Contingent Business Interruption Insurance: Why Most Claims Get Denied

What Mid-Market Companies Get Wrong About Contingent Business Interruption Coverage

Business Interruption Insurance Explained

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Contingent business interruption insurance (CBI) covers income losses your business suffers when a key supplier, vendor, or technology platform experiences a covered disruption, even when your own facility is completely untouched. Standard business interruption coverage stops at your property line. CBI extends that protection into the supply chain dependencies your business relies on to operate.

Most mid-market companies either lack CBI coverage entirely, carry it with the wrong structure, or have never confirmed whether it would actually pay during a real supplier outage. The structural gaps, wrong trigger language, inadequate sublimits, and missing cyber provisions are invisible until a claim is denied.

This page covers why CBI claims get denied, how to structure the coverage correctly, and what to review before your next renewal.

After the CDK Global ransomware attack brought down operations at more than 15,000 auto dealerships across North America in June 2024, producing an estimated $1 billion in collective losses, business owners assumed their business interruption policies would respond. For most, they did not. The disruption happened at the vendor’s platform, not at their facility. Standard business interruption policies covered losses at their own premises. They did not follow the business into its supply chain.

At The Coyle Group, we specialize in complex, high-value risks that other agencies do not know how to structure. Contingent BI is one of the coverage areas we audit on nearly every commercial program review, because the structural gaps are that common and that costly.

Is Your Supply Chain Protected When a Supplier Goes Down?

Most standard business interruption policies only pay when your own facility is the source of the loss. When a supplier, vendor, or platform you depend on experiences an outage, the claim is frequently denied before it reaches an adjuster.

The Coyle Group has spent 40+ years helping mid-market and enterprise companies identify the coverage gaps their current broker never flagged. A 30-minute review of your current policy could reveal whether your contingent BI coverage would actually pay in a real supplier disruption.

What Is Contingent Business Interruption Insurance and Why Are Companies Getting Burned Without It?

Contingent business interruption insurance covers income losses your business suffers when a key supplier, vendor, or technology platform experiences a covered disruption, even if your own facility is completely untouched. Standard business income coverage stops at your property line. CBI extends that protection into your supply chain. But the conditions that trigger a payout are far narrower than most policyholders assume, and misunderstanding those conditions is the reason so many claims fail.

When the CrowdStrike software failure caused more than $5 billion in global business losses in July 2024, only an estimated $1.5 billion was recovered through insurance.

That $3.5 billion gap is exactly what properly structured contingent business interruption insurance is designed to close.

Supply chain disruption now ranks among the top global business risks, according to Allianz’s Business Interruption Trends Report. The global CBI market was valued at $8.7 billion in 2024 and is projected to reach $18.2 billion by 2033. According to the Business Continuity Institute’s Supply Chain Resilience Report, 80% of organizations reported at least one supply chain disruption in the prior 12 months.

When properly structured, contingent business interruption insurance can respond to:

Who carries the highest contingent business interruption exposure:

The Insurance Information Institute notes that many businesses carry CBI as a policy add-on without ever confirming whether the structure reflects their actual supply chain dependencies. That is the gap that produces denied claims.

Who Likely Does NOT Need Contingent Business Interruption Insurance

CBI adds less value when a business can quickly substitute alternative suppliers with minimal cost or revenue impact. If your operations can absorb a 30-day outage at any single supplier without material revenue disruption, your existing standard BI coverage is likely sufficient.

Businesses with highly diversified supplier networks across multiple geographies, short lead times, and no single-source component dependencies face lower CBI exposure and may not need the additional endorsement structure.

What Is an Example of a Contingent Business Interruption Loss?

In June 2024, CDK Global, the automotive software platform used by approximately 15,000 dealerships across North America, suffered a ransomware attack that took the platform offline for nearly two weeks. Dealerships reverted to manual processes. Sales slowed. Service departments shut down. Collective losses were estimated at $1 billion.

For most dealerships, this was a textbook contingent business interruption event: the loss originated at a third-party platform, not at the dealership’s own facility. Whether any individual dealership recovered depended entirely on three things: whether their policy required physical damage at a named supplier’s location, whether their CBI sublimit was large enough to cover the actual loss, and whether their cyber form covered third-party platform outages.

Many recovered nothing. Not because CBI coverage doesn’t exist, but because the coverage they carried wasn’t structured to respond to this type of event.

