepare, and the strategic advice you provide on transactions worth millions or billions of dollars. Every opinion letter, every engagement, and every deal document creates potential legal liability.

As a result, this creates two-directional financial exposure. First, there are your own costs when something goes wrong. Legal defense alone can exceed $500,000 even if you win. Second, there are claims from others who believe your advice, execution, or documentation caused them financial harm.

What “Contract-Ready” Really Means

When clients, lenders, or counterparties require insurance certificates, they’re not just checking a box. Rather, they’re verifying that your firm has sufficient financial capacity to respond to claims without declaring bankruptcy or forcing them into protracted collection efforts. That’s the difference between a COI that closes deals and one that stalls them.

Being contract-ready means having coverage that actually responds to the scenarios in your engagement letters. Additionally, it requires limits high enough to satisfy client requirements, and endorsements that provide the additional insured status and waivers your contracts demand.

What Does “Investment Banking Insurance” Actually Mean?

Investment banking insurance isn’t a single policy. Instead, it’s a coordinated stack of coverages designed to address different risk categories.

Unlike standard business insurance, it’s structured around the specific liability exposures of advisory work, M&A transactions, capital raises, engagement failures, and management decisions, not physical risks or general operations.

To illustrate, standard business insurance, like general liability, handles slip-and-fall accidents and property damage at your office. However, it completely excludes professional advice, financial recommendations, and management decisions. Similarly, basic property policies protect your furniture and computers but ignore the digital threats that can paralyze your operations.

The Three Core Risk Buckets

Advice Risk

Claims that your professional services caused financial harm

Governance Risk

Allegations that leadership made wrongful management decisions

Operational Risk

Cyber attacks, fraud, and system failures that create direct losses or third-party liability

Each bucket requires different insurance coverage that responds to different triggers and provides different types of protection.

What Insurance Does an Investment Banking Firm Typically Need?

Most boutique banks need $2M to $5M in E&O coverage, $3M to $10M in D&O limits, and $1M to $5M in cyber protection depending on deal size and client requirements.

What Does Investment Banking E&O Cover (and What Does It Not)?

Professional Liability insurance (also called E&O) is the foundation of your protection as an advisory firm. Specifically, this policy responds when someone alleges your professional services caused them financial harm.

For investment banking firms, E&O is the policy that responds when a client claims your advice, your process, or your documentation caused them financial loss, regardless of whether the claim has merit.

What’s Covered

What’s NOT Covered

On the other hand, most E&O policies specifically exclude:

Common Claim Triggers

What CFOs Should Verify Before Binding

According to research, typical E&O retentions for investment banks range from $25,000 to $250,000 per claim, with some larger firms carrying $500,000 retentions to reduce premium costs.

To verify that it actually covers fairness opinions, valuations, and M&A advisory work.

What Does Investment Banking D&O Cover (and Why Do Firms Need It Early)?

Directors and Officers insurance protects your leadership team and the firm itself from management liability claims. Notably, even boutique investment banks without formal boards face significant D&O exposure.

For boutique and mid-market firms, D&O is often triggered before E&O, partner disputes, FINRA investigations, and investor allegations frequently target individuals personally before they become entity-level claims.

What’s Covered

Why Early-Stage Banks Get Hit

Many small investment banks assume D&O claims only happen to public companies. In reality, however, D&O exposure exists whenever:

Understanding Side A, B, and C Coverage

Side A

Protects individual directors and officers when the company cannot or will not indemnify them (such as in bankruptcy)

Side B

Reimburses the company for amounts paid to indemnify directors and officers

Side C

Covers the entity itself for securities claims and other specified wrongful acts

Investment banks should pay particular attention to Insured vs. Insured exclusions, which can eliminate coverage for disputes between partners or claims by the firm against its own leadership.

Investigations Coverage

D&O policies typically define “claim” to include formal regulatory investigations, but the trigger varies by carrier. Some respond when you receive a Wells Notice or target letter. Others require a formal proceeding to be commenced.

