Fiduciary Liability Insurance: What Is It? Why Do You Need It?

Operating a retirement plan for your employees creates legal obligations most business owners never anticipated. A single administrative error, investment choice, or plan document oversight can trigger lawsuits that put both company assets and personal wealth at risk.

The reality facing plan sponsors: ERISA excessive fee litigation surged by 35% in 2024, with 136 new cases filed, a 183% increase from the previous year. These lawsuits target businesses of all sizes, and the financial consequences extend far beyond insurance premiums.

At The Coyle Group, we’ve spent four decades helping business owners protect themselves from ERISA exposures. Fiduciary liability insurance addresses a unique risk that standard policies like D&O insurance or general liability simply don’t cover.

The Bottom Line. Key Takeaways

What Is ERISA?

Employee

Retirement

Income

Security

Act

The Employee Retirement Income Security Act of 1974 (ERISA) sets minimum standards for retirement and other benefit plans. This federal law doesn’t require employers to establish benefit plans, but once you offer them, ERISA imposes strict fiduciary duties on those managing the plans.

What 40+ Years Taught Me About This Risk

After four decades helping business owners navigate insurance challenges, I’ve seen the same pattern repeatedly: successful companies establish 401(k) plans to attract talent, appoint themselves as trustees, and never realize they’ve created significant personal liability exposure. The businesses that avoid costly surprises treat fiduciary coverage as essential infrastructure, not an optional add-on.

Understanding Fiduciary Duties Under ERISA

ERISA imposes strict duties and obligations upon the trustees or fiduciaries of employee retirement and benefit plans. These responsibilities include:

Core Fiduciary Obligations:

Violating these duties, or even appearing to violate them, exposes fiduciaries to lawsuits, fines, penalties, and government investigations.

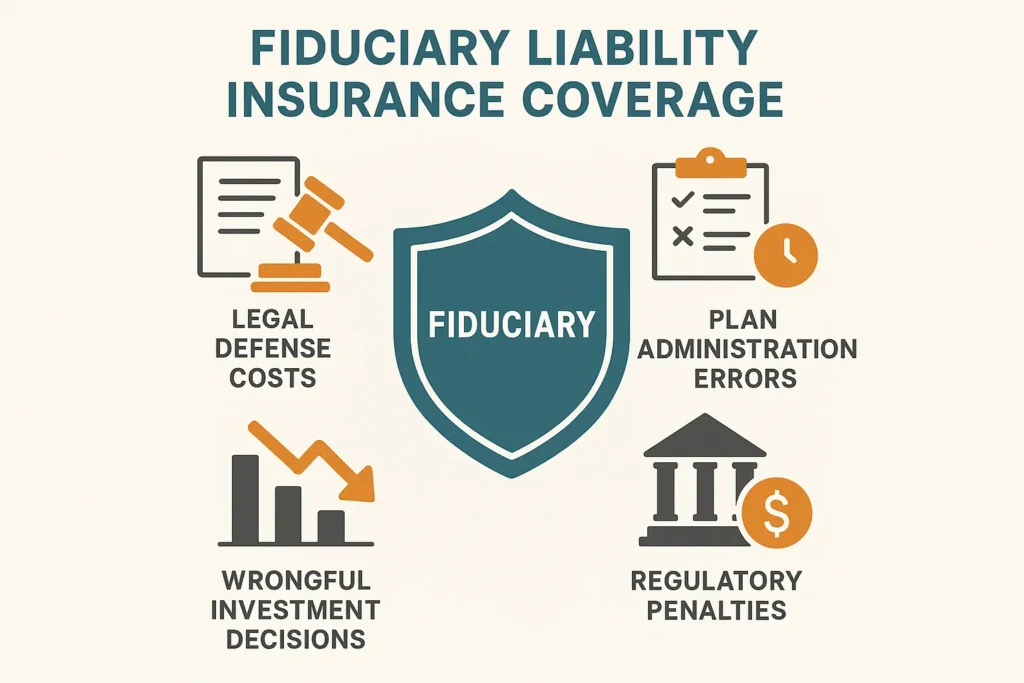

What Is Fiduciary Liability Insurance?

Fiduciary liability insurance protects individuals and companies from claims alleging mismanagement of employee benefit plans. This coverage typically forms part of a management liability insurance portfolio alongside D&O and EPLI policies.