Contingent Business Interruption vs. Standard Business Interruption

Standard Business Interruption |

Contingent Business Interruption |

|

|---|---|---|

|

What triggers coverage |

Physical damage at YOUR location |

Physical damage at a SUPPLIER’S location (or broader trigger with endorsements) |

|

Where the loss must occur |

Your own premises |

A supplier, vendor, or key customer’s facility |

|

Cyber events |

Generally excluded |

Excluded by default; available via specific endorsement |

|

Named supplier requirement |

N/A |

May require suppliers to be listed by name |

|

Waiting period |

Typically 24–72 hours |

Typically 24–72 hours (separate from BI waiting period) |

|

Sublimit |

Your full BI limit applies |

A separate, often much lower sublimit applies |

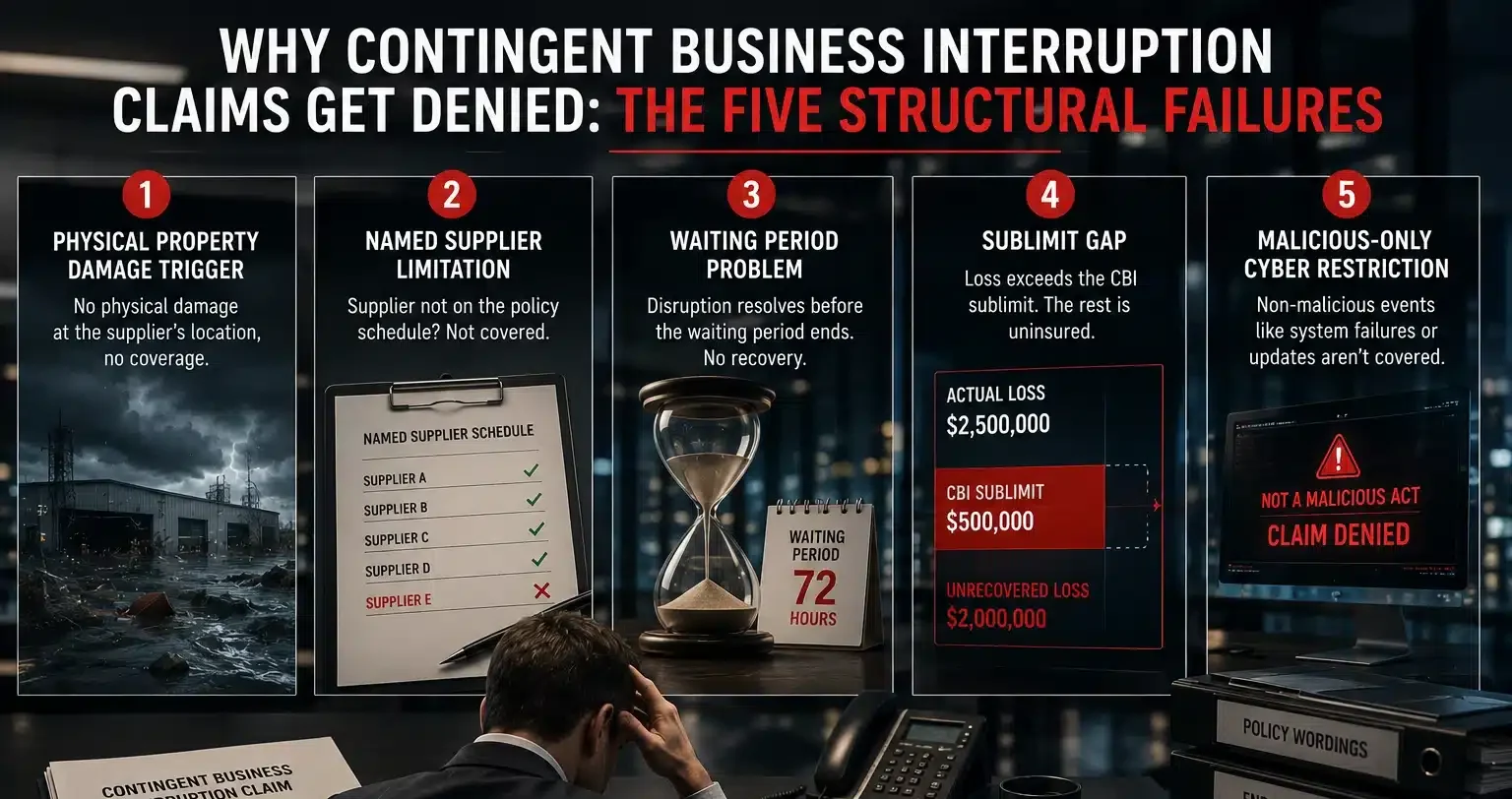

Why Contingent Business Interruption Claims Get Denied: The Five Structural Failures

Most CBI claims fail not because the endorsement is missing but because the trigger conditions, supplier schedules, sublimits, and cyber provisions were never structured to match the actual loss scenario. Five specific policy design failures account for the vast majority of denied contingent business interruption claims, and most mid-market companies carry at least three of them without knowing it.

