Cyber Insurance Quote Form

Before You Fill Out a Cyber Insurance Quote Form, Read this

Stop Using Cyber Insurance Quote Forms

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

You’re searching for a cyber insurance quote form. Fill in a few details, get a number, move on. For straightforward situations, online forms may work fine. But here’s what happens more often: form-based cyber insurance quotes almost always miss what actually matters.

Ransomware incidents frequently exceed seven figures once downtime, forensics, and legal costs are included, yet most form-based quotes fail to account for your specific risk exposure.

They cost you money through undercoverage or unnecessary premiums.

The better approach? Talk to an expert first. Then get a quote that works.

The Bottom Line. TL;DR

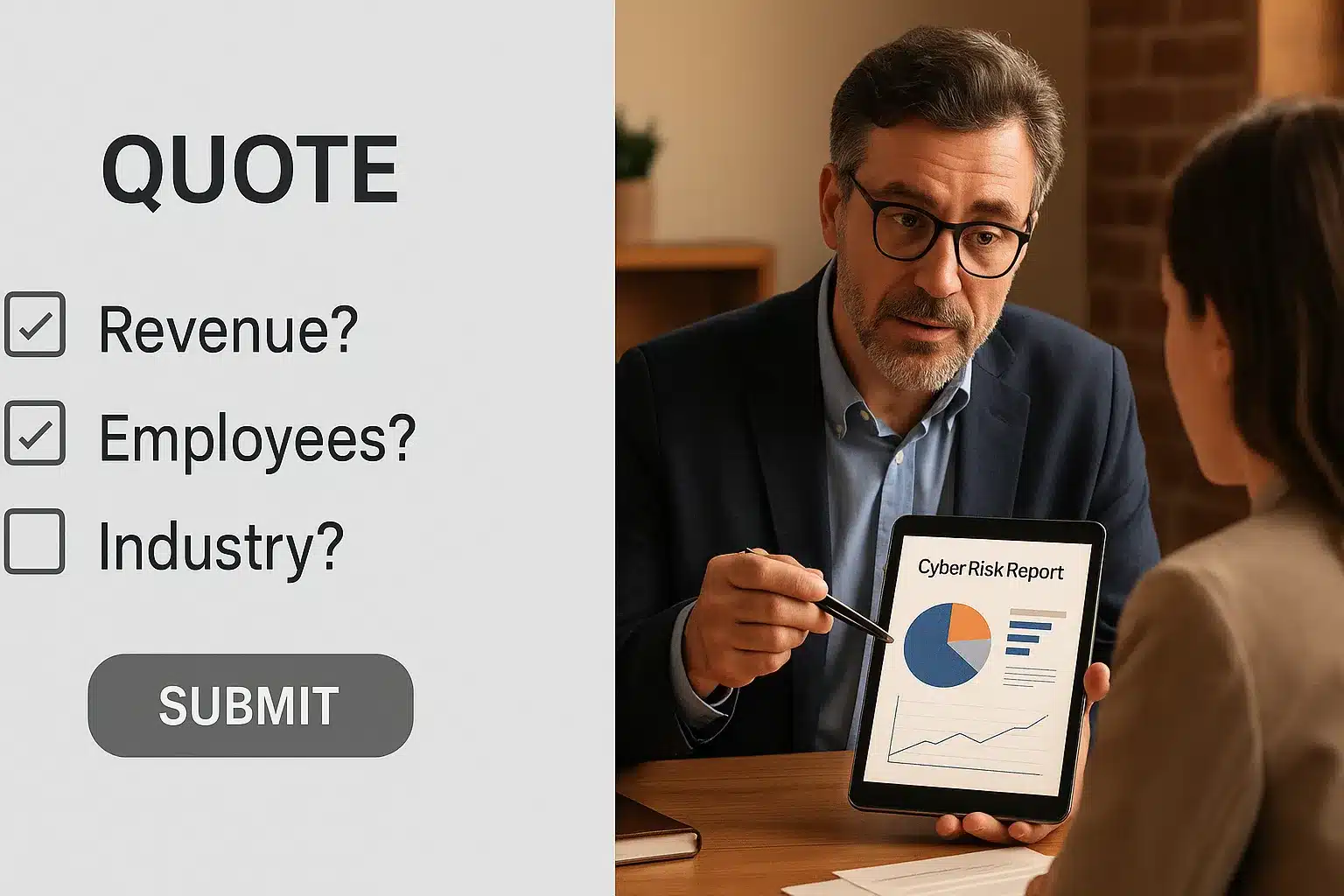

What a Cyber Insurance Quote Form Actually Delivers

A cyber insurance quote form is designed for one thing: speed.

You fill in basic information, company size, industry, revenue, and an algorithm generates a quote based on broad industry benchmarks. The form optimizes for simplicity and volume, built so anyone can complete it in 10 minutes without expert knowledge.

The Problem with Algorithmic Quotes

Here’s what these forms miss:

The algorithm bets a template designed for thousands fits yours. It usually doesn’t.

Why Generic Cyber Insurance Quotes Fall Short

When you’re not a cyber insurance expert. Filling out a form feels logical. But it’s a shortcut that leads in the wrong direction.

