Insurance for Private Equity Firms

The Complete Coverage Guide

TL;DR. The Bottom Line

Private equity firms carry risk at three distinct levels:

Generic business insurance fails at every one of them.

PE-specific programs covering D&O, Private Equity Management Liability, E&O, cyber, and portfolio company insurance are the standard today.

The firms that skip them are one LP dispute or SEC inquiry away from a very expensive lesson.

Private equity is a high-stakes business. You’re managing investor capital, making consequential decisions about acquisitions and exits, and operating portfolio companies across multiple industries. Every one of those activities carries legal, financial, and operational exposure that standard commercial insurance was never built to address.

Insurance for private equity firms is a specialized field that requires both PE-specific policy forms and a broker who genuinely understands how the fund structure creates layered liabilities.

The frustration most PE professionals describe is not a lack of awareness about insurance. It is that the process feels commoditized. Brokers treat renewal as a background chore, ask for the same information every year, and hand back a policy that was not designed with a fund structure in mind. Then a claim comes in, and the firm discovers that the policy does not respond the way anyone expected.

This guide covers what you actually need to know: what coverages are essential at each layer of the structure, what the most dangerous gaps look like, how portfolio company coverage should be organized, and what you can expect to pay.

What Makes Insurance for Private Equity Firms Different From Standard Business Coverage?

Private equity firms face a three-layer risk structure that no generic commercial policy is designed to address. Each layer carries distinct exposures, distinct parties who can bring claims, and distinct policy forms required to respond. Understanding this architecture is the first step to building a program that will actually hold up when you need it.

Most businesses operate as a single entity with employees, customers, and vendors. PE firms operate across three interconnected exposure layers simultaneously, each requiring its own coverage approach:

A standard D&O policy addresses the first layer partially. It does nothing for the fund or portfolio layers. That is exactly why PE-specific coverage exists, and why working with a broker who understands the entire structure is non-negotiable.

To have your current PE insurance program reviewed against this three-layer framework.

What Are the Core Insurance Coverages Every Private Equity Firm Needs?

Private equity firms need several specialized coverage lines that go well beyond what a typical business insurance program provides. The exact combination depends on fund size, portfolio complexity, and regulatory profile, but certain coverages are foundational for virtually every PE firm operating today.

Here is a breakdown of the essential coverage lines Every Private Equity Firm Needs:

Directors and Officers (D&O) Insurance

D&O insurance protects the firm’s executives, directors, and officers from personal liability arising from management decisions, fiduciary breaches, or wrongful acts. In the PE context, D&O claims most often arise from investors or regulators alleging mismanagement, conflicts of interest, or failures in the acquisition and exit process. The critical nuance is that entity-level D&O often excludes claims brought by fund investors, meaning the policy the GP bought to protect itself may not respond to an LP lawsuit. That gap requires a PE-specific policy form to close.

Private Equity Management Liability (PEML)

PEML is a bundled policy purpose-built for PE firms and is discussed in detail in its own section below. It combines D&O with employment practices liability, fiduciary liability, and investigations coverage in a single form designed around the GP and fund risk structure.

Errors and Omissions (E&O) / Professional Liability

E&O coverage protects the firm against claims arising from investment advice errors, misrepresentations, or failures in professional services rendered as an investment advisor or fund manager. The SEC’s 2023 rules for private fund advisors specifically flagged E&O limits and retentions as an area advisors need to reassess in light of new regulatory requirements.

Cyber Insurance

Cyber coverage is now a foundational exposure for PE firms, with risk concentrated both in the management company’s own operations and across the portfolio. Data breaches, ransomware at portfolio companies, and wire fraud targeting capital calls are all active threats. This is covered in its own section below.

Fund Liability / Fund Management Liability

Fund Liability insurance addresses GP and fund-level exposures including LP claims, sponsor litigation, outside directorship liability (ODL), and portfolio company creditor issues. This coverage is distinct from entity-level D&O and is essential for any fund that has raised outside capital.

