Cyber Insurance Renewal

More Than Rubber-Stamping Last Year’s Policy

Cyber Insurance Renewal: 6 Costly Mistakes Business Owners Make

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

Cyber insurance renewal is the annual process of reassessing your policy limits, coverage terms, and carrier requirements before your policy expires, not simply signing off on the same coverage as the previous year.

Your cyber insurance renewal notice arrives. The premium looks similar to last year, the coverage seems familiar, and the renewal period is ticking down. So you sign off and move on to the next thing.

In short, treating cyber insurance renewal as routine invites gaps; treating it as a review improves fit and value.

However, here’s what most SMBs (Small-Medium Sized Businesses) often overlook: your cyber insurance renewal is a critical opportunity to reassess whether your coverage still aligns with your actual risk profile.

Your business has changed since last year. Your threat landscape has evolved. And your coverage gaps may have widened without you realizing it.

TL;DR

Your cyber insurance renewal demands strategic attention:

Investment range:

$1,000–$7,500 annually for most SMBs, depending on revenue, industry risk, and security posture. Therefore, plan budget ranges before your cyber insurance renewal meeting.

Assess Your Cyber Coverage

What Cyber Insurance Renewal Should Actually Be

When your cyber insurance policy comes up for renewal, you’re facing a choice: continue with what you have, or take the opportunity to reassess. True cyber insurance renewal isn’t just about renewing a policy; it’s about actively auditing whether your policy still protects your business against your current risks.

This is the distinction that separates SMBs that manage cyber risk strategically from those that make passive decisions about renewal. One group uses renewal as a checkpoint. The other group simply extends what they already have.

At The Coyle Group, we frequently observe this difference in our clients. When SMBs approach renewal thoughtfully, they often discover coverage gaps, better pricing options, or carrier changes they weren’t aware of. When they don’t, they end up renewing policies that no longer fit their business.

What 40+ Years Taught Me About This Risk

From my experience after four decades helping businesses navigate insurance challenges, I’ve seen the same cyber insurance renewal mistake countless times: business owners who assume “no news is good news” when their renewal arrives. They sign the documents, file them away, and move on, completely unaware they’re underinsured until a claim happens.

The businesses that avoid this trap treat renewal as an annual health check for their cyber protection. They ask questions. They reassess. They negotiate. And they consistently secure better coverage at better prices than those who auto-renew.

Why Your Business Risk Profile Has Shifted Since Last Renewal

Your risk profile changes every year, whether you notice it or not. New employees, cloud migrations, remote work expansion, and new vendors each add to the attack surface. Underwriters see this, and reprice accordingly. What qualified for favorable rates last year may not this year. Since last year’s renewal, your business has likely evolved in ways that affect your cyber risk profile:

Operational Changes:

Threat Evolution:

Regulatory Changes:

Carrier Market Shifts:

Bottom line

Renewal is your moment to verify your policy still fits. Most SMBs skip this step and discover gaps only after filing a claim.

The $1M Limit Reality: Why Most SMBs Are Dangerously Underinsured

A $1 million cyber policy sounds like real coverage until you look at what a mid-sized breach actually costs. For most SMBs, forensic investigation, legal defense, notification, and business interruption alone routinely exceed $1 million before a ransom payment is even considered.

Here’s a statistic that should raise red flags during your cyber insurance renewal: Policy limits typically range from $1 million to $5 million, with most companies starting with policies of $1 million.

That sounds like substantial coverage until you examine the actual costs of a cyber incident.

True Cost of a Data Breach

Small businesses can expect to pay $120,000 to $1.24 million in 2025 to respond and resolve a security incident. A cyber attack costs an SMB $254,445 on average, with some attacks costing up to $7 million.

Breaking down breach expenses:

Secure Better Coverage

Hidden Risks of Passive Renewal: What You’re Missing

Auto-renewing without a review exposes you to five risks that won’t show up in your premium notice, but will show up in a denied claim. Here’s what passive renewal actually costs.

1. Coverage Drift

Your operations evolved, but your policy didn’t. Cloud systems, e-commerce, and new vendors. each creates exposure that your old policy may not address. Carriers now expect robust third-party risk management with documented vendor cybersecurity requirements.