For investment banks subject to FINRA oversight, investigations coverage is critical and should include coverage for informal inquiries that can still cost $50,000 to $200,000 in legal fees.

To ensure your leadership team has proper protection against investor and regulatory claims.

What Does Cyber Insurance Cover for Investment Banks (and Where Does It Break)?

Cyber insurance has become essential for investment banks handling confidential deal information, managing electronic funds transfers, and relying on cloud-based systems for operations.

For investment banking firms, the key exposures are deal information breaches, business email compromise targeting wire transfers, and ransomware disrupting time-sensitive transaction processes where downtime has direct financial consequences.

What’s Covered

Where Coverage Breaks

Vendor Outages

Most cyber policies won’t cover lost revenue when your Bloomberg terminal, CRM, or cloud accounting system goes down unless you specifically purchase dependent business interruption coverage

Waiting Periods

Many business interruption provisions require 8 to 24 hours of downtime before coverage kicks in

Panel Vendor Requirements

Some carriers require you to use their approved incident response firms rather than letting you choose your own

Failure to Maintain Controls

If you don’t implement MFA, endpoint detection, or verified backups, the carrier may deny your claim under a “failure to maintain reasonable security” provision

Essential Questions Before Binding

According to Munich Re’s 2025 cyber insurance analysis, the global cyber insurance market is projected to reach $16.3 billion in 2025, reflecting the growing recognition of cyber risk across all industries.

What Does Crime Insurance Cover (and Why Does Cyber Not Replace It)?

Crime insurance is the most commonly overlooked coverage in investment banking insurance programs. Yet it addresses one of your highest-frequency threats.

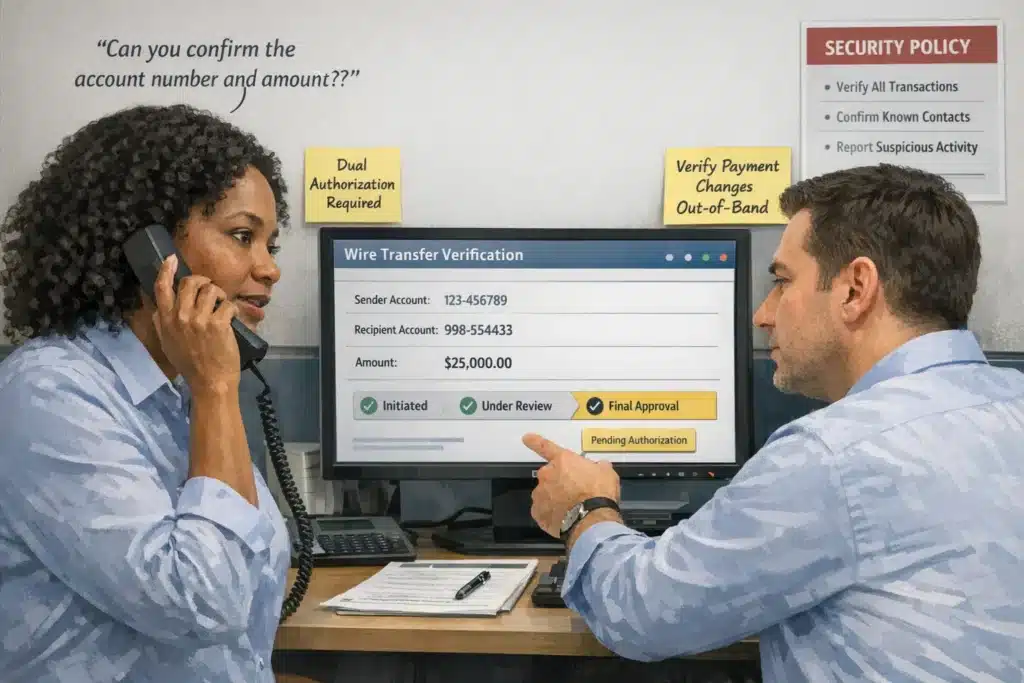

Investment banks are frequent wire fraud targets, social engineering attacks impersonating clients, counterparties, or senior partners to redirect deal-related transfers are among the highest-dollar crime claims in financial services.