Who Needs This Protection?

Trustees of ERISA-based plans typically include:

Critical point: These individuals face personal liability for fiduciary breaches. Your personal assets, homes, savings, investments, are at risk without proper insurance.

Common Fiduciary Liability Claims

Between 2016 and 2023, plaintiffs’ lawyers filed just over 460 excessive fee lawsuits. The litigation landscape continues expanding into new areas beyond traditional excessive fee claims.

Claim Type |

What Triggers It |

Recent Trends |

|---|---|---|

|

Excessive Fees |

Failing to negotiate lower recordkeeping or investment management fees |

Most common claim type; settlements ranging from $200,000 to $124.6 million |

|

Imprudent Investments |

Selecting underperforming funds or failing to remove poor options |

Increasing focus on target-date fund performance |

|

Forfeiture Mismanagement |

Using forfeitures to reduce employer contributions vs. participant expenses |

28 new forfeiture cases filed in 2024 |

|

Plan Design Challenges |

Actuarial assumptions, pension risk transfers, benefit calculations |

Emerging theory challenging settlor functions |

|

Health Plan Fees |

Excessive prescription drug costs, pharmacy benefit manager fees |

New frontier, first lawsuits filed against J&J and Wells Fargo |

|

Wellness Program Violations |

Premium surcharges based on tobacco use |

More than 20 putative class actions filed in 2024 |

|

Conflicts of Interest |

Self-dealing, using proprietary funds without justification |

Scrutiny of party-in-interest transactions |

|

Administrative Errors |

Failure to enroll eligible employees, incorrect benefit calculations |

Covered by employee benefits liability if simple mistakes |

Real-World Example: The Cost of Administrative Oversight

Consider a mid-sized manufacturing company with 200 employees and a $5 million 401(k) plan. The finance director, serving as plan administrator, used plan forfeitures to offset company contributions, a common practice explicitly allowed in the plan document.

A former employee filed a class action claiming this violated fiduciary duties, arguing forfeitures should have reduced participant fees instead. Defense costs alone exceeded $800,000 before reaching a $1.2 million settlement.

Without fiduciary liability insurance, these costs came entirely from company operating funds and personal assets of the named fiduciaries.

What Fiduciary Liability Insurance Covers

Coverage Components

Coverage Element |

What It Protects |

Typical Limits |

|---|---|---|

|

Defense Costs |

Attorney fees, expert witnesses, court costs |

Unlimited defense costs in most policies |

|

Settlements |

Negotiated resolutions of fiduciary breach claims |

Up to policy limits |

|

Judgments |

Court-ordered damages for breach of fiduciary duty |

Up to policy limits |

|

Regulatory Defense |

DOL or IRS investigations and audits |

Sublimits of $100K-$500K |

|

Plan Restitution |

Making plan participants whole after fiduciary breach |

Up to policy limits |

|

Crisis Management |

Public relations response to plan-related allegations |

Sublimits of $25K-$100K |

Standard policy limits: $1 million to $10 million, with most middle-market companies selecting $2-5 million coverage.

What’s Excluded from Coverage

Fiduciary liability insurance does not cover:

Fiduciary Liability vs. Related Coverage Types

How These Policies Differ

Coverage Type |

What It Protects |

Primary Beneficiary |

ERISA Requirement |

|---|---|---|---|

|

Fiduciary Liability |

Mismanagement of benefit plans |

Company & individual fiduciaries |

Not required |

|

ERISA Fidelity Bond |

Theft/fraud by plan handlers |

The benefit plan itself |

Required: 10% of plan assets, $1,000 minimum, $500,000 maximum |

|

Employee Benefits Liability (EBL) |

Administrative errors in plan enrollment/documentation |

Company & plan administrators |

Not required |

|

D&O Insurance |

Management decisions, shareholder lawsuits |

Directors and officers |

Not required |

Critical distinction: Most D&O policies specifically exclude coverage of fiduciary liability claims. You need standalone or integrated fiduciary coverage.

ERISA Fidelity Bonds: The Mandatory Cousin

While fiduciary liability insurance is optional, ERISA fidelity bonds are legally required for anyone handling plan funds. These bonds:

Think of it this way: ERISA bonds protect against criminals. Fiduciary liability protects against mistakes, negligence, and alleged mismanagement.

