Quick Answer:

Action over liability is a New York-specific legal concept where an injured worker sues a property owner after collecting workers comp, and the property owner then tenders that lawsuit back to the contractor under the indemnity agreement in the construction contract.

If the contractor’s general liability policy excludes action over claims, the contractor is personally responsible for a multi-million dollar lawsuit with no insurance coverage.

These exclusions are common in downstate New York policies and are often disguised under different names in the policy language.

What Is Action Over Liability and Why Contractors in New York Are Uniquely Exposed

Action over liability is one of the most misunderstood coverage issues in contractor insurance, and it is one of the most financially devastating. The term describes a specific sequence of events that leads from a workers compensation claim to a multi-million dollar lawsuit landing directly on the contractor who thought they were insured.

The concept is most prevalent in New York, particularly in downstate New York and the Five Boroughs, where labor law and construction contract language create conditions that make action over claims both common and expensive. Understanding how this works before you start a project is the difference between a covered claim and a business bankruptcy.

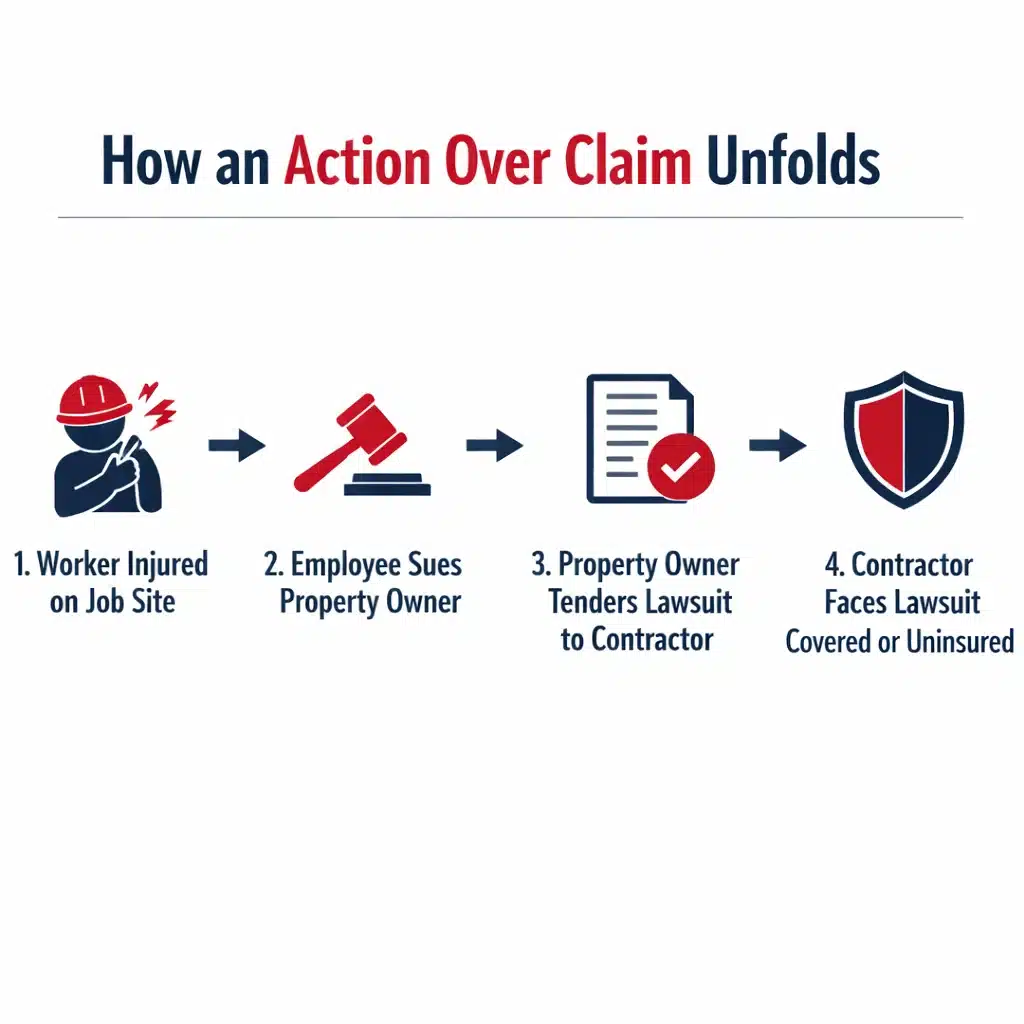

Every action over a scenario involves three parties. The first party is the contractor performing the work. The second party is the contractor’s employee who is injured on the job. The third party is the property owner or project owner who engaged the contractor.

Before construction begins, the property owner sends the contractor a construction contract. Inside that contract is an indemnity agreement, sometimes called a hold harmless agreement. The language states that the contractor promises to indemnify and hold the property owner harmless from any or all claims that may arise during construction. The owner also typically requires the contractor to name them as an additional insured on the contractor’s policies.

How does a routine injury turn into an uninsured multi-million dollar lawsuit?

An action over claim starts with a workers comp injury and follows a predictable four-step path to a general liability lawsuit. The mechanism is not a legal technicality. It is a documented sequence that plays out regularly on New York construction projects, and understanding each step is the only way to recognize when your policy may leave you exposed.