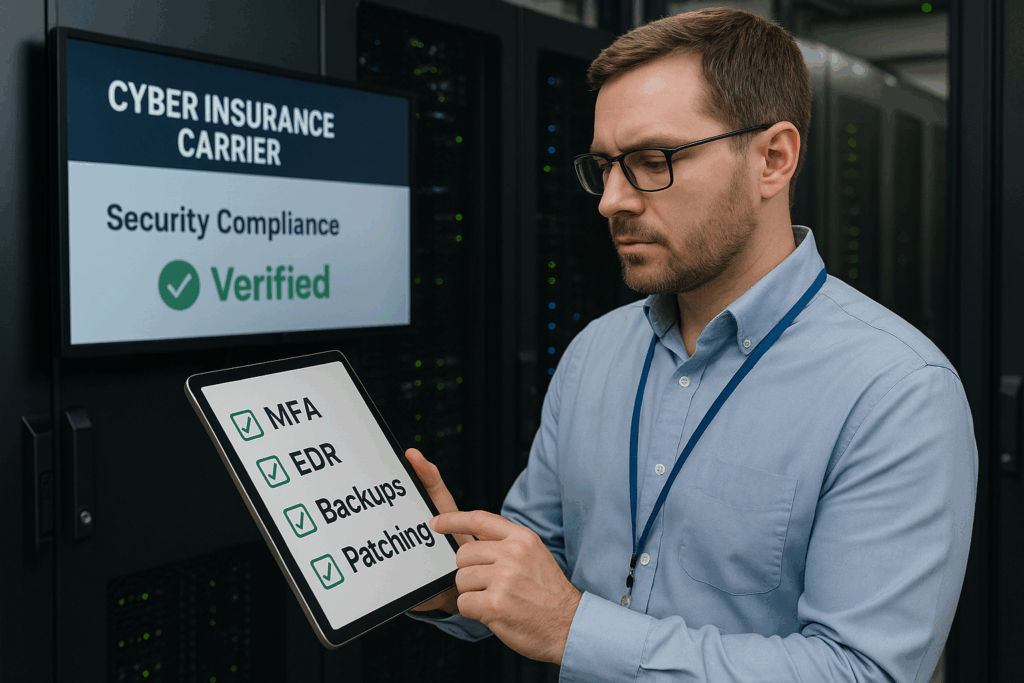

2. Missing Mandatory Security Controls

3. Missed Savings Opportunities

Nearly two-thirds of businesses realized cost savings in 2024 by having their brokers shop their renewals properly. Premiums moderated and flattened in many sectors, but only for those who negotiated.

4. Compliance Gaps

New privacy laws may require coverage elements your policy doesn’t include. Privacy violations are now a top concern for underwriters. Renewing without reviewing = potential regulatory exposure.

5. Carrier Appetite Changes

Your insurer might have exited your industry vertical. Non-renewal notices often arrive with 30-60 days’ warning, not enough time to find quality replacement coverage. Due to increased targeting by ransomware groups.

What Gets a Renewal Declined or Restricted

Carriers decline or restrict renewals for six specific reasons: no MFA on email or VPN, no EDR on endpoints, unverified or undocumented backups, claims frequency in the prior 3-5 years, operating systems past end-of-life (Windows 10 EOL: October 2025), and revenue growth that wasn’t disclosed at last renewal. Any one of these can result in a non-renewal notice with 30-60 days’ warning.

How The Coyle Group Approaches Strategic Cyber Insurance Renewal

We don’t process renewals; we reassess them. When clients approach renewal, we audit current coverage against actual operations, review business changes, and verify coverage limits match realistic breach scenarios.

Our Process:

Why it matters:

We help you avoid the $1M trap. If you’re underinsured, we show you what adequate coverage looks like before you need it. Understanding the difference is crucial for evaluating whether your policy effectively protects your business, and knowing what cyber insurance actually covers prevents surprises when filing a claim.

When to Start Your Cyber Insurance Renewal Process

The Golden Rule:

Start 30-90 days before expiration. Companies waiting until the last minute often face non-renewal crises with inadequate time to find alternatives.

Critical:

Most policies renew in Q4. Waiting until September means scrambling when underwriters are swamped.

Understanding the Cyber Insurance Market

Market Outlook:

Stable rates (-5% to +5% forecast) with plentiful capacity, but only for businesses with strong security controls. The , up from $16.3 billion in 2025, but access to favorable coverage increasingly depends on demonstrating comprehensive cybersecurity measures.

Key Trends:

What This Means:

Market conditions favor prepared businesses. Strong security posture unlocks competitive pricing. Neglecting controls creates renewal challenges, or outright non-renewals.

Admitted vs. Surplus Lines

Most cyber policies are written on non-admitted (surplus lines) paper, meaning the carrier isn’t licensed by your state and the policy isn’t backed by your state’s guaranty fund. This is standard for cyber; don’t be alarmed, but it means policy language varies more than in admitted markets, and you have fewer regulatory protections if the carrier becomes insolvent. When shopping at renewal, your broker should be able to tell you whether each quote is admitted or surplus lines paper.

Real-World Renewal Scenario

The $3M Surprise

What Underwriters Actually Ask at Cyber Insurance Renewal

Question Underwriters Ask |

What They’re Looking For |

|---|---|

|

Do you have MFA on all email and remote access? |

Full deployment, not partial |

|

Do you use EDR/MDR on all endpoints? |

Active monitoring, documented |

|

Are backups immutable, offsite, and tested? |

Restoration test logs required |

|

Have you had any claims or incidents in the past 3 years? |

Frequency and severity of losses |

|

Do you have a documented incident response plan? |

Tested within the last 12 months |

|

What is your patch management SLA for critical vulnerabilities? |

14-30 days standard expectation |

|

Do you have third-party vendor security requirements? |

Written contracts required |

Don’t Auto-Renew Blindly

Questions about Cyber Insurance Renewal?

Taking Control of Your Cyber Insurance Renewal

Your cyber insurance renewal is too important to treat as routine paperwork. Strategic reassessment saves money, closes gaps, and provides genuine protection.

Why Work with The Coyle Group:

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the United States, helping them solve their insurance challenges. Gordon specializes in helping SMBs develop comprehensive cyber insurance programs that protect their operations and support their growth objectives.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Tech E&O vs. Cyber Insurance: What You Need to Know

First Party vs Third Party Cyber Insurance: What’s Covered, What’s Missing, and What You Actually Need