How It Works on D&O and EPLI Insurance Applications

A warranty statement is a formal declaration in Directors & Officers (D&O) and Employment Practices Liability Insurance (EPLI), insurance applications, where you confirm you’re not aware of any facts, circumstances, or situations that could give rise to a claim.

If you sign this statement and a claim later emerges from something you knew about, even informally, your insurer can deny coverage entirely.

In my 40+ years advising business owners on management liability insurance, I’ve seen warranty statements trip up executives more than almost any other application question. The problem isn’t understanding what it asks. The problem is underestimating how broadly insurers interpret your answer.

This guide explains exactly what warranty statements require, what triggers disclosure, and how to answer without putting your coverage at risk.

What is a warranty statement in a D&O or EPLI insurance application?

A warranty statement is a formal declaration made by the applicant when applying for management or professional liability insurance.

By signing it, you are stating that:

The warranty statement is usually found:

Once signed, consequently, the warranty becomes part of the policy and is relied upon by the insurer when determining coverage.

Why do insurers require a warranty statement when applying for coverage?

Insurers use the warranty statement to avoid insuring a known loss.

In insurance terms, this is often referred to as avoiding the “burning barn.” Just as a property insurer won’t insure a building that’s already on fire, a liability insurer does not want to insure a claim that is already developing.

The warranty statement helps insurers determine whether:

As a result, this protects the insurer from taking on losses that are already in motion.

What types of policies commonly include a warranty statement?

Warranty statements are standard in:

Any policy written on a claims-made basis will almost always include a warranty statement, because prior knowledge directly affects coverage.

Understanding the policies that require warranty statements

Watch this video for a comprehensive D&O Insurance overview

What kinds of situations must be disclosed in a warranty statement?

Warranty statements are intentionally broadly worded. Therefore, they typically require disclosure of:

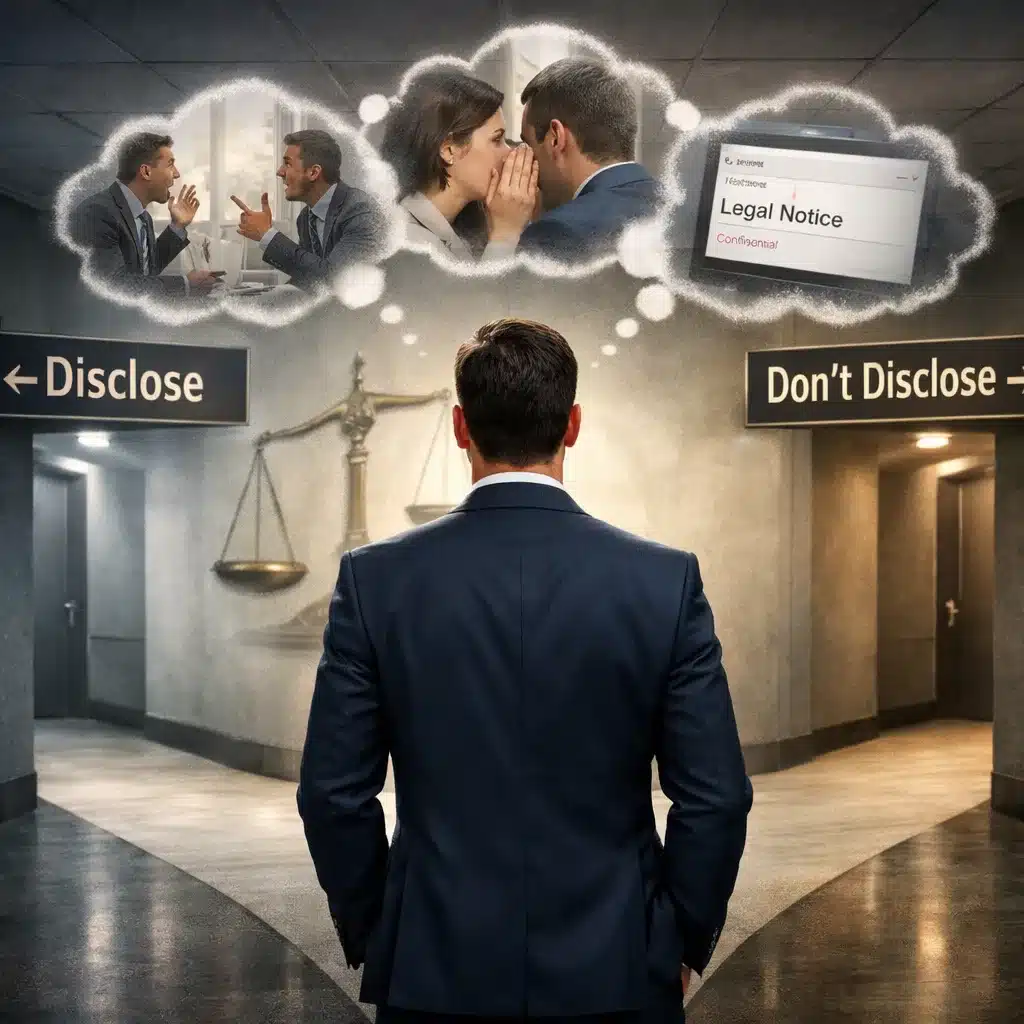

Importantly, the situation does not need to be formal, documented, or serious to require disclosure.

