The CrowdStrike Outage: Will Cyber Insurance Cover It?

On July 19, 2024, a single line of code in a CrowdStrike software update crashed millions of Windows systems worldwide. Airlines grounded flights. Hospitals postponed procedures. Banks halted transactions. The Blue Screen of Death appeared on computer monitors from Fortune 500 headquarters to small business offices.

The question every business owner asked: Will my cyber insurance policy respond to this event?

The answer depends entirely on your specific policy language, and that’s exactly the problem most businesses discover too late.

TLDR: Key Takeaways

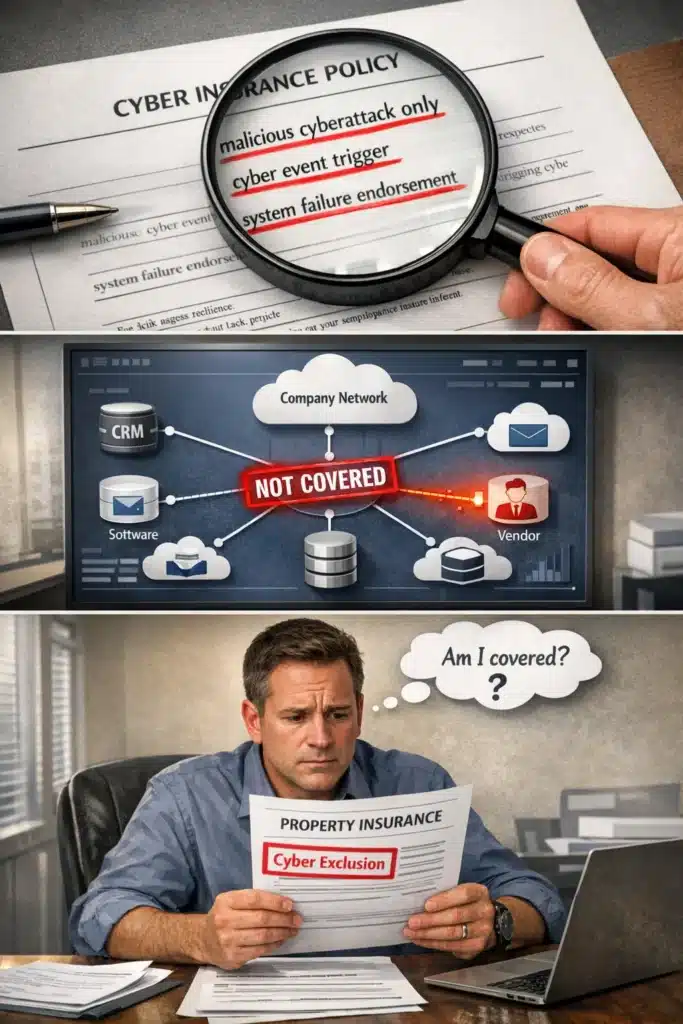

What 40+ Years Taught Me About System Failure Claims

In four decades of handling cyber insurance claims, I’ve learned that the difference between “covered” and “denied” often comes down to three words buried in policy definitions. Business owners assume their cyber policy protects against all technology failures. It doesn’t.

The CrowdStrike incident perfectly illustrates why policy language matters more than premium cost when selecting cyber insurance coverage.

Understanding the CrowdStrike Event

What Happened

According to Microsoft estimates, approximately 8.5 million Windows devices were impacted globally when CrowdStrike released a defective software update at 04:09 UTC on July 19, 2024.

Affected industries:

What’s the Difference Between System Failure and Security Failure Coverage?

This was NOT a malicious cyberattack, it was a system failure caused by human error in code deployment. That distinction determines whether your policy responds.

Coverage Type |

CrowdStrike Event Classification |

Typical Policy Response |

|---|---|---|

|

Security Failure |

❌ Not applicable (no malicious actor) |

Would be covered |

|

System Failure |

✅ Applies (software deployment error) |

Coverage depends on endorsement |

|

Act of War/Terrorism |

❌ Not applicable |

Would be excluded |

Many cyber policies restrict business interruption coverage to “security failures” only, explicitly excluding system failures caused by:

Is the CrowdStrike Outage Covered by Cyber Insurance?

What Types of Coverage May Pay for CrowdStrike Losses?

According to insurance industry analysis, these coverage sections are most likely to respond:

1. What Does Business Interruption Coverage Pay For?

What it covers:

Example calculation:

2. What Are Extra Expenses in Cyber Insurance?

What it covers:

These costs help minimize business interruption losses and get operations back online faster.

3. Does Cyber Insurance Cover Vendor Outages Like CrowdStrike?

Yes, but only with dependent business interruption coverage:

According to Coalition Insurance data, over 30% of breaches now involve third-party elements. Standard business interruption typically covers only YOUR network failures. Dependent business interruption extends protection to:

Without this endorsement, the CrowdStrike event may not trigger coverage since it originated from an external vendor’s update.