What Crime Insurance Covers

Why Cyber Isn’t Enough

Many firms assume their cyber policy covers wire fraud. However, cyber insurance and crime insurance have different coverage triggers.

For more clarity on this distinction, review our guide on cyber insurance versus crime insurance.

Real-World Investment Banking Scenarios

Scenario 1

Your CFO receives an email from what appears to be the CEO requesting an urgent wire transfer to close a time-sensitive deal. The email is actually from attackers who’ve spoofed the CEO’s address. Your firm wires $350,000 before discovering the fraud.

Response

Crime insurance with social engineering coverage would respond. Standard cyber insurance might exclude this because there was no breach of your systems.

Scenario 2

You’re closing an M&A transaction and receive updated wire instructions from the seller’s counsel. Unknown to you, the seller’s law firm has been compromised and the wire instructions are fraudulent. You send $2.8M in escrow funds to the wrong account.

Response

This falls into a gray area where both crime and cyber policies might respond, but coverage often depends on specific policy language around client funds and third-party fraud.

Prevention Controls That Underwriters Reward

According to the FBI’s Internet Crime Complaint Center, business email compromise losses exceeded $2.9 billion in 2023, making it one of the costliest cyber crimes for businesses.

And verify whether your current policies coordinate properly between cyber and crime coverage.

What Are the Most Common Claim Scenarios for Investment Banking Firms?

Understanding how claims actually arise helps you recognize why specific coverages matter. Moreover, it clarifies how different policies might respond to the same incident.