1. The Physical Property Damage Trigger

Most traditional CBI policies require physical property damage at the supplier’s location before coverage activates. A factory fire halting production: the policy responds. A ransomware attack encrypting a supplier’s systems and shutting down operations: most policies do not respond. A critical vendor pushing a faulty software update that takes their platform offline: no physical damage, no coverage.

This single exclusion is why thousands of businesses recovered nothing after the CrowdStrike event. The outage was caused by a faulty software update, not a fire or flood. Physical damage triggers eliminate coverage regardless of the size of actual losses.

2. The Named Supplier Limitation

Some CBI policies only cover disruptions affecting suppliers listed by name on the policy schedule. Any supplier not on the schedule is not covered. If your supplier network changes during the year and the policy is not updated, new suppliers are exposed. If a disruption occurs two tiers back in your supply chain at a vendor your primary supplier depends on, named-only coverage almost certainly does not respond. Mid-market companies with actively evolving supplier networks are especially exposed to this gap. It is rarely discussed at renewal.

3. The Waiting Period Problem

Most CBI provisions include a waiting period, typically 24 to 72 hours, before coverage activates. Disruptions that resolve before the waiting period ends produce zero recoverable losses under the policy. For just-in-time manufacturers or distributors, a 36-hour outage at a critical supplier can shut down a production line and cost six figures while the insurance policy sits dormant.

4. The Sublimit Gap

A company carrying $10 million in BI coverage may discover their CBI sublimit is $500,000. When a real supply chain loss exceeds that cap, the difference is unrecovered and uninsured. Most policyholders do not know their CBI sublimit until they file a claim and see the cap applied.

5. The Malicious-Only Cyber Restriction

Some cyber insurance policies include business interruption or contingent BI language but restrict coverage to losses from malicious cyberattacks only. A negligent software update, a system failure, or an accidental platform outage does not meet the malicious trigger. The CrowdStrike incident was caused by a faulty software update, not a malicious attack. Businesses with malicious-only cyber BI provisions received nothing from their cyber carrier for those losses.

Real-World Example: CDK Global, June 2024

In June 2024, CDK Global, the automotive software platform used by approximately 15,000 dealerships across North America, suffered a ransomware attack that took the platform offline for nearly two weeks. Dealerships reverted to manual processes. Sales slowed. Service departments shut down. Collective losses were estimated at $1 billion.

For many dealerships, the claim outcome depended entirely on whether their policy required physical damage at a listed supplier location, whether their cyber form covered malicious events at a third-party vendor, and whether their CBI sublimit was sized to the actual exposure. Dealerships without the right language received nothing. The losses were real. The coverage gaps were structural, undetected at policy inception, and almost never reviewed at renewal.

Wondering if your current policy has any of these structural gaps? Contact our team for a no-obligation policy review.

Named vs. Unnamed Suppliers: The Policy Structure That Determines Whether You Collect

Named supplier CBI coverage only responds when the disruption hits a supplier specifically listed in your policy schedule. Blanket or unnamed coverage extends to any qualifying dependent third party without requiring a maintained schedule. For mid-market companies with evolving supplier networks, named-only coverage is one of the most common undetected gaps in any commercial program.

How named-only coverage fails in practice:

Structure |

How It Triggers |

Primary Risk |

|---|---|---|

|

Named or Scheduled Only |

Covers only suppliers listed by name and location |

Any unlisted or new supplier produces no recovery |

|

Blanket or Unnamed |

Covers any qualifying dependent third party |

Typically carries lower per-location sublimits |

|

Hybrid (Named + Blanket) |

Higher limits for scheduled suppliers, sublimit for all others |

Balances coverage breadth with cost for complex supply chains |

Business interruption insurance for manufacturers often requires a hybrid structure because supplier networks span multiple tiers and change frequently. Reviewing your industry risk profile is the starting point for structuring contingent business interruption insurance correctly.

Does the Physical Damage Requirement Still Apply to Cyber and Technology Outages?

