Quick Answer

Garage insurance (also called garage liability insurance) covers your legal liability to customers and third parties from your shop’s operations. Garage keepers insurance covers physical damage to customer vehicles left in your care. Both coverages are essential for any auto service business. Buying only one of the two leaves a critical gap: garage liability will not pay to repair a customer’s car that was damaged on your lot, and garage keepers insurance will not pay for a slip-and-fall lawsuit.

Garage liability insurance and garage keepers insurance are the two foundational coverages for any auto service business, but they protect against completely different types of claims. Auto repair shop owners who treat them as interchangeable, or who carry one without the other, discover the gap when a claim is denied. Understanding what each policy does, and why both are required, is the starting point for any properly structured garage insurance program.

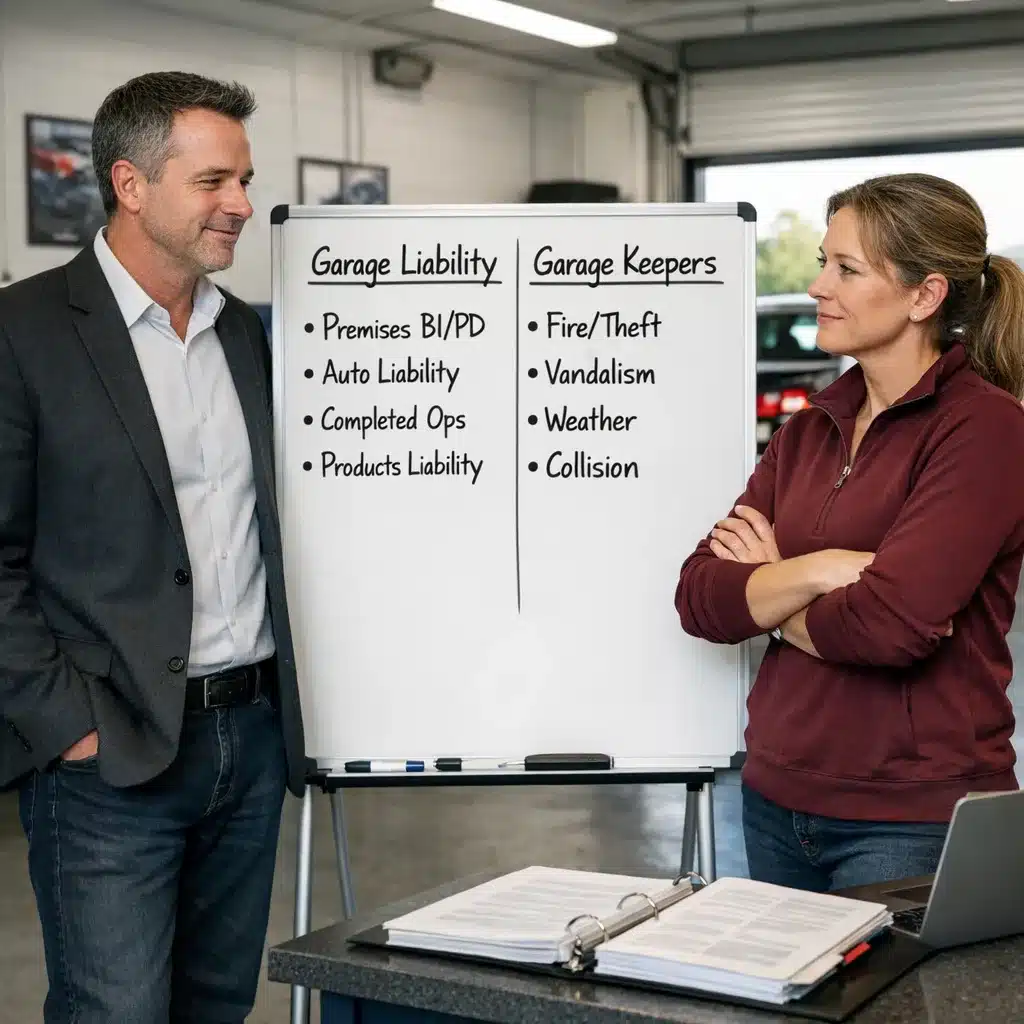

Garage liability insurance is the liability backbone of an auto service business. It covers your legal obligation to pay damages for bodily injury, property damage, and auto liability arising from your shop’s operations. Garage keepers insurance is entirely different: it covers physical damage to customer vehicles that are in your care, custody, or control while at your shop for service, storage, or repair.

What Is Garage Liability Insurance and What Does It Cover?

Garage liability insurance is the liability foundation every auto service business needs before it opens its doors. It covers claims alleging that your shop’s operations caused bodily injury or property damage to a third party. According to the Auto Care Association, there are 280,307 auto service outlets operating in the United States, and virtually every one of them faces premises liability and operations liability exposure that a standard commercial general liability policy does not adequately address.