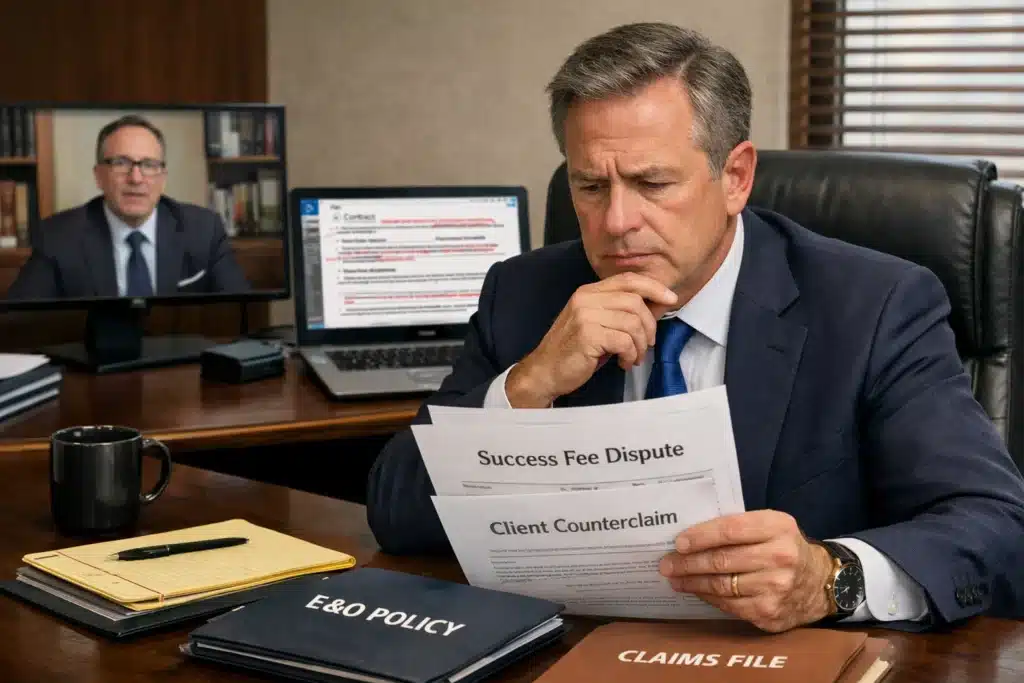

Engagement Letter Dispute Evolves Into Negligence Claim

Fairness Opinion Challenged Post-Close

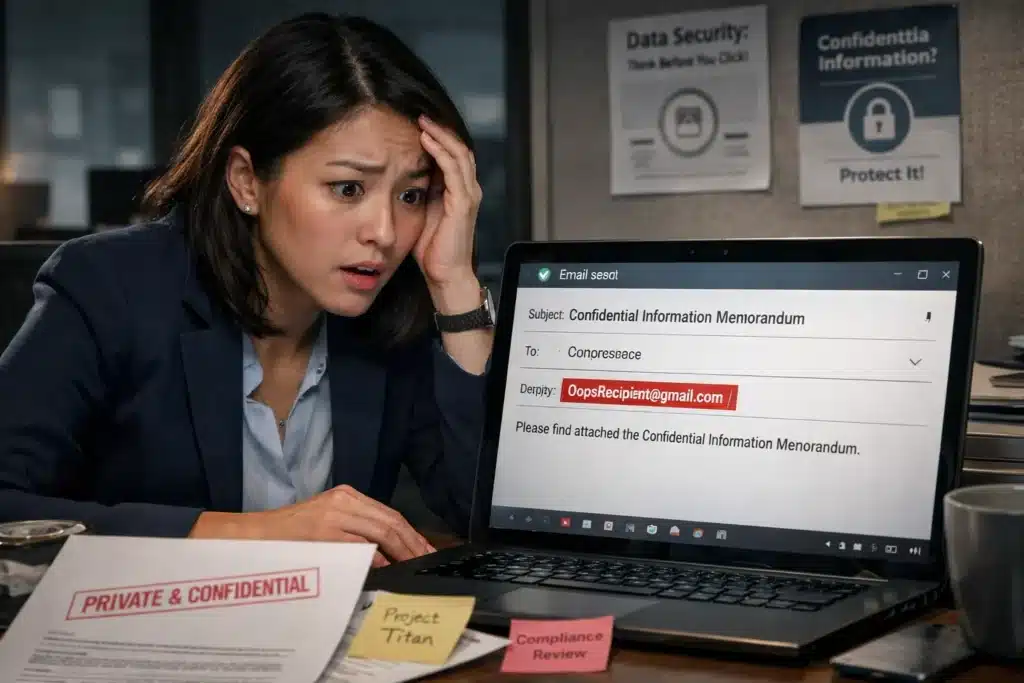

Confidential Information Disclosed Accidentally

Business Email Compromise Leads to Fraudulent Wire Transfer

Employee Termination Escalates to Retaliation Claim

Regulatory Inquiry Into Supervision and Disclosures

Who Can Sue an Investment Banking Firm (and Why Does That Matter for Limits)?

Understanding your potential plaintiffs helps determine appropriate coverage limits. Therefore, it’s essential to recognize all possible claim sources.

Direct Clients

Your sell-side or buy-side clients can sue for negligence, breach of engagement, or failure to perform promised services. These claims trigger your E&O policy.

Target Companies and Their Shareholders

Even when you’re not directly hired by them, targets and their shareholders can claim your fairness opinion was negligent or biased. Minority shareholders are particularly likely to challenge valuations after transactions close.

Investors and Lenders

Private equity investors, venture capital funds, and lenders who relied on your analysis or due diligence can sue if deals go bad. Third-party reliance claims are common in financial services.

Counterparties to Transactions

Other parties to deals, including placement agents, co-advisors, and financing sources, can bring claims if they believe your actions harmed their interests.

Employees and Former Partners

Employment claims and partner disputes create both EPLI and D&O exposure, particularly when compensation arrangements involve profit participation or carried interest.

Regulators

SEC, FINRA, and state securities regulators can bring investigations and enforcement actions that trigger D&O coverage for regulatory proceedings.

The key insight

Multiple parties can sue over a single transaction. A challenged fairness opinion might trigger claims from the client who hired you, shareholders who opposed the deal, and investors who financed it. Each claim can consume policy limits, which is why adequate limits and proper structure matter.

