How to Switch Insurance Brokers Without Disrupting Your Coverage

What the Transition Actually Looks Like and Why It Is Not as Complicated as You Think

Most business owners who are unhappy with their insurance broker stay longer than they should. They do not stay because they think the relationship will improve. They stay because the idea of switching feels uncertain.

Owners have posted it online in almost the same words: “How do I fire my commercial liability broker without interrupting coverage?“ The devil you know feels safer than the one you do not.

That hesitation is understandable, but it is usually misplaced. Switching insurance brokers is a defined process with clear steps, and when it is handled correctly, there is no disruption to your coverage.

The transition is far less dramatic than most people expect.

What follows is a straightforward walkthrough of how the switch actually works, what to expect from your old broker, and what to watch for along the way. Whether you are trying to switch commercial insurance brokers at renewal or change insurance brokers mid-policy, the core mechanics are the same.

If you are already sure your broker has stopped fitting your business, you are not alone and you are not stuck.

Most owners tell us the same thing: slow certificates, no proactive coverage review, no industry knowledge. This guide shows the exact transition process we use for mid-market accounts so the switch is handled cleanly. Book a short call if you want a private conversation about your specific situation.

What It Actually Costs to Stay With the Wrong Broker

Staying with a broker who is not keeping up does not just cost you service. It costs you coverage accuracy, contract opportunities, and recovery after a loss. The real price of inaction shows up quietly, and you rarely notice it until a claim or a contract is on the line.

Here is what the data says about the cost of a mismanaged program:

When to Make the Move

The cleanest switch happens at renewal. Your existing policies are naturally expiring and being replaced, the new broker markets the account, places the coverage, and the old policies simply do not renew. There is no overlap, no cancellation, and no penalty.

That said, there are moments when waiting for renewal is the wrong answer, and the timing table below lays out when each path makes sense.

Renewal vs. mid-term switch:

Timing |

When it makes sense |

What to watch for |

|---|---|---|

|

At renewal (preferred) |

Service is bad but not catastrophic; you have 60 to 120 days of runway |

Start conversations early so the new broker has time to market |

|

Mid-term |

Service breakdown is actively costing money (delayed certificates, missed endorsements, unresponsive account management) |

Short-rate cancellation penalty may apply; new broker explains the off-cycle change to underwriters |

If you cancel policies before the renewal date, you may be subject to a short-rate cancellation penalty, which means the outgoing carrier keeps a larger portion of the premium than a pro-rata refund would provide. In some situations, that penalty is worth taking, particularly if the service breakdown is costing you money. In most cases, timing the switch to renewal avoids this entirely.

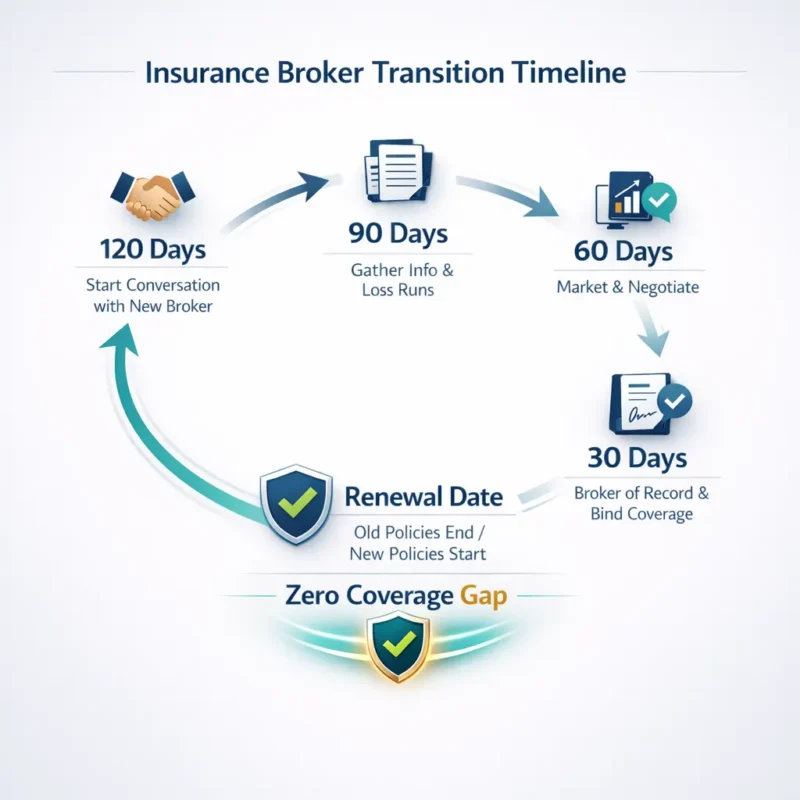

The ideal broker-switch timeline looks like this:

When things are rushed, details get missed. When there is enough lead time, the process is methodical and thorough.

