Who Is an Insured on a D&O Policy? Understanding Who Is Actually Protected

Directors & Officers (D&O) insurance is often described as “protecting leadership.” However, when a real issue arises, the most important question becomes far more specific:

Who is actually an insured on a D&O policy?

This matters because D&O claims almost always name individuals personally. If you assume you’re covered and you’re wrong, the consequences can be severe. This article explains who qualifies as an insured on a D&O policy, how broadly that definition is applied, and where misunderstandings commonly occur.

Who is considered an insured on a D&O policy?

An insured on a D&O policy is not listed by name on a schedule like a property policy.

Instead, D&O policies define insureds by role, not by individual identity. Accordingly, in most private company D&O policies, the definition of “Insured Person” broadly includes:

This is why adding a new board member does not require endorsement in most cases. Coverage attaches automatically based on the role, not the person.

Watch this short video for a clear breakdown of what’s actually covered under a D&O policy and common misconceptions about insured status

What 40+ Years Taught Me About This Risk

After working with hundreds of boards and executives, I’ve learned that most people don’t read their D&O policy until a claim hits. By then, it’s too late to fix gaps. The executives who avoid this trap treat their D&O policy as a personal asset protection document, not just corporate paperwork.

Why does it matter who is insured on a D&O policy?

Because D&O claims are personal.

Regulators, shareholders, employees, creditors, or other third parties often name:

If you are named in a lawsuit and you are not an insured, the policy will not defend you. Furthermore, there is no retroactive fix once a claim is made.

According to data from the National Association of Corporate Directors, litigation against directors and officers has increased significantly over the past decade, making proper coverage more critical than ever.

To see real-world examples of D&O claims and why understanding your insured status is critical, check out this video:

What is the difference between an insured person and an insured organization on a D&O policy?

D&O policies distinguish between two categories:

This distinction matters because different “Sides” of coverage apply depending on who is named and who pays the defense. Understanding whether you are protected personally is far more important than knowing whether the entity is insured.