How an Action Over Claim Actually Unfolds

The sequence is predictable once you understand the mechanism. What makes it dangerous is that it starts with a routine workers’ comp claim and ends somewhere far more serious.

Why do contractors with active general liability policies end up with no coverage?

Action over exclusions are embedded in general liability policies under endorsement titles that do not mention action over at all. Contractors discover this gap after a claim is filed, not before. In downstate New York, policies competing on price frequently carry these exclusions, and brokers who win business at 30 to 50 percent below market are often winning on the back of coverage that does not exist.

The Exclusion Problem: Why Your Policy Might Not Cover This

In downstate New York, particularly in the Five Boroughs, contractor liability insurance is expensive. Contractors under cost pressure sometimes choose policies that exclude action over liability to reduce premiums.

Brokers competing on price sometimes present policies with action over exclusions without clearly disclosing what is missing, sometimes winning business at 30 to 50 percent below the correct cost.

However this happened, whether the contractor chose to exclude it to save money or a broker failed to disclose it, the financial consequence is the same: no coverage for the lawsuit.

What makes this worse is that action over exclusions are frequently disguised in policy language. They do not always say “action over claims excluded” in plain terms.

Some of the endorsement titles that actually eliminate action over coverage include:

Because these endorsements use different names than the coverage they eliminate, contractors often do not realize their policy has this gap until after a claim is filed.

Reading an endorsement titled “Amendment to employee injury exclusion” and understanding that it eliminates your coverage for a $3 million lawsuit requires specific knowledge of how these endorsements interact with the base policy form.

Most contractors do not have that knowledge. Most brokers focused on price do not volunteer it.

The Financial Consequence of an Uninsured Action Over Claim

The contractor’s options when facing an uninsured action over claim are limited. They can attempt to return the claim to the property owner, who has no obligation to accept it and whose insurer will pursue subrogation against the contractor under the contract terms. They can attempt to negotiate a settlement out of pocket, typically impossible at the dollar amounts involved. Or they absorb the full judgment.

For a painting contractor, masonry contractor, drywall installer, or any tradesperson working at height in New York City or downstate, these claims occur with regular frequency. The lawsuit amount typically reflects the severity of the injury, legal fees, and the broad exposure created by the indemnity agreement language. Multi-million dollar actions are not unusual.

A business owner who has spent decades building a contracting operation can lose everything because of one policy endorsement they were never told about. The business is not protected by the fact that the workers comp carrier handled the underlying claim. The general liability policy is a separate instrument, and if it excludes action over, it does not respond. No overlap. No fallback. No coverage.

What actually happens to a contractor who faces an action over claim without coverage?

The typical outcome is bankruptcy. This is not a worst-case scenario. For painting contractors, masonry workers, drywall installers, and tradespeople working at height in New York City, these claims occur regularly. The lawsuit amount reflects the severity of the injury, legal fees, and the broad exposure created by the indemnity language. Multi-million dollar actions are not unusual.

How to Verify Your Coverage Before the Next Project

Confirming your action over coverage requires more than a certificate of insurance and a declaration page.

The coverage lives or dies in the endorsements, and endorsements require line-by-line review with someone who understands how they interact with the base policy form.

Understanding how your complete insurance program is structured, including how general liability, workers comp, and contractual liability interact, is the foundation of adequate contractor coverage.

A thorough business insurance program review ensures these coverage layers align before a claim tests them.

Why is action over liability so much more financially significant in New York than in other states?

New York Labor Law Sections 240 and 241 impose absolute liability on property owners and general contractors for gravity-related construction injuries. When a contractor signs an indemnity agreement and then excludes action over coverage, they are potentially accepting the property owner’s full Labor Law 240 exposure without any insurance to back it up. That is why these claims regularly reach multi-million dollar figures.

What New York Labor Law Adds to the Exposure

Action over liability in New York carries additional weight because of New York Labor Law Sections 240 and 241, which impose absolute liability on property owners and general contractors for certain gravity-related injuries on construction sites.

Under Labor Law 240, if a worker is injured in a fall, the property owner and general contractor can be held strictly liable regardless of the worker’s own negligence.

This absolute liability provision is what makes action over claims in New York significantly more financially significant than in other states. Because the property owner faces strict liability under the labor law, the indemnification tender to the contractor carries the full weight of that exposure.

The contractor who signed an indemnity agreement and excluded action over liability is now potentially facing a claim that includes the property owner’s full Labor Law 240 exposure.

What 40+ Years in Contractor Insurance Has Taught Me

The contractors I have seen bankrupted by action over claims were not uninformed. They had brokers, paid premiums, and had certificates on file. What they did not have was someone willing to sit down, go through every endorsement, and say: this one eliminates your coverage for the lawsuit you are most likely to face.

The question to ask your broker is not “Am I covered?” It is “Does this policy cover third-party action over claims arising from indemnity agreements?” If they cannot answer that directly and in writing, the answer is probably no.

This is why action over coverage for contractors in New York is expensive and why the exclusion, while it reduces premium, creates an exposure no contractor can absorb. The premium savings from excluding action over coverage is predictable and modest. The cost of an uninsured action over claim is unpredictable and potentially unlimited. That trade-off is never worth making.

Frequently Asked Questions About Action Over Liability

About the Author

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.