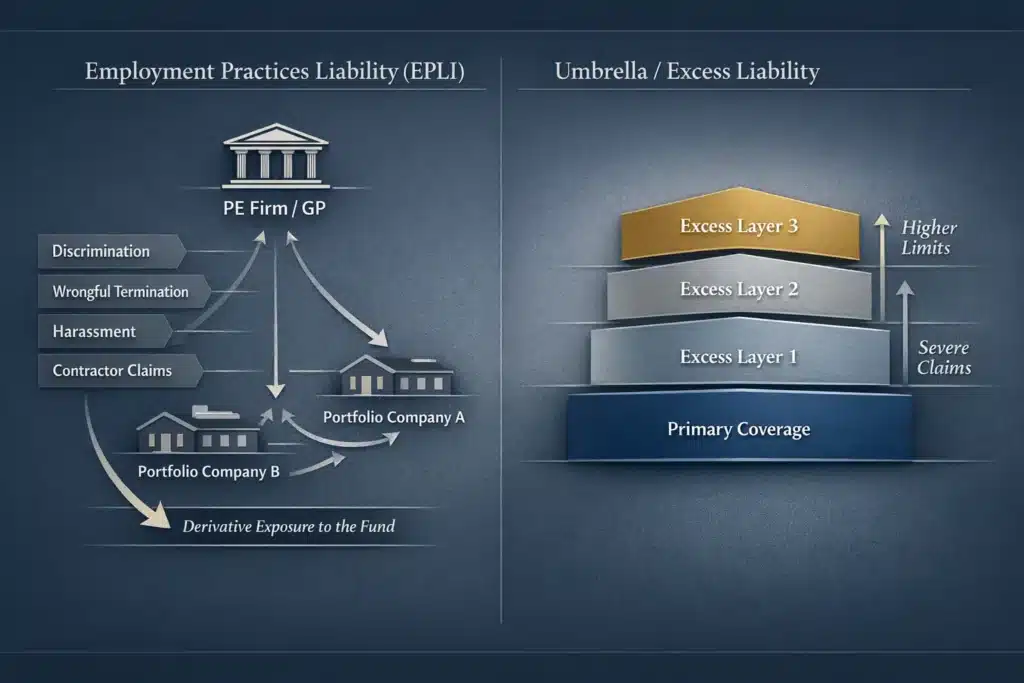

Employment Practices Liability (EPLI)

EPLI covers claims from employees and contractors at the GP entity level for discrimination, wrongful termination, and harassment. PE firms with portfolio companies also need to assess EPLI at the portfolio level, since employment claims at a portfolio company can create derivative exposure back to the fund.

Umbrella / Excess Liability

Umbrella coverage provides additional limits above the primary liability coverages. Given the dollar amounts involved in PE transactions and the potential severity of claims, adequate umbrella limits are essential.

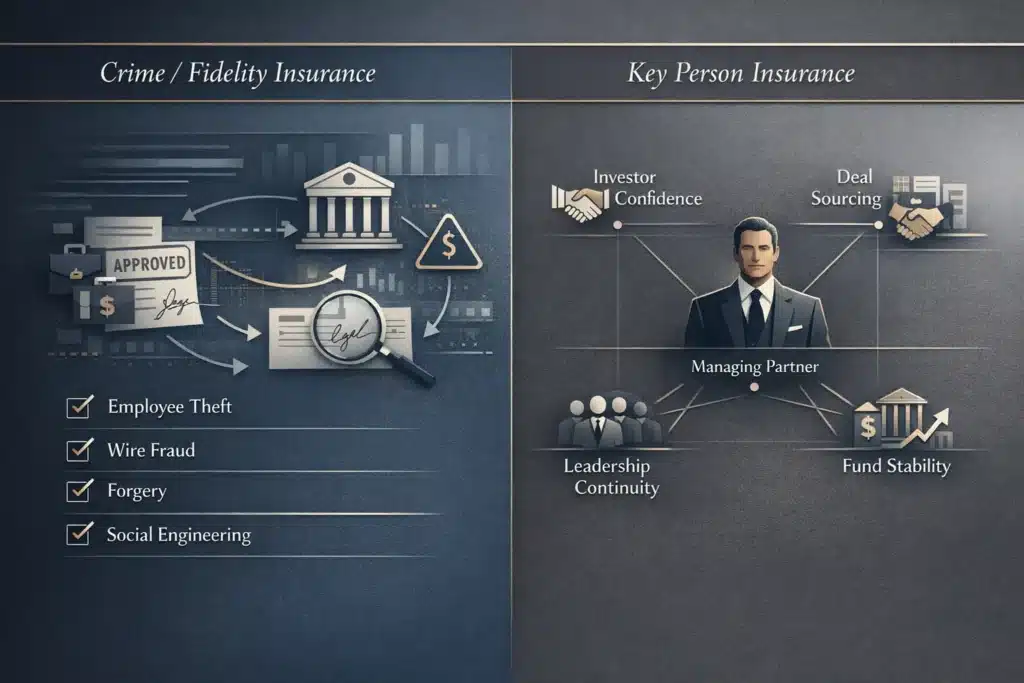

Crime / Fidelity Insurance

Crime coverage protects against losses from employee theft, wire fraud, forgery, and social engineering. For PE firms managing significant capital flows and wire transfer activity, crime coverage is a critical component of the program.

