Quick Answer

Ocean cargo insurance protects your goods during sea transit against physical loss or damage, covering the full insured value from origin warehouse to final destination. Unlike carrier liability, which caps at just $500 per package under COGSA, ocean cargo insurance pays for overboard container losses, seawater damage, port theft, and rough handling. Annual open cargo policies typically cost 0.5% to 2% of cargo value. If you import, export, or ship goods by sea, this is not optional coverage.

What Is Ocean Cargo Insurance and Why Carrier Liability Is Not Enough

Ocean cargo insurance protects your goods during transit by sea against physical loss or damage. It covers your financial interest in cargo from warehouse to warehouse, including loading, the ocean voyage, unloading, and inland transport.

Under the Carriage of Goods by Sea Act (COGSA), ocean carriers can legally limit their liability to $500 per package regardless of the actual value of goods inside. Carriers also hold 17 statutory defenses when cargo is lost or damaged, including acts of God and navigation errors. Storm damage? The carrier is not liable. This is federal law, and courts enforce it consistently.

Ocean cargo insurance is your policy covering your financial interest, regardless of who caused the loss. It pays based on the insured value of your goods, not on what the carrier decides to accept responsibility for.

How ocean cargo insurance works for importers shipping from China and Asia

What Ocean Cargo Insurance Typically Covers

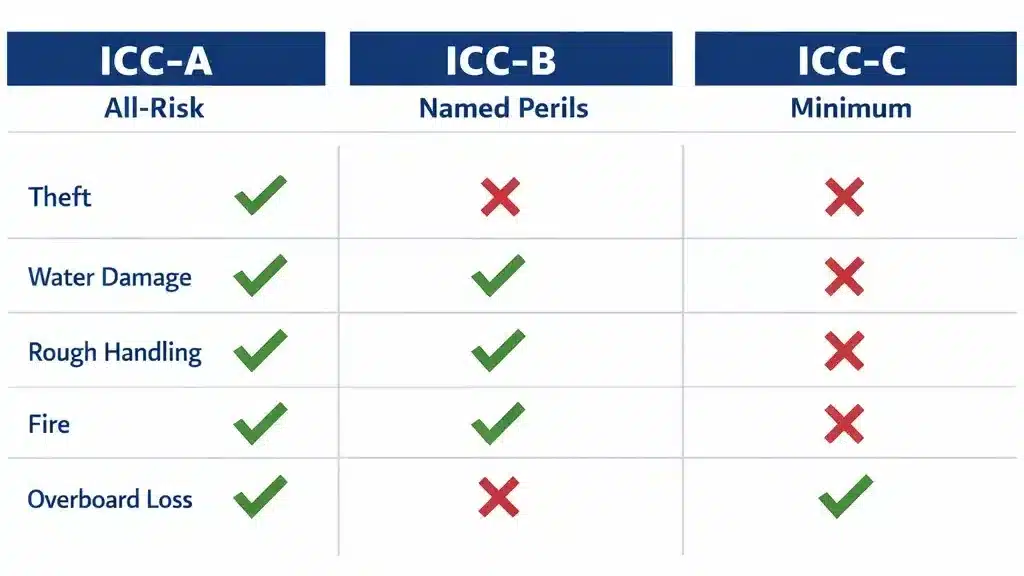

The World Shipping Council reported 576 containers lost at sea in 2024. When yours is the one that goes overboard, all-risk coverage pays the full insured value. Named perils policies only cover the perils specifically listed, leaving out theft, rough handling, and most weather damage.

All-risk (ICC-A) coverage is the broadest available form. You do not need to prove the cause of loss. Most commercial shippers should carry nothing less.

What Ocean Cargo Insurance Does NOT Cover

Packaging failures, delayed delivery financial losses, inherent deterioration, and temperature damage from improper stowage are the most common denial categories. Understanding these exclusions before a loss is what separates businesses that recover fully from those that absorb partial losses out of pocket.

Even all-risk policies have exclusions that eliminate coverage in predictable scenarios. These are not obscure provisions; they are the exact situations where businesses routinely file denied claims.

All-Risk vs. Named Perils: Which Coverage Structure You Actually Need

Named perils policies leave out theft, rough handling, and most weather damage. These are the losses that actually happen most frequently in commercial shipping operations.

The premium difference between all-risk and named perils is typically 0.1% to 0.3% of cargo value. On a $500,000 shipment, that is $500 to $1,500. The coverage gap is not worth the savings for most commercial shipments.

Coverage Type |

What It Covers |

What It Misses |

Best For |

|---|---|---|---|

|

All-Risk (ICC-A) |

All physical loss or damage from external causes unless excluded |

Delay, inherent vice, packaging failures |

Most commercial importers and exporters |

|

Named Perils (ICC-B) |

Fire, explosion, stranding, sinking, collision, earthquake, wave wash, jettison |

Theft, rough handling, most weather damage |

Low-value bulk commodities |

|

Named Perils (ICC-C) |

Fire, explosion, stranding, sinking, collision, jettison |

Theft, rough handling, weather, breakage |

Minimum CIF transactions only |

General Average: The Risk That Hits Even Undamaged Cargo

General average can force you to post a cash deposit equal to 50% or more of your cargo value before your undamaged goods are released from the port. Without ocean cargo insurance, you pay out of pocket and wait years for settlement.

Under general average, when a captain takes voluntary action to save the vessel and all cargo during an emergency, every cargo owner contributes proportionally to the costs, even if their cargo arrived undamaged. All-risk ocean cargo insurance posts the required guarantee and handles the settlement process, releasing your cargo promptly.

What 40+ Years Taught Me About General Average

The Ever Given blocked the Suez Canal in 2021 with over 18,000 containers aboard. The MV Dali hit Baltimore’s Key Bridge in 2024 with over 9,000 containers. In both cases, general average was declared and cargo owners with uninsured goods faced cash demands and months of delays. All-risk cargo insurance covers general average protection, and for many importers, this benefit alone justifies the annual premium.

Incoterms, Coverage Amounts, and How to Avoid Underinsurance

Your Incoterms determine when risk transfers and who is responsible for coverage. Insuring at less than full cargo value triggers coinsurance penalties that reduce partial loss payments proportionally.

The correct insured value formula: Invoice Value + Freight Cost + 10% minimum. If you insure $50,000 on cargo worth $100,000 and suffer a $40,000 partial loss, coinsurance penalties reduce your payment to $20,000. The cost of adequate coverage is a fraction of the cost of getting this wrong.

Incoterm |

Who Arranges Insurance |

When Risk Transfers |

|---|---|---|

|

FOB |

Buyer |

When goods cross the ship’s rail at origin port |

|

CIF (minimum ICC-C only) |

Seller |

When goods cross the ship’s rail at origin port |

|

CIP (broader ICC-A coverage) |

Seller |

When goods delivered to first carrier |

|

DDP |

Seller typically |

At final destination |

For importers, understanding how product liability insurance for importers interacts with cargo coverage is essential. Ocean cargo covers physical damage during transit. Product liability covers claims when products cause harm after successful delivery. You need both. A comprehensive review of how to shop for business insurance ensures ocean cargo coverage is integrated within your complete coverage program.

CASE STUDIES

Real Insurance Outcomes

Explore real-world insurance case studies that show how we helped businesses identify coverage gaps, solve complex risk challenges, strengthen protection, and achieve better insurance outcomes.

Frequently Asked Questions About Ocean Cargo Insurance

Author’s Expertise

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.