How Do Time Deductibles Work in Cyber Insurance?

Most business owners don’t realize cyber policies use time-based deductibles rather than dollar deductibles for business interruption claims.

Common Time Deductibles

Deductible Period |

Coverage Activation |

Best For |

|---|---|---|

|

8 hours |

After 8 hours of downtime |

Larger businesses with significant daily revenue |

|

12 hours |

After 12 hours of downtime |

Mid-market companies |

|

24 hours |

After 24 hours of downtime |

Small businesses with lower revenue concentration |

Critical consideration: If CrowdStrike systems were restored within your deductible period, you receive NO reimbursement, even if losses were substantial.

Real-World Scenario

A distribution company experienced 18 hours of downtime from the CrowdStrike outage:

Larger organizations may also face dollar deductibles in addition to time-based deductibles, creating a second threshold before coverage activates.

Critical Policy Exclusions and Limitations

1. Does Cyber Insurance Only Cover Malicious Attacks?

Some policies explicitly limit coverage to losses caused by malicious cyberattacks. According to industry reporting, the CrowdStrike outage would not qualify under these restricted policies.

Policy language to review:

2. Third-Party Vendor Exclusions

Standard first-party cyber coverage may exclude losses originating from:

3. Will My Property Insurance Cover the CrowdStrike Outage?

If you don’t have cyber insurance, could your property policy respond?

Unlikely, but worth investigating. Most property insurance policies now include cyber exclusions, but some older policies contain “silent cyber” coverage, meaning cyber events aren’t explicitly excluded.

Your broker should review:

What Should I Do If My Business Was Affected by the CrowdStrike Outage?

Step 1: Document the Time Deductible

Review your policy immediately:

Step 2: Calculate Potential Losses

Business interruption:

Extra expenses:

Step 3: Notify Your Insurer Immediately

According to cyber insurance claims data, failure to report potential claims promptly is the #1 reason for denial.

Notification requirements typically mandate reporting within:

Even if you’re unsure whether losses exceed your deductible, put your insurer on notice. You can always withdraw the claim if losses don’t materialize.

Step 4: Preserve Evidence and Documentation

Critical documentation includes:

What Can Businesses Learn From the CrowdStrike Event?

1. Policy Language Matters More Than Price

The global cyber insurance market is projected to reach $29 billion by 2027, but not all policies are created equal.

Two businesses paying similar premiums can have dramatically different coverage based on:

2. Vendor Risk Requires Specific Coverage

Over 30% of cyber incidents now involve third-party elements. The CrowdStrike event demonstrates why dependent business interruption coverage isn’t optional, it’s essential.

Assess your vendor dependencies:

3. Time Deductibles Create Hidden Exposure

Unlike dollar deductibles on property policies, time deductibles mean you absorb 100% of losses during the waiting period. For the CrowdStrike event:

Understanding what cyber insurance actually covers helps you evaluate whether your time deductible aligns with recovery capabilities.

4. Silent Cyber is Disappearing

Property insurers have systematically eliminated silent cyber coverage over the past five years. If your property policy doesn’t explicitly exclude cyber events, you have an increasingly rare policy that may respond, but don’t count on it at renewal.

How Will CrowdStrike Change the Cyber Insurance Market?

How Will the CrowdStrike Outage Affect Cyber Insurance Policies?

According to Aon’s analysis, the CrowdStrike event is prompting insurers to:

Expected changes at renewal:

Industry-Specific Considerations

Different industries face unique exposures from system failures:

What Can I Do Besides Buy Cyber Insurance?

While insurance provides financial protection, the CrowdStrike event demonstrates why cyber resilience requires more than just coverage.

Critical Risk Management Practices

1. Vendor Management

2. Business Continuity Planning

3. Update Management Protocols

4. Insurance Program Design

Understanding the difference between cyber insurance versus crime insurance helps ensure comprehensive coverage for both malicious and non-malicious technology failures.

How The Coyle Group Approaches System Failure Coverage

We don’t just place cyber insurance; we architect programs that respond when you need them.

Our process:

The businesses that recovered fastest from CrowdStrike-type events had three things in common: proper dependent business interruption coverage, documented recovery procedures, and immediate insurer notification.

Frequently Asked Questions

Don’t Wait for the Next System Failure

The CrowdStrike event isn’t an anomaly, it’s a preview of our increasingly interconnected technology environment. Software updates, cloud provider outages, and vendor system failures will continue disrupting businesses. The question isn’t whether another event will occur, but whether your insurance program will respond when it does.

If you’re uncertain about your coverage:

Why Work with The Coyle Group

The businesses that emerged from the CrowdStrike event financially protected had proper coverage in place beforehand. Waiting until after an incident to discover coverage gaps is costly and stressful.

To verify your program responds to both malicious attacks and system failures.

Author’s Expertise

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping businesses develop comprehensive cyber insurance programs that protect against both malicious cyberattacks and non-malicious system failures, ensuring coverage responds when needed most.