Mid-term switches are possible, and we have done them, but they require explaining to underwriters why the change is happening outside the normal cycle. Most underwriters are not eager to look at a deal mid-term because they assume it is a shopping exercise.

When we do a mid-term change, we explain the circumstances clearly, and in most cases, the underwriters understand.

What Happens Before the Switch

Before any transition takes place, the new broker has already done the heavy lifting. The decision to switch is based on the complete picture, not a promise.

By the time you say “let us do it,” your new broker should already have:

This pre-work phase is also when the new broker should be identifying issues your current program may have missed. The most common findings we see:

A good broker does not just replicate what you already have. They use the transition as an opportunity to get the program right. This is the same diagnostic approach we explain in our Diagnostic Insurance Review process, where we review the policy as a whole rather than line by line.

One thing we are always clear about from the beginning: this is not a shopping exercise. We are not trying to win the account by undercutting the price.

If correcting undervaluation or closing coverage gaps means the premium goes up, we will tell you that upfront and explain why. The goal of the transition is to get the program to where it should be, not to make the numbers look good on day one and deal with the consequences later.

If you want to understand why this matters, why shopping your business insurance around is ineffective covers the long version.

What Happens After You Say Yes

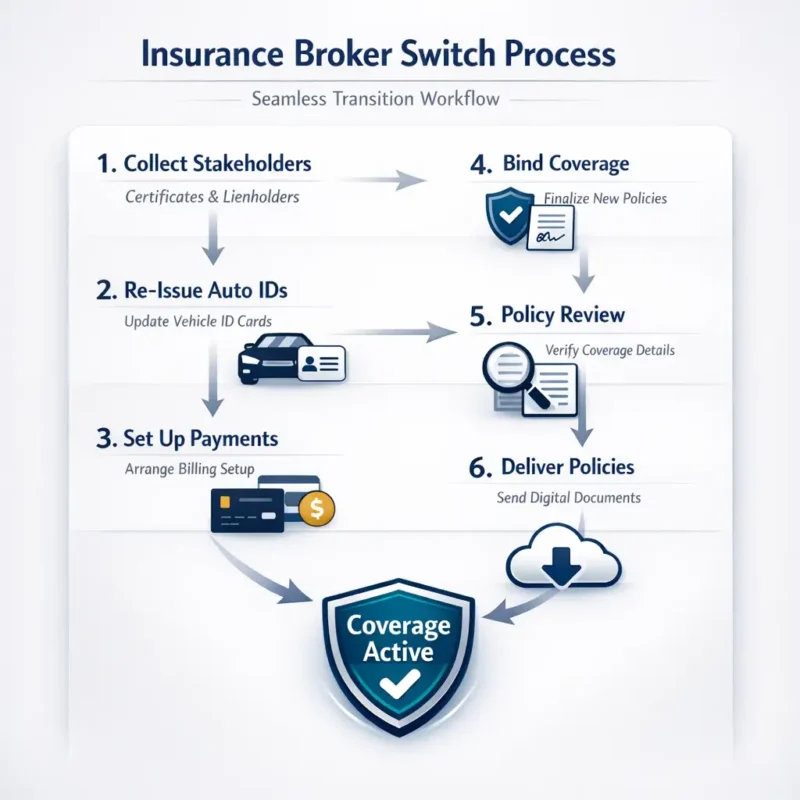

Once the decision is made, the execution is a series of defined steps. None of them are complicated, but all of them need to happen in the right order and on the right timeline.

Step-by-step execution:

A missed certificate can hold up a contract or create a compliance issue, which is why the certificate holder and lien holder list is always step one. For lenders, they need evidence of property insurance naming them as the loss payee. This is administrative work, but it is critical.

The financial mechanics are not complicated, but they need to be handled cleanly so there is no gap between the old coverage expiring and the new coverage taking effect.

What a Broker of Record Letter Actually Does

A Broker of Record (BOR) letter is a short document on your company letterhead that tells the insurance carrier to recognize your new broker as the authorized representative for your policies. It transfers servicing rights without changing the policy itself, which is how business owners switch an insurance broker without losing coverage or altering the policy terms.

Three things to know about a BOR letter:

Our full explainer on broker of record letters covers the legal language, who signs, and how it is submitted. If you are reading about BOR letters for the first time, it is almost always because your new broker is handling it for you, not because you need to draft one yourself.

Getting to Know Your New Team

A transition is not just about paperwork. It is about building a new working relationship, and that starts before the ink is dry on the binders.