Who Faces ERISA Litigation Risk?

Company Size Doesn’t Matter

Approximately 440 out of 1,350 large plans in America (33%) have been sued for alleged excessive fees in the last eight years. For plans with assets over $1 billion, more than 50% have been sued.

But small and mid-sized businesses aren’t immune:

Litigation increasingly targets:

Why Your Personal Assets Are at Risk

Under ERISA Section 409, fiduciaries can be held “personally liable” to “make good” any losses they’re responsible for. This means:

All potentially subject to claims if you’re found liable for fiduciary breach.

Standard umbrella liability policies won’t help; they specifically exclude professional liability and fiduciary exposures.

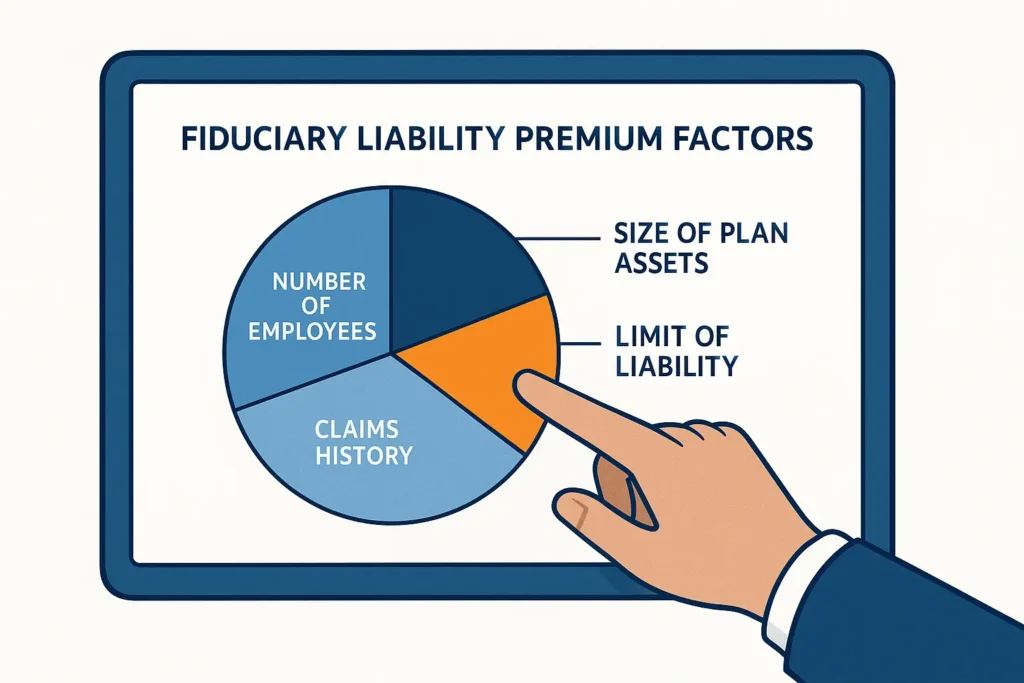

What Drives Fiduciary Liability Costs?

Premium Factors

Factor |

Impact on Premium |

How to Optimize |

|---|---|---|

|

Plan Assets |

Higher assets = higher premium |

Can’t control, but shows plan success |

|

Number of Participants |

More participants = higher exposure |

Growth is positive; maintain accurate census |

|

Plan Types |

Multiple plans (401k + health) cost more |

Bundle with single insurer for discounts |

|

Claims History |

Prior lawsuits significantly increase rates |

Implement strong governance practices |

|

Fiduciary Practices |

Documented processes reduce premiums |

Investment policy statements, committee minutes |

|

Fee Benchmarking |

Regular fee reviews show prudence |

Annual RFPs for service providers |

Typical annual premiums:

The premium represents approximately 15% of your D&O insurance premium when added as an endorsement.

Real-World Litigation Trends

The Forfeiture Lawsuit Wave

28 new forfeiture cases were filed in 2024, alleging plan fiduciaries breached their duty of loyalty by applying forfeited plan assets to future contribution obligations instead of reducing participant expenses.

These lawsuits challenge a practice explicitly permitted in most plan documents. The outcome could fundamentally change how plans handle forfeitures, and retroactively expose sponsors to liability.