What Do Clients, Lenders, and Counterparties Require on a COI?

Certificates of Insurance (COIs) are the documents that prove your coverage to third parties who require it. Understanding common requirements helps you structure policies that actually satisfy contract obligations.

Typical Requirement Buckets

Minimum Limits by Coverage Type:

Additional Insured Requests

Most common on general liability policies when you’re visiting client sites or attending industry events. Less common (but not impossible) on E&O policies for specific engagements.

Waiver of Subrogation

Prevents your insurer from suing the client to recover amounts paid on a claim. This is standard on GL policies, less common on professional liability.

Primary and Noncontributory Language

Ensures your insurance pays before the client’s insurance. Typically applies to general liability, not professional liability.

Notice of Cancellation

Requires your insurer to notify the certificate holder if your policy is cancelled or non-renewed. Most carriers will provide 10 days’ notice for non-payment and 30 days for non-renewal, but they won’t guarantee specific notice periods to third parties beyond what’s in the policy.

COI Requirement Checklist

Before signing an engagement letter with insurance requirements, verify:

Pro tip

Share your standard engagement letter with your broker before signing deals. They can identify insurance requirements that need attention and help you negotiate feasible alternatives if requirements exceed available coverage.

What Contract Terms Can Accidentally Create Uninsured Liability?

Engagement letters and transaction documents sometimes include language that creates insurance problems. As a result, careful review is essential.

Uncapped Indemnity Obligations

The Problem: When you agree to indemnify a client without any limitation of liability, you’ve potentially exceeded your insurance limits and created personal liability.

Better Approach: Cap indemnification at 1-2x your engagement fee or negotiate limits that align with your E&O coverage.

Assuming Another Party’s Negligence

The Problem: Agreeing to defend and indemnify a client even for their own negligent acts typically voids insurance coverage. Most E&O policies exclude assumed liability beyond what you’d have at common law.

Better Approach: Limit indemnification to claims arising from your own negligence, not the client’s acts.

“All Losses” vs. “Damages” Language

The Problem: “All losses” can include items insurance doesn’t cover, such as lost profits, opportunity costs, or consequential damages.

Better Approach: Define covered damages narrowly to match insurance policy language.

Guaranteeing Outcomes or Performance

The Problem: Promising specific results, valuations, or transaction success typically falls outside E&O coverage, which protects against negligent performance, not guaranteed outcomes.

Better Approach: Frame your obligations as “best efforts” or “professional standards” rather than guaranteed results.