If it gives you pause, it likely belongs in the disclosure.

What 40+ Years Taught Me About This Risk

After four decades working with business owners on management liability insurance, I’ve seen countless coverage denials stem from warranty statement issues. The executives who thought “this will blow over” often end up personally liable when claims surface months or years later. Meanwhile, those who disclosed situations upfront typically maintain coverage for everything except the disclosed matter, which is simply excluded by endorsement.

The distinction is critical

Disclosure might mean one excluded situation, but nondisclosure can void your entire policy when you need it most.

How broadly are warranty statement questions interpreted by insurers?

Very broadly.

Insurers apply a reasonable foreseeability standard. However, the question is not:

Instead, the question is whether a reasonable person in your position could foresee a claim arising from the situation.

If the answer is yes, the insurer expects disclosure.

Subjective vs. Objective Warranty Language: What’s the Difference?

Not all warranty statements are worded the same way. Understanding whether your warranty uses subjective or objective language affects how you should answer.

Objective language is more dangerous because it can impute knowledge, if your attorney knew, courts may rule that you knew.

How do insurers word warranty statements on applications?

While wording varies, warranty statements usually follow a similar structure, such as:

Some insurers:

Different format, but the same legal effect.

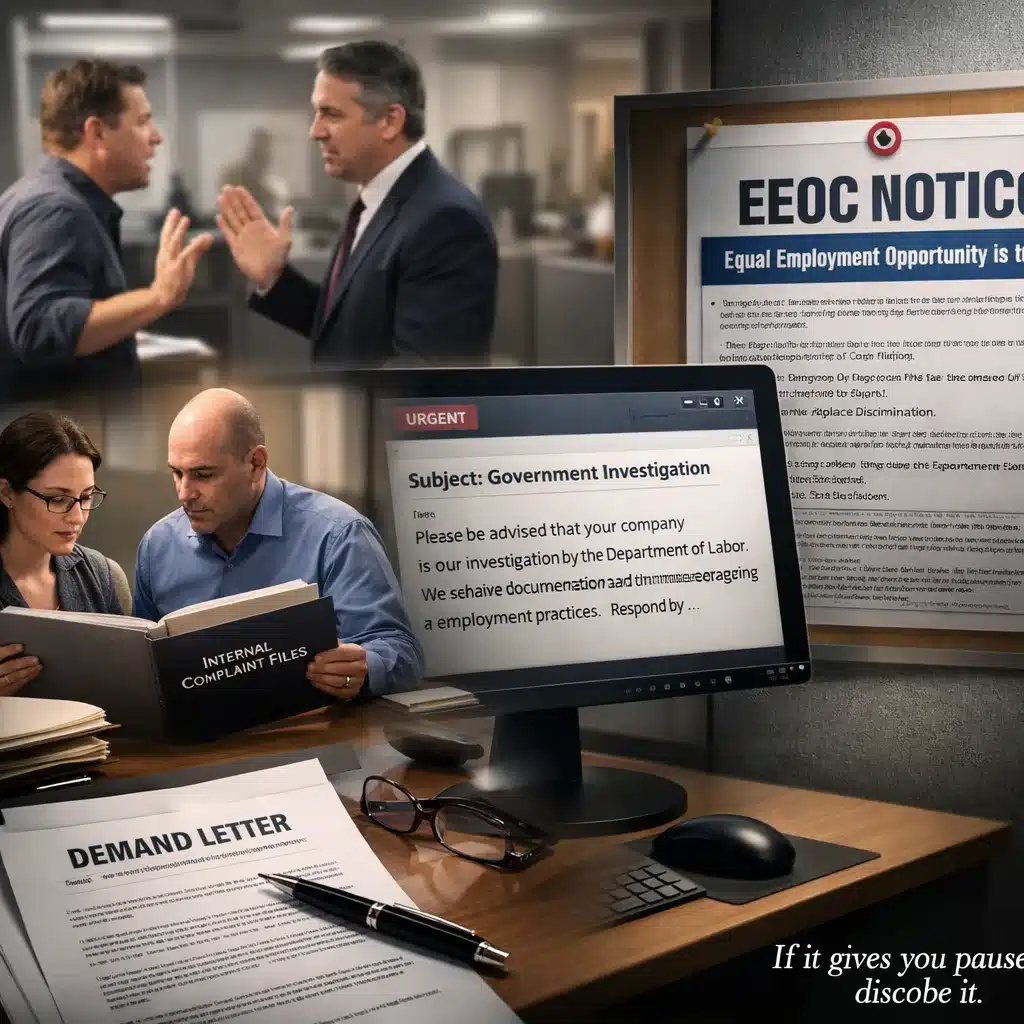

Real-World Example: The SEC Investigation That Voided Coverage

A private equity firm applied for increased D&O limits after their outside counsel received an SEC informal inquiry. The executives discussed the investigation internally and specifically mentioned needing higher insurance limits in those communications. Nevertheless, they did not disclose the SEC inquiry in their warranty statement.

Three years later, when the SEC finally filed charges, the excess insurer denied coverage entirely. During discovery, emails surfaced showing the firm knew about the investigation before purchasing the increased limits. The court ruled the warranty statement barred all coverage under the excess policy, leaving the firm exposed beyond their primary limits.

The takeaway? Even informal inquiries that haven’t yet become formal claims can trigger disclosure requirements if they reasonably could lead to a claim.

What happens if you disclose a potential claim or situation?

In most cases, disclosure does not automatically kill coverage.

Typically, the underwriter will:

However, the disclosed matter will usually be:

Furthermore, the rest of the policy remains intact.

When can disclosure lead to a declination instead of an exclusion?

Disclosure can lead to a declination when the issue is severe or systemic.

Examples include:

In these cases, the insurer may decide the risk is uninsurable at any price.

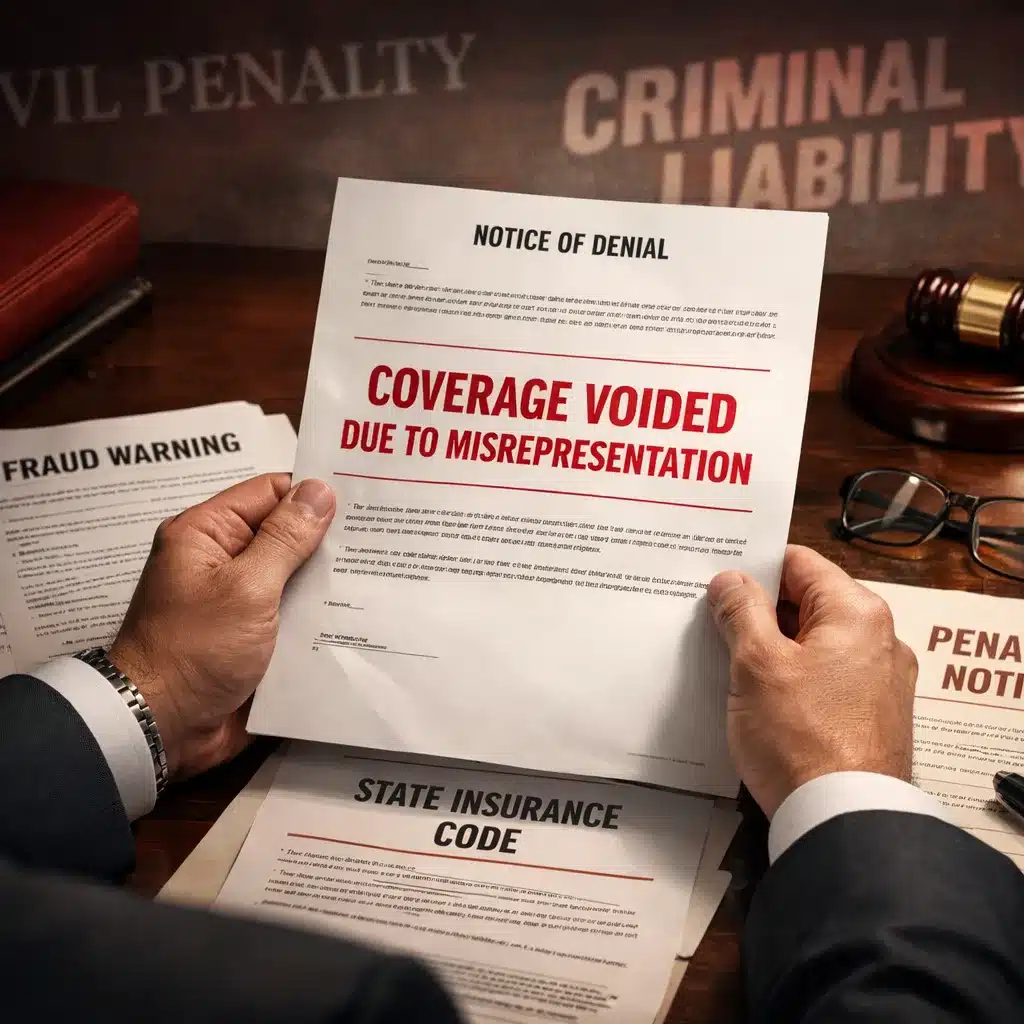

What happens if you fail to disclose something on a warranty statement?