The Questions Forms Don’t Ask

Only 18% of applicants can confirm complete implementation of four core security controls. Generic forms can’t identify these gaps, but they determine whether you qualify and what you’ll pay.

What 40+ Years Taught Me About This Risk

After four decades helping businesses navigate insurance, I’ve seen the same mistake repeatedly: owners who assume “no news is good news” when their form-based quote arrives. They purchase coverage, unaware they’re underinsured, until a claim happens. Businesses that avoid this trap treat cyber insurance as a strategic decision. They ask questions, reassess needs, and consistently secure better coverage at better prices.

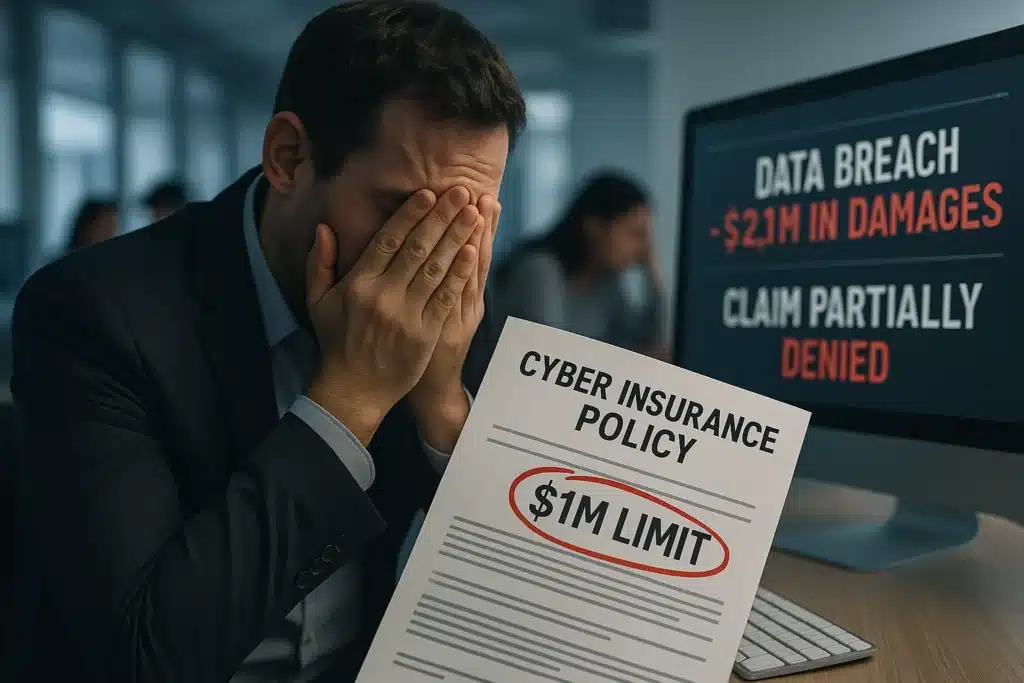

Real-life example:

A 35-employee marketing firm filled out an online form, got approved for $1M coverage at $140/month. Seemed perfect. Eight months later, a vendor email compromise drained $680K from their account. Their claim was denied, and the form never asked if they had MFA on their accounting software. They didn’t. The policy required it. The business took 18 months to recover financially, lost three major clients, and the owner remortgaged his home to cover payroll.

The form worked fine for getting a quote. It failed completely at getting coverage that would actually pay.

Businesses that avoid this trap treat cyber insurance as a strategic decision. They verify their security controls match policy requirements before buying, not after filing a claim.

This real example illustrates a broader pattern we see in client claims, which we unpack next.

The False Economy Problem: Cheap Quote, Expensive Regret

Most SMBs see a low-priced form quote and think they’ve found a deal. Then they discover the trade-off. Form-generated premiums are priced against broad industry averages, not your actual risk exposure. When deductibles, sublimits, and excluded endorsements reveal themselves during a claim, the savings evaporate.

Common Quote Form Pitfalls

While many businesses pay less than $100 per month, costs vary significantly:

Deductible Surprises Form quote:

Your form quote shows a $5,000 deductible and a $1M limit. Sounds safe.

Here’s what actually happens in a ransomware event.

All of this erodes the same $1M limit.

But here’s the problem most forms don’t show:

By the time operations resume, you haven’t exceeded the deductible, you’ve exhausted usable coverage.

Coverage Limit Inadequacy

SMB cyberattack average: $254,445, but that number blends minor phishing incidents with catastrophic ransomware events.

When ransomware triggers forensic response, legal exposure, notification obligations, restoration, and downtime at the same time, $1M disappears faster than most owners expect.

That’s why form-based limits feel sufficient on paper, and inadequate in real claims.

Missing Endorsements:

Ransomware response, business interruption, legal defense, and breach notification. These are often limited, excluded, or sub-limited in form-based quotes unless explicitly negotiated. The few dollars saved with a generic quote cost far more when you discover coverage gaps.

Don’t risk undercoverage. Schedule your call to assess your actual cyber insurance needs.

