SaaS Insurance for Software Companies

Get Contract-Ready for Tech Risks

SaaS Insurance Explained in 5 Minutes

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

Close deals faster and sleep better, get limits that satisfy MSAs and investors.

SaaS insurance isn’t a single policy; it’s a coordinated program designed to respond when software failures, data incidents, or board decisions create financial loss.

If a software bug, outage, or breach hits today, would your policy actually respond? Get a contract-ready SaaS insurance program built around your risks.

The Bottom Line – TL;DR

What do SaaS companies need?

A well-structured SaaS insurance program coordinates multiple policies, so coverage responds correctly when software, data, or contracts create financial loss.

Unlike general business insurance, SaaS risk lives in your code, your contracts, and your uptime obligations, not your physical premises. Each policy in the stack covers a different failure mode, and gaps between them are where most claims disputes start.

The Coverage Stack

Real Scenarios → Which Policy Responds

The gap

According to the National Association of Insurance Commissioners (NAIC), General Liability covers physical risks, injuries, and property damage. It specifically excludes professional services, data breaches, and software failures. That’s 100% of your actual exposure as a SaaS company.

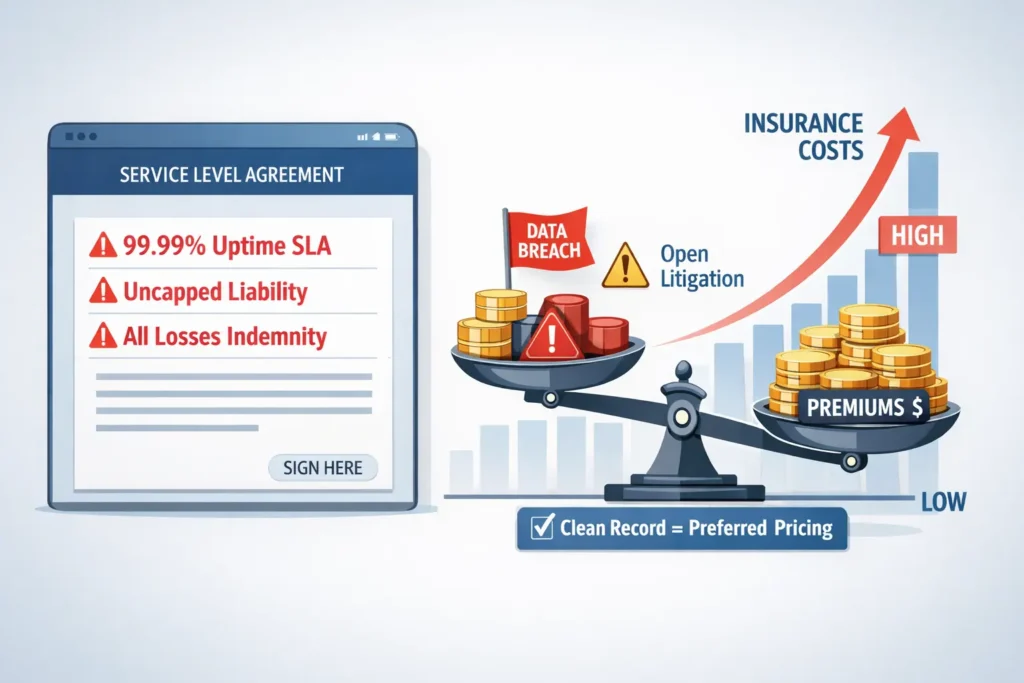

SaaS Insurance Pricing: What Drives Your Cost

SaaS insurance pricing reflects your revenue, data sensitivity, security controls, and SLA commitments, not just your company size. Two SaaS companies at the same ARR can see 2x to 3x premium differences based on controls and contract language alone. The four factors below explain what underwriters actually weigh.

The Big Four Cost Factors

1. Revenue & Data Sensitivity

2. Security Controls (Biggest Lever You Control)

3. Service Level Agreements

4. Claims History

Typical Monthly Bundles

The gap without controls:

If you lack MFA, tested backups, or endpoint detection/response (EDR), we regularly see premium surcharges of 50–100% or outright coverage denial.

Real-World Example: When API Dependencies Fail

The Incident

A cloud HR platform integrated with a payroll processing API. During a critical pay period, the API went down for 14 hours. Their clients couldn’t process payroll.

Client Losses:

Business Impact:

How Insurance Responded

Why SaaS Insurance Is a Decision, Not a Form

Most SaaS founders assume insurance is about checking boxes:

MFA? Yes. Backups? Yes. Policy in place? Done.

But insurance doesn’t fail because a form was filled out incorrectly.

It fails because the coverage wasn’t designed to match how the business actually operates.

Underwriters don’t just look at controls. They look at:

That’s why two SaaS companies with identical security controls can get very different coverage outcomes.

What 40+ Years Taught Me. The best SaaS insurance programs aren’t the ones with the longest checklists. They’re the ones where coverage, contracts, and operations tell the same story.

That’s what prevents disputes when a claim happens.

How SaaS Insurance Breaks and How We Prevent It

Most SaaS companies don’t get hurt because they skipped insurance.

They get hurt because their coverage wasn’t built for how SaaS risk actually works. Policies that weren’t designed for your revenue model, your vendor dependencies, or your contract language create gaps that only surface at claim time, when it’s too late to fix them.

Here’s where things usually break:

By the time founders discover these gaps, the damage is already done.

What we do differently:

We design coordinated SaaS insurance programs, Tech E&O, Cyber, D&O, and Crime, that align with your revenue model, your contracts, and your dependencies. No gray areas. No finger-pointing between carriers. Just coverage that works when it matters.

What 40+ Years Taught Me About This Risk. Price doesn’t take down SaaS companies, coverage gaps do.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

Questions about SaaS Insurance?

Get the Right Coverage for Your SaaS Company

Most SaaS insurance programs fail because they’re built like small-business policies, not technology risk strategies. When claims involve downtime, data, or board decisions, that difference matters.

We work exclusively with SaaS and technology companies, from pre-revenue startups to publicly traded software firms, structuring insurance programs that hold up under client scrutiny, investor diligence, and real claims.

If you want clarity on whether your current coverage actually protects your revenue and contracts, the next step is simple.

On a 15-minute call, you’ll get:

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping SaaS and technology companies develop comprehensive insurance programs that protect their operations, satisfy investor and client requirements, and support their growth objectives.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

Tech E&O vs. Cyber Insurance: What You Need to Know

Life Sciences – Business Interruption Insurance

What is Clinical Trails Insurance