For larger accounts, the loss control inspection is an opportunity to demonstrate that the business takes risk management seriously, and in some cases, it surfaces recommendations that can actually reduce your exposure and your costs over time. This is the kind of proactive service that your broker should already be doing at every renewal, and if they are not, that alone is a reason to consider a change.

What to Expect from Your Old Broker

This is the part most clients are anxious about, and it is worth being direct.

Your old broker is going to lose commission income when you leave. On a mid-market account, that could be $20,000, $50,000, or well over $100,000 in annual commissions.

They are not going to be happy about it, and that is understandable. But you need to be prepared for how that unhappiness may express itself.

What usually happens:

A simple script that ends the conversation cleanly:

“We made a decision. We appreciate the relationship we had, and if you have questions or concerns, here is my new broker’s contact information.”

That is it. You are not obligated to justify your decision, negotiate, or absorb someone else’s frustration.

Most broker transitions are professional. But it is better to be prepared for the difficult version than to be caught off guard by it.

We coach every client through this conversation because we have seen every version of it. The key is to be grateful for the relationship that existed, firm about the decision that has been made, and brief.

Do not get drawn into a long discussion about what went wrong or what could have been done differently. Is switching insurance agents difficult? explains the full social dynamic of how this conversation typically goes.

If you are anxious about that conversation, book a call and we will walk you through exactly what to say.

What Can Go Wrong and How to Prevent It

The most common pitfall in a broker transition is running out of time. This happens for different reasons:

This is why the 120-day lead time matters. When there is enough runway, these delays are manageable. When you are backed up against the renewal date, every delay becomes a crisis.

If your current broker is dragging their feet on loss runs, our guide to insurance loss runs explains what you are entitled to and how to request them formally.

The other area where things can get complicated is the underwriting process itself. For larger accounts, insurance carriers often send a loss control inspector to evaluate the premises before finalizing a quote.

If that inspection turns up issues (safety deficiencies, missing equipment, inadequate fire protection), it can slow things down or change the terms of the quote.

What this looks like in practice

A mid-sized distributor in the Northeast came to us six weeks before renewal. Their existing broker had never ordered a property appraisal, and the building was insured for roughly 60% of its replacement cost. The old broker had missed it for three renewal cycles. During the switch, we identified the shortfall, ordered a proper valuation, and corrected the limit before bind.

The premium went up modestly, but the client went from being exposed on roughly $4 million of property value to being properly covered. That kind of correction is the whole point of doing the transition right.

We approach loss control positively. Some clients see it as a hassle, and we understand that.

Risk control exists to prevent claims, and preventing a claim is always cheaper than paying one, not just for the insurance company but more so for the client.

Every claim carries uninsured costs: downtime, wasted materials, overtime, retraining, and administrative time. The total cost of a loss is almost always several times what the insurance company pays.

So, when a loss control inspection surfaces something that needs to be addressed, that is actually working in the client’s favor.

After the deal is signed and the policies are bound, there is generally very little that falls through the cracks. Occasionally, a client will assure us that a risk management issue has been resolved when it has not, and we have to go back to the underwriter to negotiate.

That is an inconvenience, but it is manageable. The real pitfalls are all in the pre-binding phase, which is why preparation and lead time are everything.

The First 90 Days After the Switch

Once the transition is complete, the first 90 days are about confirming that everything is in place and building the working relationship.

90-day checklist:

This is also the period when we identify any issues or improvements that were not part of the initial transition but should be addressed. Maybe there is a coverage gap that needs to be closed at the next renewal. Maybe there is a risk management issue that should be on the calendar.

The first 90 days set the tone for the relationship going forward, and we treat them accordingly. If you want to see what a proper mid-year check-in looks like, this is what a coverage review covers.

Frequently Asked Questions About Switching Insurance Brokers

Ready to Make the Move?

If you have been thinking about switching brokers but have been putting it off because the process feels uncertain, consider this: the process is defined, the steps are clear, and the right broker will handle the coordination for you.

Your job is to make the decision. Our job is to make the transition seamless.

Start with a conversation to talk about your situation. We will walk you through exactly what the transition looks like for your specific account, with no obligation and no pressure.

If you want to read more before reaching out, we have written guides on signs your broker has outgrown you, what your insurance broker should be doing at renewal, and how to choose a top commercial insurance broker.

Each of those explains a different part of the relationship you should expect from the broker who replaces the one you are leaving.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

Third Party Employment Practices Liability Insurance. Protect Your Business

Are You Overpaying or Underinsured on Your Business Insurance?

Liberty Mutual Business Insurance Quotes