What Form-Based Quotes Miss About Requirements

The cyber insurance market has evolved dramatically. Insurers now demand proof of strong security measures before considering a policy. A form that asks “do you have MFA?” is not the same as verifying it’s deployed across all systems. The gap between what forms accept and what underwriters actually require at claim time is where most coverage failures originate.

Mandatory Security Controls

Top insurance requirements include:

Critical Reality

If forensic investigators find that your security controls weren’t implemented (not just listed on a form), expect claim denial.

Unsure if you meet the 2025 requirements? Book a call for a complimentary security assessment.

What Happens Without Documentation

Form-based quotes don’t verify your security. They ask if you “have MFA” but don’t confirm deployment across ALL systems, verify reports, or prove it works.

Understanding what cyber insurance covers requires knowing both coverage AND obligations.

Hidden Risks of Passive Form Submission

Submitting a form and accepting the quote feels like a decision made. But passive form submission creates four distinct risks that compound over time, risks most businesses don’t discover until a claim is filed or a non-renewal notice arrives.

1. Coverage Drift

Your operations evolved, but the form didn’t capture: new cloud systems, e-commerce platform, additional vendors, and remote workforce expansion.

Carriers now expect documented vendor cybersecurity requirements.

2. Missing Compliance Elements

Data collection is the most negotiated coverage aspect. New privacy laws may require elements standard forms don’t include: CCPA, GDPR (if handling EU data), HIPAA (healthcare), industry-specific regulations.

Understanding the difference between first-party and third-party cyber coverage prevents claim surprises.

3. Missed Savings Opportunities

Direct premiums for cyber insurance declined 2.3% in 2024, the first decrease since 2015. Nearly two-thirds of businesses realized savings, but only those who properly shopped coverage.

Organizations with MDR saw 10%+ premium savings.

4. Carrier Appetite Changes

Your insurer might have exited your industry. Non-renewal notices often arrive with 30-60 days’ warning, not enough time for quality replacement.

How The Coyle Group Approaches Cyber Insurance Differently

We don’t process quotes; we have conversations. When clients reach out about cyber insurance, we start with understanding what you actually do and what you’re trying to protect.

Our Strategic Process

Understanding Your Business

We ask about your operations: What data do you handle? Who are your customers? What systems would shut down your business if they went offline? These aren’t questions a form can capture.

Identifying Your Actual Exposures

Based on 40+ years working with businesses like yours, we can spot gaps most owners miss. A manufacturer faces different cyber risks than a financial advisor. Generic forms treat everyone the same.

Navigating Carrier Requirements

We know what different carriers actually require, not just what their forms say. Some insurers are strict about MFA deployment. Others focus on backup testing. We help you understand expectations before you apply, not after a claim is denied.

Market Access

We work with 20+ cyber carriers. That means if one carrier doesn’t fit your risk profile or budget, we have alternatives. Form-based quotes typically show 1-3 options.

Plain-English Guidance

Cyber policies are complex. We explain what you’re actually buying, what’s excluded, and what you need to document. Most importantly, we tell you what could void your coverage before you sign.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

Want to know your actual exposure?

Real-World Example: The Cost of Form-Based Quotes

When to Start Your Cyber Insurance Assessment

Don’t wait for renewal. If you’re approaching coverage decisions, start the conversation 30-90 days before you need the policy. Starting early gives you time to address security gaps before underwriters review your application, shop multiple carriers, and document controls that directly affect your premium. Last-minute decisions result in higher costs and fewer options.

Strategic Timeline

Understanding the Cyber Insurance Market

Market outlook shows stable rates (-5% to +5% forecast) with plentiful capacity, but only for businesses with strong security controls. Businesses with documented MFA, EDR, and tested backup protocols are seeing flat or declining premiums. Businesses without are facing restrictions, higher deductibles, or outright declinations. The market rewards preparation and penalizes form-based assumptions.

Key Market Trends

Market Size and Growth

The global cyber insurance market tripled in five years to $13 billion. Some reports project $29 billion by 2027, but access increasingly depends on demonstrating comprehensive cybersecurity.

What Makes Strategic Cyber Insurance Different

A form-based quote compares you to thousands of similar businesses and prices you accordingly. A strategic assessment treats you as one business with a specific risk profile, specific security posture, and specific exposures, and structures coverage around that reality.

Form-Based Quote vs. Strategic Assessment

Questions about Cyber Insurance Quote Form?

Taking Control of Your Cyber Insurance Coverage

Your cyber insurance decision is too important for a checkbox exercise. Form-based quotes offer convenience but sacrifice customization, accuracy, and expertise that protect your business.

Why Work with The Coyle Group

Don’t settle for algorithm-generated numbers. Strategic assessment identifies your actual risks, documents security controls, and secures coverage that works when you need it.

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience solving insurance challenges for businesses across the US. Gordon specializes in comprehensive cyber insurance programs, helping hundreds navigate complex coverage decisions and secure optimal protection.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Tech E&O vs. Cyber Insurance: What You Need to Know

First Party vs Third Party Cyber Insurance: What’s Covered, What’s Missing, and What You Actually Need