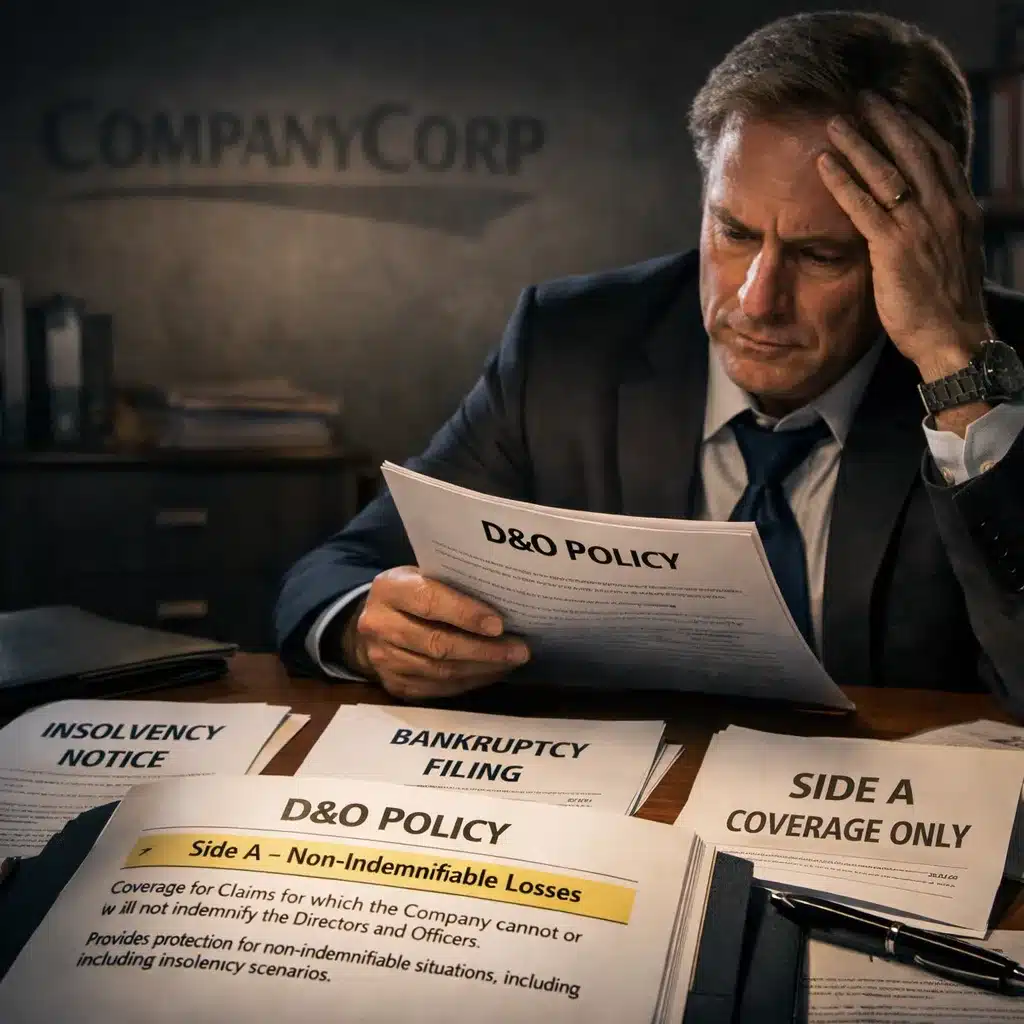

Real-World Example: The Side A Coverage Gap

A technology company’s CFO faced personal allegations of financial misrepresentation during bankruptcy proceedings. The company could not indemnify him due to insolvency. Without robust Side A coverage in his D&O policy, his personal assets would have been at risk for the $2.3 million defense and settlement costs.

Which directors are insured on a D&O policy?

In most private company D&O policies, all directors are insured, including:

There is no named schedule. Consequently, coverage is automatic based on status.

Which officers are insured on a D&O policy?

Officers are typically insured if they:

Titles alone are not always determinative. In reality, insurers look at function, not just job descriptions.

This is especially relevant in private companies where executives wear multiple hats.

Are former directors and officers insured on a D&O policy?

Yes, for acts committed during their tenure, assuming the claim is made while coverage is in force (or during an extended reporting period).

This is a key feature of claims-made coverage:

This is why continuity of coverage and tail policies matter so much in transactions or dissolutions. Moreover, according to Insurance Information Institute data, the majority of D&O claims involve acts that occurred years before the lawsuit was filed.

For a deeper understanding of how claims-made policies work and why former directors remain protected, watch this explanation:

Are employees insured on a D&O policy?

Sometimes, but not universally.

In many private company forms, the definition of Insured Person may include:

This becomes especially important when Employment Practices Liability Insurance (EPLI) is packaged with D&O.

How does EPLI affect who is insured under a D&O policy?

When EPLI is included in a management liability package, the insured definition often expands to cover individuals responsible for employment decisions, such as:

These individuals are insured only for employment-related acts, not for general management liability.

Are spouses, estates, or legal representatives insured on a D&O policy?

Yes, but in a limited, derivative way.

Most D&O policies extend insured status to:

However, coverage applies only when they are named solely because of their relationship to an insured person.

This prevents plaintiffs from bypassing coverage by suing family members. As a result, the policy protects against creative legal strategies designed to circumvent coverage.

Are advisory board members insured on a D&O policy?

Often, yes, but this is policy-specific.

Many private company D&O policies include advisory committee members within the insured definition. However, this varies significantly and must be confirmed in the policy language.

This is one of the most commonly overlooked coverage gaps. Additionally, companies should review their fiduciary liability coverage if advisory boards make investment or benefit decisions.

When does D&O insurance protect individuals versus the company?

This depends on the Side A / Side B / Side C structure:

For personal asset protection, Side A is the most critical.

What happens if the company cannot indemnify an insured person?

If the company is:

Then Side A coverage becomes the only line of defense.

This is why directors and officers should never evaluate D&O insurance solely based on entity coverage. In fact, the Delaware General Corporation Law contains specific provisions about when companies cannot indemnify their directors and officers.

What common assumptions do executives make about who is insured on a D&O policy?

The most dangerous assumptions include:

These assumptions are often proven wrong during claims. Consequently, executives should verify coverage before accepting board positions.

How can directors and officers confirm they are properly insured on a D&O policy?

Before a claim happens, executives should:

D&O insurance is a non-standard policy. Every form is different. Therefore, working with specialists who understand D&O coverage nuances is essential.

How can directors and officers make sure they are personally protected by their D&O insurance?

The safest approach is:

If something goes wrong, this policy is meant to protect you, not just the balance sheet. In addition, executives should understand what constitutes a wrongful act under their specific policy.

Frequently Asked Questions About D&O Insurance Coverage

Get Expert Guidance on D&O Coverage

Understanding who is actually insured on your D&O policy isn’t just about reading definitions. It’s about verifying that your personal assets are protected before a claim arises.

At The Coyle Group, we specialize in tailoring D&O coverage for executives, board members, and private companies. We ensure you understand exactly who is protected, in what circumstances, and with what limits.

To review your D&O coverage with an expert who focuses on personal asset protection, not just corporate compliance.

Author’s Expertise

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping directors, officers, and executives understand their personal liability exposures and structure D&O coverage that provides genuine protection when it matters most.