Health Plan Fee Litigation Emerges

In February 2024, a newly filed class action against Johnson & Johnson’s group health plan alleged that defendants failed to demand lower prices to administer prescription drug benefits, resulting in millions of dollars in “losses” for plan participants.

This represents a new frontier, applying excessive fee theories developed in retirement plan litigation to health and welfare plans.

Pension Risk Transfer Challenges

Plaintiffs now argue that purchasing annuities to transfer pension obligations is too risky and fails ERISA’s prudence requirements, despite these transactions being widely accepted fiduciary practice for decades.

How The Coyle Group Gets It Right

We don’t just sell fiduciary liability policies. We help you avoid claims in the first place while ensuring complete protection when allegations arise.

Our Fiduciary Risk Management Approach

Assessment Phase:

Protection Phase:

Prevention Phase:

Reducing Your Fiduciary Liability Risk

Best Practices for Plan Sponsors

Governance Structure:

Fee Management:

Investment Oversight:

Participant Communication:

Third-Party Management:

Frequently Asked Questions

How can business owners minimize fiduciary liability exposure?

Implement documented governance processes including regular committee meetings, annual fee benchmarking, investment performance reviews, and periodic service provider RFPs. Work with ERISA attorneys to ensure plan documents are current and properly followed. Most importantly, purchase adequate fiduciary liability insurance since even prudent fiduciaries face litigation risk in today’s environment.

Do I need fiduciary insurance if I have an outside advisor managing investments?

Yes. Even with a §3(38) investment manager handling investment decisions, company fiduciaries remain responsible for selecting and monitoring that manager. You also retain fiduciary duties for plan administration, fee negotiation, and service provider oversight. Fiduciary liability insurance protects against claims in all these areas.

What should I do if I receive a DOL audit notice?

Contact your insurance broker immediately to determine if your fiduciary policy covers DOL investigation costs (most do via sublimits). Engage ERISA counsel before responding. The DOL typically examines plan documents, fee arrangements, investment selection processes, and fiduciary bonding compliance. Documented governance procedures significantly improve audit outcomes.

Can fiduciary insurance be paid from plan assets?

Yes, plans can pay for fiduciary liability insurance using plan assets, as the coverage protects the plan and its participants. However, many sponsors pay premiums from corporate funds. Consult your ERISA attorney on the most appropriate approach for your situation.

How does offering an ESOP affect fiduciary liability?

Plans holding employer securities face unique risks and require higher ERISA fidelity bond limits of $1 million rather than $500,000. ESOPs also face additional fiduciary scrutiny regarding stock valuation, diversification options, and conflicts of interest. Fiduciary liability premiums for ESOPs typically run 50-100% higher than traditional 401(k) plans.

What’s the difference between a claims-made and occurrence policy?

Fiduciary liability policies are claims-made, meaning the claim must be made during the policy period (or extended reporting period) regardless of when the alleged wrongful act occurred. This differs from general liability, which uses occurrence-based coverage. Understanding retroactive dates and continuity is critical when purchasing or changing fiduciary policies.

Should non-profit organizations carry fiduciary liability insurance?

Absolutely. Non-profits face the same ERISA obligations and litigation risks as for-profit companies. Non-profit board members often have limited business experience and may be particularly vulnerable to fiduciary breach claims. Protecting board members with both non-profit D&O insurance and fiduciary liability coverage is essential for recruiting and retaining quality leadership.

How quickly can fiduciary litigation escalate costs?

Defense costs for ERISA class actions frequently exceed $500,000 before reaching discovery, with total defense costs averaging $1-3 million through trial. Settlement amounts in 2024 averaged $4.6 million. These costs accumulate rapidly; having adequate coverage limits in place before claims arise is essential.

Your Next Step

If you sponsor an employee benefit plan and lack fiduciary liability insurance, you’re operating with significant uninsured exposure. Even if you have coverage, policy terms vary dramatically between carriers, ensuring your protection is comprehensive requires expert review.

We’ll review your current benefit plans, identify fiduciary exposures, and provide competitive quotes from multiple carriers.

About the Author

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the United States, solving their insurance challenges. Gordon specializes in helping companies develop comprehensive management liability programs including fiduciary liability, D&O, EPLI, and cyber insurance that protect their operations and support their growth objectives.