Key Person Insurance

Key person insurance protects the fund against the financial impact of losing a critical GP or managing partner whose relationships and expertise are central to the fund’s investment strategy. For smaller and mid-market PE firms in particular, the departure or death of a key principal can materially affect fund performance and investor confidence.

Contact us if you want to know which of these coverages you currently have and whether the forms and limits are appropriate for your fund structure.

What Is Private Equity Management Liability Insurance (PEML) and Do You Need It?

PEML is a bundled management liability policy designed specifically for the operational structure of a private equity firm. Rather than purchasing separate policies for D&O, employment practices, and fiduciary liability, PEML packages these coverages into a single form with a unified limit and language built around how PE firms actually operate.

If your firm has raised outside capital from limited partners, you need PEML. A standard D&O policy will not respond to many of the most common PE-specific claims because it was not written with the fund structure in mind.

Here is what a PEML policy typically includes:

The investigations coverage component is particularly important given the current regulatory environment. In August 2023, the SEC enacted new rules for private fund advisors under the Investment Advisers Act of 1940, requiring quarterly statements, annual audits, and new restrictions on how advisors allocate certain fees. As NFP noted when the rules were enacted, this makes it critical that advisors carry the broadest investigation and regulatory coverage possible. Any increase in regulatory oversight increases the likelihood of investigations and subsequent litigation.

You can review the specific coverage types relevant to management liability on our site for a deeper breakdown of each component.

The firms most at risk of discovering they have the wrong structure are those that bought D&O years ago, renewed it without review, and assumed it covered everything. It almost certainly does not.

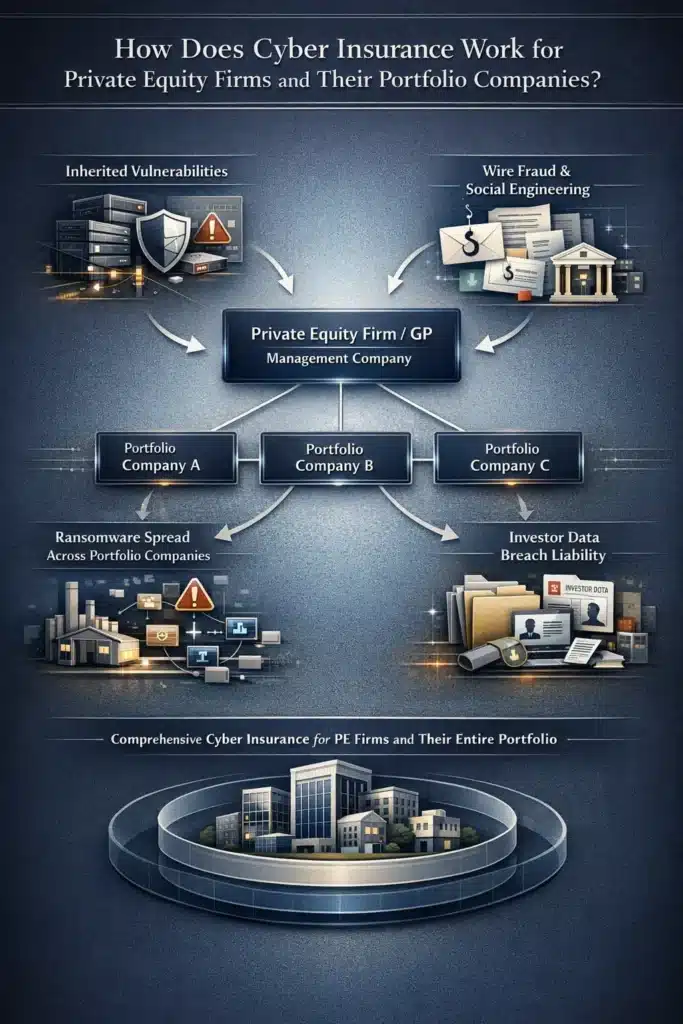

How Does Cyber Insurance Work for Private Equity Firms and Their Portfolio Companies?