What Is Garage Keepers Insurance and What Does It Cover?

Garage keepers insurance covers physical damage to customer vehicles while they are in your care, custody, or control. This coverage gap is the most commonly misunderstood risk in auto service insurance: garage liability insurance does not pay for damage to a customer’s car. If a customer’s vehicle is damaged by fire, theft, vandalism, or an accidental collision while at your shop, garage keepers is the policy that responds.

Direct Primary vs Legal Liability: The Garage Keepers Choice That Matters Most

Garage keepers insurance comes in two fundamentally different forms, and choosing the wrong one is one of the most common and costly mistakes auto service business owners make. The difference determines whether your customer is made whole quickly, or whether your shop ends up in a protracted dispute about legal fault.

Legal Liability Form

Legal liability garage keepers only pays when the shop is legally at fault for the damage. If a customer’s car is stolen from your lot and you have adequate security in place, legal liability coverage may deny the claim because no negligence is established. The premium is lower, but the coverage gap is real.

Direct Primary Form

Direct primary garage keepers pays regardless of fault. If a hailstorm damages all the vehicles on your lot, direct primary coverage pays for every one. This is the form that most auto service businesses should carry. The premium is higher, but it eliminates disputes about fault and provides genuine protection for your customer relationships.

Which Auto Service Businesses Need Both Coverages?

Both garage liability and garage keepers coverage are required for any business that takes custody of customer vehicles. The specific risk profile varies by business type, but both coverages are essential across the board. According to NADA, U.S. auto dealerships alone service millions of vehicles annually, creating enormous aggregate garage keepers exposure.

Business Type |

Garage Liability |

Garage Keepers |

Key Notes |

|---|---|---|---|

|

Required |

Required |

Both essential; direct primary recommended |

|

|

Body shop |

Required |

Required |

High-value vehicles; direct primary essential |

|

Tire shop |

Required |

Required |

Vehicles in bays and on lot at all times |

|

Transmission shop |

Required |

Required |

Long repair cycles; extended custody period |

|

Towing company |

Required |

Required |

Vehicles in transit add unique exposure |

|

Parking garage/valet |

Required |

Required |

Direct primary is the standard for valet |

|

Auto dealer |

Required |

Required |

Both customer and inventory vehicles |

How Much Do Garage Liability and Garage Keepers Insurance Cost?

Premium for both coverages is driven by payroll, revenue, number of vehicles serviced, lot capacity, and claims history. For most small to mid-size independent repair shops, the combined annual cost of a well-structured garage insurance program falls between $3,000 and $8,000. For a detailed breakdown by shop type and region, see our dedicated guide to garage insurance cost.

Coverage |

Typical Annual Range |

Key Cost Drivers |

|---|---|---|

|

Garage liability |

$1,300 to $2,500 |

Payroll, square footage, completed operations exposure |

|

Garage keepers (legal liability) |

$200 to $400 |

Lot capacity, average vehicle value, location |

|

Garage keepers (direct primary) |

$500 to $1,500 |

Lot capacity, vehicle mix, maximum custody value |

|

Full combined program |

$3,000 to $8,000+ |

All factors combined; claims history most significant |

Building a Complete Garage Insurance Program Beyond the Core Two

Garage liability and garage keepers are the foundation, but a complete program for most auto service businesses includes additional components. For auto body shop insurance, the exposure is particularly significant because high-value vehicles are held for extended repair cycles.

Beyond those four core coverages, some shops need additional components. A shop that installs aftermarket equipment should consider inland marine coverage for high-value parts. For auto repair shop insurance programs specifically, an annual review with a specialist broker is the mechanism for keeping coverage aligned with how your business has grown. The Insurance Information Institute reports that commercial auto and property claims costs rose 8.2% in 2024, making current limit adequacy a meaningful concern for shops that have not reviewed their program recently.

Key Benefits of Carrying Both Garage Liability and Garage Keepers Insurance

Carrying both coverages properly structured eliminates the gaps that produce claim denials and protects both your business and your customer relationships.

Why The Coyle Group for Garage Insurance

Gordon Coyle has over 40 years of experience placing insurance for auto service businesses of every size. We work with repair shops, body shops, tire dealers, transmission specialists, and auto dealers across the country. We know which carriers write the best garage forms, what completed operations language to look for, and how to structure garage keepers limits so they reflect your actual maximum custody exposure rather than an average that leaves you underinsured on your worst day.

Questions About Garage Insurance versus Garage Keepers

For general liability insurance questions specific to auto service businesses, understanding the distinction between garage liability and standard commercial general liability is the critical first step. Garage liability forms are specifically designed for automotive operations in ways that standard GL forms are not.

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.