Failing to disclose material information is extremely risky.

Most applications include fraud warnings stating that:

May result in civil or criminal penalties under state law.

This alone makes nondisclosure a poor gamble.

How can a failure to disclose void coverage after a claim is filed?

The greater danger appears after a claim is filed.

During the discovery phase, insurers often uncover:

If the insurer determines you had prior knowledge and failed to disclose it, they may:

At that point, defense costs shift back to you, often mid-litigation.

Why is answering the warranty statement incorrectly so risky for decision makers?

For executives and directors, the risk is personal.

D&O and EPLI claims often:

An invalid policy means:

This is why warranty statements deserve careful, deliberate attention.

When should you be asked to sign a warranty statement and when should you not?

You should sign a warranty statement:

You should not be signing a new warranty:

A new warranty at renewal is a red flag and should be questioned. According to industry experts, requiring fresh warranties at renewal can compromise coverage continuity and should generally be avoided.

How should business owners and executives approach the warranty statement safely?

A practical rule of thumb:

If you’re debating whether to disclose something, disclose it. Honesty now is safer than denial later. The goal is not to get coverage at all costs, it’s to get coverage that actually responds when needed.

Working with an experienced advisor helps:

Understanding the difference between severability provisions can also help protect innocent directors and officers when one person fails to disclose properly.

Learn more about how severability protects board members

Can You Negotiate Warranty Statement Language?

Yes. Warranty statements are negotiable, but most business owners don’t realize this until it’s too late.

In my experience, companies that work with knowledgeable brokers and coverage counsel before signing often secure better warranty language than those who treat the application as routine paperwork.

What Can Be Negotiated

1. Subjective vs. Objective Language

Push for subjective knowledge language (“facts you are personally aware of”) rather than objective language (“facts a reasonable person would know”). Objective warranties are more dangerous because courts have ruled that knowledge held by your attorneys or key executives can be imputed to the company, even if the CEO personally didn’t know.

2. Limit Whose Knowledge Counts

The broader the definition of “knowledge,” the greater your exposure. Negotiate to restrict the warranty to the actual knowledge of specific named individuals, typically the CEO, CFO, and General Counsel, rather than “any person proposed for coverage.”

3. Apply the Warranty Only to New Limits

When adding coverage layers or increasing limits, negotiate warranty language that applies only to the new coverage, not your existing limits. This way, if a coverage dispute arises, at least your base limits remain protected.

For example, in Rivelli v. Twin City Fire Insurance Company, the warranty applied only to an additional $2.5 million layer. When a dispute arose, the policyholder still recovered under the original $2.5 million in limits because the warranty didn’t touch them.

4. Require Full Severability Language

Strong severability provisions protect innocent directors and officers when someone else fails to disclose properly. A typical full severability clause states that the application will be treated as a separate application for each insured, and that one person’s knowledge won’t be imputed to others.

Without severability, one executive’s failure to disclose can void coverage for the entire board.

5. Secure Non-Rescission Protection

Negotiate language preventing the insurer from rescinding the entire policy based on application misrepresentations. This is particularly critical for Side A (personal asset protection) coverage.

What Typically Cannot Be Negotiated

Insurers will not eliminate the warranty statement entirely. The fundamental requirement, confirming you’re not aware of impending claims, protects them from insuring the “burning barn.” However, the specific wording, scope, and whose knowledge triggers the warranty are all fair game.

The Process Matters

Before signing any warranty statement:

The companies that treat warranty statements as boilerplate often regret it when claims arise. Those that negotiate the language upfront protect themselves from coverage disputes that could have been avoided.

Frequently Asked Questions

Taking the Right Approach to Warranty Statements

Warranty statements deserve serious attention from business leaders. They’re not mere formalities, they’re binding declarations that can determine whether your management liability coverage responds when you need it most.

The executives and directors who understand this distinction approach warranty statements with appropriate care. They work with experienced advisors, disclose when uncertain, and ensure their coverage genuinely protects against the risks they face.

Don’t treat your warranty statement as routine paperwork. Moreover, the consequences of getting it wrong extend far beyond premium dollars, they can impact your personal financial security and peace of mind.

If you have questions about warranty statements, coverage continuity, or how to properly complete management liability applications, reach out to a specialist who can guide you through the process correctly.

Author’s Expertise

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping executives and directors structure comprehensive management liability programs that genuinely protect when claims arise.