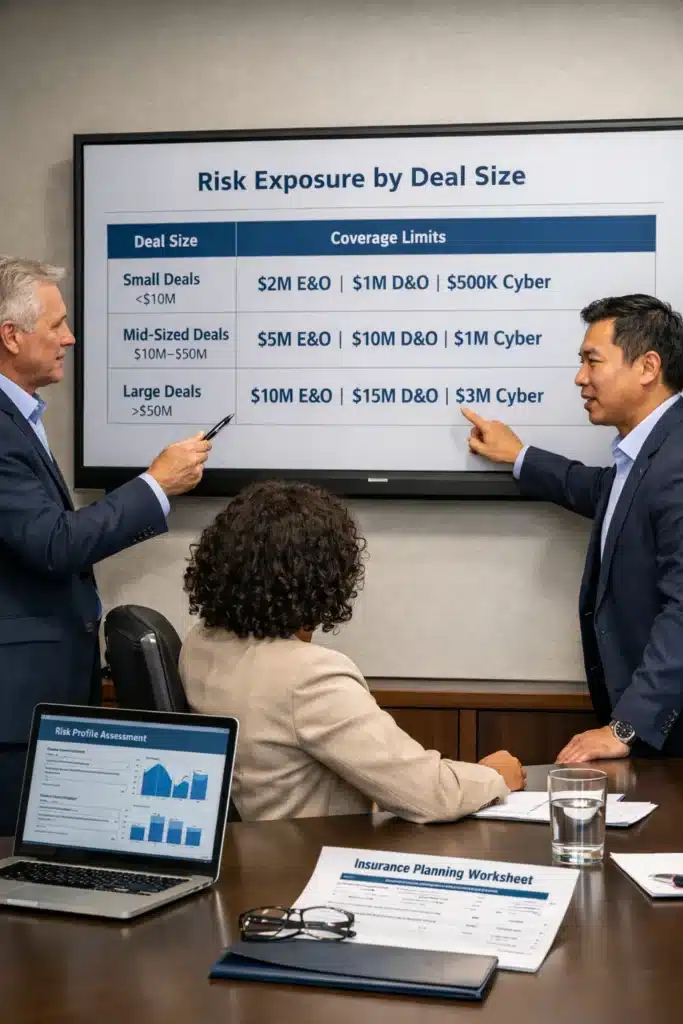

How Much Coverage Should an Investment Banking Firm Buy?

Determining appropriate limits requires understanding your specific risk profile rather than applying generic rules. Consequently, several factors must be considered.

Start With These Factors

Limit-Sizing Frameworks

Real Numbers From the Market

According to industry data, typical investment banking insurance programs include:

Cyber insurance typically ranges from $1M to $5M regardless of firm size, while crime coverage runs $1M to $3M depending on funds movement volume.

Why Are Retentions So High for E&O and D&O (and How Should We Think About Them)?

Investment banking retentions (also called deductibles or self-insured retentions) are significantly higher than retentions for most other types of insurance. Understanding why helps you make informed decisions.

What a Retention Actually Means

Your retention is the first dollars you pay per claim before insurance coverage kicks in. If you have a $100,000 retention and a $300,000 claim, you pay $100,000 and the insurer pays $200,000.

Why Retentions Are High

How to Choose Your Retention

Match to Liquidity

Choose a retention that your firm can comfortably pay from operating cash or readily available credit. Don’t select a $250,000 retention if you only have $100,000 in liquid reserves.

Avoid “Paper Coverage”

Setting a $500,000 retention to reduce premiums only works if you can actually pay $500,000. If you can’t, the savings are illusory.

Consider Premium Savings

Moving from a $50,000 to a $100,000 retention might save 15-25% in premium. Moving from $100,000 to $250,000 might save another 15-20%. Run the numbers.

Inside vs. Outside Defense Costs:

Some policies include defense costs in the retention (you pay defense costs until hitting your retention). Others cover defense costs immediately and the retention only applies to settlements and judgments. Inside retention policies require higher liquidity.

Typical Retention Ranges

What Drives Investment Banking Insurance Pricing?

Understanding pricing factors helps you control costs. Moreover, it reveals where you have leverage in negotiations.

Major Pricing Factors

Cost Levers You Control

From a broker who specializes in financial services, insurance, and understands investment banking risk.

What Questions Should a CFO or CEO Ask Their Broker Before Binding?

These questions reveal whether your broker truly understands investment banking coverage. Alternatively, they show if the broker is just filling in application fields.

Coverage Questions

Process Questions

Relationship Questions

What 40+ Years Taught Me About This Risk

The brokers who can’t answer these questions specifically are the ones whose clients discover coverage gaps when claims arise. Investment banking insurance requires specialized knowledge, not just access to E&O markets.

CASE STUDIES

Real Insurance Outcomes

Explore real-world insurance case studies that show how we helped businesses identify coverage gaps, solve complex risk challenges, strengthen protection, and achieve better insurance outcomes.

Questions About Investment Banking Insurance?

Your Next Step: Building Contract-Ready Coverage

Most investment banking firms discover insurance gaps only when clients reject their COIs or when claims arise. By that point, fixing coverage problems is expensive or impossible.

The Coyle Group specializes in building insurance programs for financial services firms that:

For related guidance on protecting your firm, explore our resources on D&O insurance for private funds and investment management insurance.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping investment banking firms, hedge funds, and investment management firms develop comprehensive insurance programs that protect their operations and support their growth objectives.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?