Traditional CBI coverage was designed around physical events: fires, floods, and equipment damage. Today, a ransomware attack on a logistics platform, a cloud provider outage, or a faulty software update can halt operations as completely as a factory fire, but most traditional CBI forms were never built to respond to technology-driven disruptions because no physical property was damaged.

How the physical damage trigger eliminates coverage for modern outages:

Specific cyber insurance endorsements exist that remove or modify the physical damage requirement for technology-driven supply chain disruptions. These are not standard; they must be deliberately structured into the policy. According to Munich Re’s analysis of contingent business interruption and cyber events, technology-driven supply chain interruptions now represent one of the fastest-growing uninsured exposure categories.

Many companies believe their cyber policy handles this risk. In most cases, a cyber form covers the insured’s own systems only; it does not extend to outages originating at a supplier’s location.

Questions to Raise with Your Broker to Identify This Gap

How Much CBI Coverage Is Enough? The Sublimit Problem Nobody Reviews at Renewal

CBI coverage sits behind its own sublimit, separate from and significantly lower than the main business interruption limit. A company carrying $10 million in BI coverage may have a $500,000 CBI sublimit. When a real supply chain loss exceeds that cap, the unrecovered difference comes out of operating capital. Most policyholders do not learn the size of their CBI sublimit until the claim is filed and the cap is applied.

A simple framework for testing whether your sublimit is adequate:

The World Economic Forum has noted that recovery from a significant supply chain disruption can take two to three years. Even a conservative six-month estimate for a single-source component supplier often produces a loss figure that far exceeds standard CBI sublimits on most mid-market programs.

A practical benchmark for companies with concentrated supplier exposure is three to six months of gross profit attributable to the top supply chain dependencies. Most standard CBI structures fall short of this threshold without deliberate adjustment at renewal. See how your full commercial coverage program addresses supply chain business interruption exposure.

A 30-minute review could be the difference between a paid claim and a seven-figure gap. Book a call with The Coyle Group.

What Does Contingent Business Interruption Insurance Cost?

CBI coverage does not have a standard price because the premium is driven by the specific structure of the endorsement, not by a flat rate. The coverage adds cost to a commercial property policy, but the premium is modest relative to the exposure it addresses. Most mid-market companies are surprised to learn it is negotiable at renewal rather than fixed.

The six main factors that drive CBI premium:

The correct question is not “how much does CBI cost?” but “what is the right structure, and what does that structure cost?” Those are two different conversations, and most generalist brokers only have the second one.

What Mid-Market CFOs and Risk Managers Should Do Before the Next Renewal

Every structural CBI gap described above is fixable before a loss event, and most corrections can be negotiated at renewal through endorsements and schedule adjustments. They are nearly impossible to retrofit after a claim is filed. The six steps below give risk managers and CFOs a prioritized sequence for closing the most common failures before the next disruption turns them into a denial.

Most of the supply chain business interruption coverage gaps that produce denied claims were visible at policy inception. The businesses that find them before a loss event pay a premium adjustment at renewal. The ones that find them during a claim pay the full uninsured loss.

What a Generalist Broker Typically Misses on CBI

Most commercial property policies include a CBI endorsement as a default add-on.

What a generalist broker often does not catch: whether the endorsement language contains a physical damage trigger that silently excludes technology-driven outages; whether the sublimit was set by a carrier default rather than a supplier dependency analysis; whether the policy’s definition of “direct supplier” stops at tier-one and leaves upstream exposure uncovered; and which markets offer blanket coverage language versus named-only defaults.

These are carrier-specific placement decisions that require knowledge of which insurers offer the broadest language.

Reach out to our team at The Coyle Group to schedule a structured CBI review before your next renewal cycle.

Questions about Contingent Business Interruption Insurance?

Get the Right Coverage for Your Supply Chain

Most contingent business interruption coverage gaps are invisible until a loss event turns them into a denied claim. The structure of the trigger, the supplier schedule, the sublimit, and the cyber provisions all determine whether a claim succeeds or fails, and most mid-market companies have never had those four points reviewed together.

The Coyle Group has spent over 40 years reviewing commercial insurance programs for mid-market and enterprise companies. Our CBI reviews are structured around the five failure scenarios documented on this page, not a general policy summary. We identify the specific gaps, identify the markets that offer the broadest language, and structure the endorsements before renewal, not after a loss.

Book a 30-minute CBI coverage review. No obligation. No generic pitch. A structured review of whether your current program would actually pay if a key supplier went offline tomorrow.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?