Quick Answer

The workers comp valuation date is the specific day each year when your payroll and claims data for the past three years is sent to the workers comp rating bureau to calculate your experience modification factor (E-Mod). Because approximately 80% of data submitted contains errors, reviewing and correcting your underlying data before the valuation date can significantly reduce your premium. Once data is submitted, it locks in for the upcoming renewal cycle and cannot be corrected until the following year.

What Is the Workers Comp Valuation Date and Why It Controls Your Premium

Your valuation date determines how much you pay for workers comp for the next 12 months. Most business owners have never heard of it.

On the valuation date, three years of payroll and claims data is submitted to the rating bureau. That data is used to calculate your E-Mod, which multiplies your base premium. Approximately 80% of submissions contain errors. Once submitted, the data locks in for the full renewal cycle. You cannot correct it until the following year.

The workers comp valuation date is the single most impactful administrative date in your entire insurance program.

Every year, on a specific date tied to your policy anniversary, all of your workers compensation payroll data and claims information from the past three years is submitted to your state’s rating bureau.

That bureau uses this data to calculate your experience modification factor, the E-Mod or X-Mod, which directly multiplies your base workers comp premium. An E-Mod of 1.35 means you pay 35% above the industry baseline. An E-Mod of 0.85 means you pay 15% below it.

Approximately 80% of data submitted to rating bureaus contains errors. Classification errors, incorrect payroll allocations, open reserves on settled claims, and claims coded to the wrong policy period are common.

Once submitted on the valuation date, this data locks in for your upcoming renewal. You cannot correct it until the following year.

How the workers comp experience mod is calculated and why it matters for your premium

The 80% Error Problem: Why Your Data Is Probably Wrong

Approximately 80% of experience rating worksheets submitted to rating bureaus contain at least one error that artificially inflates the mod. This is not a minor technical issue. It is why businesses overpay for workers comp year after year without understanding why.

The four most common error categories are classification misassignments, open reserves on settled claims, incorrect policy period allocations, and payroll miscoding. Each type inflates the E-Mod by a different mechanism, and each is correctable before the valuation date if identified in time.

What 40+ Years Taught Me About Workers Comp Data

In four decades of managing workers comp programs for businesses, I have never seen an experience mod that couldn’t be improved by reviewing the underlying data. The question is never whether errors exist. The question is how much they’re costing you and whether you find them before the valuation date or after. Once the data is locked in, you’re paying for those errors for the entire renewal cycle.

Mod Audits vs. Pre-Valuation Date Review: A Critical Distinction

A mod audit corrects past errors after you’ve already paid inflated premiums. Pre-valuation date review prevents those errors from being submitted at all. The financial difference over a three-year rating window is substantial.

Most businesses are familiar with mod audits. Fewer understand that correcting errors before the valuation date avoids overpayment entirely, rather than recovering a partial refund months or years after the fact.

Approach |

When Errors Are Corrected |

Premium Impact |

|---|---|---|

|

Mod audit (reactive) |

After submission, often 12-24 months later |

Partial refund of overpaid premium |

|

Pre-valuation date review (proactive) |

Before submission, before renewal |

No inflated premium paid at all |

|

No review |

Never |

Overpayment continues for full rating window |

What to Review Before Your Valuation Date and When to Start

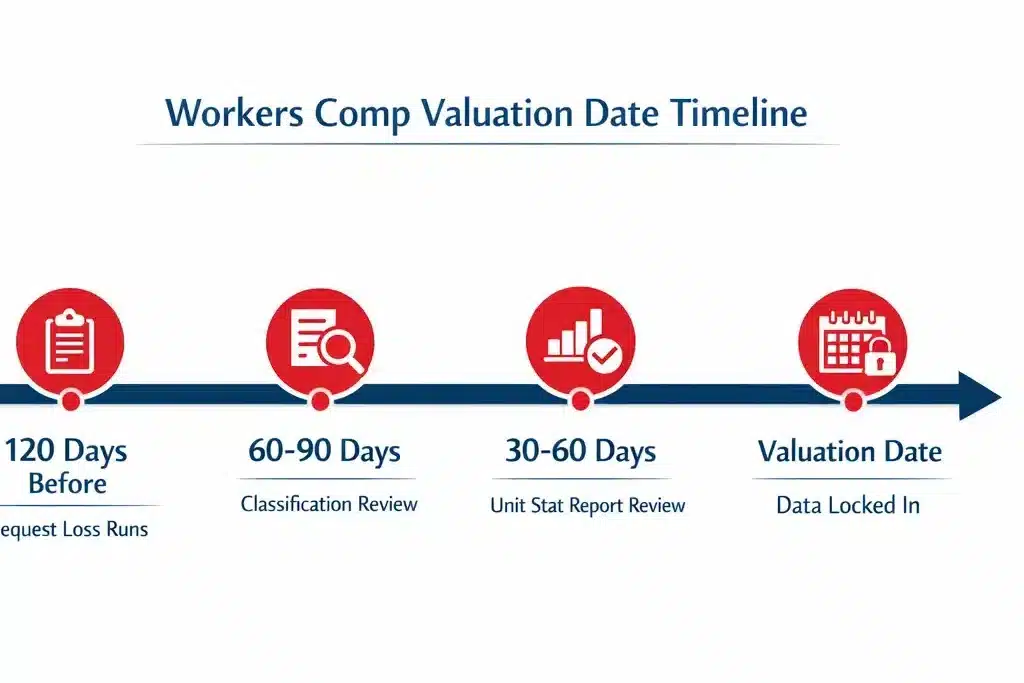

Start 90 to 120 days before your valuation date. The three review components are payroll data, claims reserves, and classification codes. Each one directly affects the E-Mod calculation.

Completing this review on time gives adequate opportunity to identify errors, coordinate with your carrier and broker, and ensure corrected data reaches the bureau before the submission deadline. Missing the window means waiting another full year.

Understanding your experience rating mod in detail before the valuation date gives you the best opportunity to identify and correct errors. Integrating this review into your annual business insurance program review ensures it never gets missed.

Frequently Asked Questions About the Workers Comp Valuation Date

Author’s Expertise

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.