Cyber risk in private equity is compounded by portfolio diversity in ways that most firms underestimate at the time of acquisition.

When you acquire a company, you inherit its cybersecurity posture along with its assets and liabilities. That posture is often unknown, unaudited, and inadequate. This creates cyber exposure across the entire fund that has nothing to do with your own IT infrastructure.

Standard cyber policies are written for single operating businesses. A PE firm needs cyber coverage that addresses both the GP entity and the expanded attack surface created by portfolio company ownership.

Key cyber exposures specific to PE firms:

Real-World Example

A mid-market PE firm acquired a regional manufacturer with approximately $85 million in revenue. The cyber diligence during the deal process was limited to a basic questionnaire.

Six months post-close, a ransomware attack was deployed through an unpatched remote desktop protocol vulnerability that had existed at the company for over two years. The response costs exceeded $1.4 million, including forensics, legal notification, remediation, and business interruption.

The PE firm’s existing cyber policy did not include portfolio company coverage, and the manufacturer’s standalone policy had a $500,000 limit with a $100,000 retention. The gap was fully uninsured.

This is the scenario that Reddit discussions around PE insurance come back to repeatedly: the portfolio company had “coverage,” but the policy terms did not match the actual exposure. Post-acquisition, the PE firm discovered niche exposures that portfolio-wide policies had overlooked entirely.

The solution is a purpose-built PE cyber program that covers the GP entity, extends to portfolio companies through a coordinated structure, and treats M&A cyber diligence as part of the underwriting process rather than an afterthought.

With our team to review your current cyber coverage across your fund and portfolio companies.

What Is Representations and Warranties Insurance and When Does a PE Firm Need It?

Representations and Warranties (R&W) insurance has become a standard tool in the PE M&A transaction process, used to protect both buyers and sellers from losses arising from breaches of the representations and warranties made in a purchase agreement. It is not a standalone policy for ongoing firm operations but a transaction-specific coverage tied to each deal.

R&W insurance is now used in the majority of PE-backed M&A transactions above a certain size threshold because it addresses a fundamental tension in deal negotiations: the seller wants a clean exit with minimal indemnification exposure, while the buyer needs protection against unknown liabilities in the acquired business.

Here is how R&W insurance fits into a PE transaction:

R&W insurance does not eliminate the need for thorough diligence. It is a complement to diligence, not a substitute for it. Underwriters will review diligence materials and exclude known issues from coverage. The areas where your diligence identified problems will not be covered. That is exactly why comprehensive pre-close diligence, including insurance diligence, remains essential.

How Should Private Equity Firms Structure Insurance Across Their Portfolio Companies?

The default approach at many PE firms is to leave each portfolio company managing its own insurance independently. That approach costs more, creates coverage inconsistencies, and leaves the fund exposed to gaps that a coordinated program would eliminate. It also creates the exact dynamic that PE professionals complain about most: portfolio companies without tailored support, negotiating alone against insurers with no leverage.

A structured portfolio insurance approach, sometimes called a portfolio insurance master program, allows a PE firm to negotiate coverage on behalf of all portfolio companies collectively, using the combined scale to achieve better pricing and more consistent terms.

According to WTW’s Alternative Asset Insurance Solutions team, which has implemented more than 100 portfolio insurance programs for PE firms over the past two decades, the advantages extend well beyond cost savings.

Benefits of a centralized portfolio insurance program:

The firms that benefit most from centralized programs are those with five or more active portfolio companies across diverse industries. Below that threshold, individual company programs with coordinated oversight can be sufficient, but only if someone is actively managing coverage quality at each company.

Working with an insurance broker experienced in private equity is the critical factor in making a portfolio program work. A generalist broker does not have the carrier relationships or PE-specific knowledge to structure these programs correctly.

What Does Insurance for Private Equity Firms Typically Cost?

Insurance for private equity firms costs vary significantly based on fund size, number and type of portfolio companies, regulatory history, and claims history. There is no single rate that applies across the industry, and any broker quoting you without a thorough submission and program design process is guessing.

One pattern worth noting from market data: individual portfolio companies without purchasing leverage regularly experience renewal premium increases in the range of 20 to 33% in hardening market conditions. Firms with centralized portfolio programs absorb market pressure better because consolidated premium volume gives them strategic negotiating power that standalone companies simply do not have.

Here are the primary factors that drive cost:

Coverage Type |

Typical Limit |

Estimated Annual Premium |

|---|---|---|

|

D&O / PEML (mid-size PE firm) |

$5M – $10M |

$25,000 – $100,000+ |

|

$5M – $10M |

$15,000 – $50,000+ |

|

|

Cyber (GP entity only) |

$5M |

$10,000 – $30,000 |

|

Cyber (portfolio master program) |

Varies by portfolio |

$50,000 – $250,000+ |

|

R&W Insurance (per deal) |

Deal-specific |

2-4% of policy limit |

|

Key Person Insurance |

Deal-specific |

Varies by principal |

|

Fund Liability |

$5M – $10M |

$20,000 – $75,000+ |

|

$10M – $25M |

$15,000 – $50,000+ |

These are ranges, not quotes. The actual cost for your firm depends on the details of your fund, your portfolio, and your risk profile. What you should be skeptical of is any broker who gives you a number before doing the work to understand your specific situation.

for a structured review of your current program and a market assessment of what your coverage should cost.

What Are the Most Common Insurance Gaps PE Firms Discover After a Claim?

In my experience working with PE firms across the US, the gaps that hurt most are not the ones anyone anticipated. They are the ones that were never reviewed because everyone assumed the existing policy covered it. By the time a claim surfaces, the gap is already there and the options are limited.

Here are the most consistently dangerous coverage gaps in PE insurance programs:

Gap 1: LP Dispute Exclusions in Entity-Level D&O

Entity-level D&O policies often contain exclusions for claims brought by investors in the fund. This means a limited partner suing the GP for alleged mismanagement of fund assets may not be covered by the D&O policy the GP bought to protect itself. PEML or Fund Liability coverage is required to close this exposure.

Gap 2: Portfolio Company Cyber Not Covered

A PE firm’s cyber policy covers the management company’s operations. It does not automatically extend to portfolio companies. A cyber incident at a portfolio company (ransomware, data breach, business interruption) falls entirely on the portfolio company’s own policy, which may have inadequate limits.

Gap 3: No Tail Coverage at Exit

When a PE firm exits a portfolio company through a sale, the D&O coverage for that period of ownership ends. Tail coverage (also called extended reporting period coverage) extends the ability to report claims arising from the covered period after the policy has been terminated. Without it, directors have no protection for claims filed after exit.

Gap 4: Fund-Level Liability Not Covered by Entity-Level Policies

Many PE firms discover that their D&O policy was written at the management company level and does not extend to cover claims made against the fund entity itself. LP disputes, carried interest litigation, and co-investor claims against the fund require fund-level coverage that must be specifically placed.

Gap 5: Inadequate Limits Relative to AUM Growth

A $5 million D&O policy was adequate when the fund managed $200 million. When AUM grows to $800 million, that limit is dangerously insufficient. Most firms do not proactively increase limits as the fund grows, and underwriters do not call to suggest it.

Gap 6: No Investigations Coverage

Regulatory investigations are expensive before they ever become formal proceedings. A PEML policy without a robust investigations coverage component leaves the firm paying those costs out of pocket. The SEC’s 2023 private fund rules made this exposure significantly more relevant for all registered PE advisors.

Work With a Broker Who Understands Private Equity

Insurance for private equity firms is not a product. It is a program that has to be built around your fund structure, your portfolio, your regulatory profile, and your stage in the fund lifecycle.

And we will show you exactly where your gaps are.

CASE STUDIES

Real Insurance Outcomes

Explore real-world insurance case studies that show how we helped businesses identify coverage gaps, solve complex risk challenges, strengthen protection, and achieve better insurance outcomes.

Questions about Insurance for Private Equity Firms?

Get the Right Coverage for Your Private Equity Firm

Insurance for private equity firms is not a product. It is a program that has to be built around your fund structure, your portfolio, your regulatory profile, and your stage in the fund lifecycle. A generalist broker who treats your renewal as a background task and hands back a standard commercial package does not have the market relationships or the PE-specific knowledge to protect you when a claim comes in.

The Coyle Group works with private equity firms and fund managers across the US to build programs that address all three exposure layers: the GP entity, the fund, and the portfolio. If your current program has not been reviewed by someone who actually understands how PE firms work, the odds are high that there are gaps.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s How To Take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

VC Insurance: 4 Essential Coverages Every Venture Capital Firm Needs

How to Get the Best Venture Capital Insurance: A Practical Guide for Fund Managers

Business Insurance for Financial Advisors