Fintech Insurance

Contract-Ready Coverage for High-Stakes Financial Risk

How To Get The Right Insurance For Fintech Companies

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Your fintech insurance demands strategic attention:

TL;DR – The Bottom Line

Protect customer funds, data, uptime, and leadership coverage built to satisfy banks, partners, and investors.

Typical starting range (early-stage):

$3,000–$10,000/year for a basic stack. Bank-partner and regulated models often run higher.

Fintech Insurance Stack at a Glance

Coverage |

What It Covers |

Why Fintechs Need It |

Common Exclusions/Gotchas |

|---|---|---|---|

|

E&O / Professional Liability |

Errors in services, processing mistakes, platform failures, negligence claims |

Payments errors, settlement delays, incorrect funds movement, advice exposure |

Uncapped indemnity in contracts, intentional acts, criminal conduct |

|

Cyber Liability |

Breach response, extortion, incident response, privacy liability, business interruption |

Data protection obligations, ransomware attacks, vendor outage losses |

Waiting periods for dependent BI, insider threats, infrastructure failure without cyber event |

|

Crime / Fidelity Bond (crime insurance with bonding language when required) |

Social engineering, funds transfer fraud, employee dishonesty, computer fraud |

Money movement protection, wire transfer fraud, account takeover |

Voluntary parting exclusion, losses from unauthorized employees, indirect losses |

|

D&O |

Investor/board claims, mismanagement allegations, regulatory investigation defense |

Fundraising protection, board seat requirements, insolvency claims |

Illegal acts, prior knowledge, insured vs insured disputes |

|

General Liability |

Premises liability, advertising injury |

Contract requirements, basic business operations |

Professional services, cyber events, contractual liability |

Why Fintech Insurance Is Different

Standard small-business policies fail fintechs because they don’t account for the unique intersection of technology and financial services. The result is a coverage stack that looks nothing like standard small-business insurance, and a policy review process that requires understanding your business model, not just your industry.

Fintech companies face exposures that traditional policies weren’t designed to cover:

According to the Federal Deposit Insurance Corporation, FDIC deposit insurance doesn’t protect against the insolvency or bankruptcy of a nonbank company, creating additional liability concerns for fintech platforms that facilitate banking services.

Critical Fork: Are You Custodying Funds or Just Facilitating?

This distinction dramatically changes your insurance requirements:

Why it matters

Banking partners and underwriters price and structure coverage differently based on whether you actually hold customer funds versus simply connecting parties. Misrepresenting your model creates coverage gaps.

What 40+ Years Taught Me About This Risk

The companies that win with insurance treat it as an enablement tool: coverage that closes deals and survives claims.

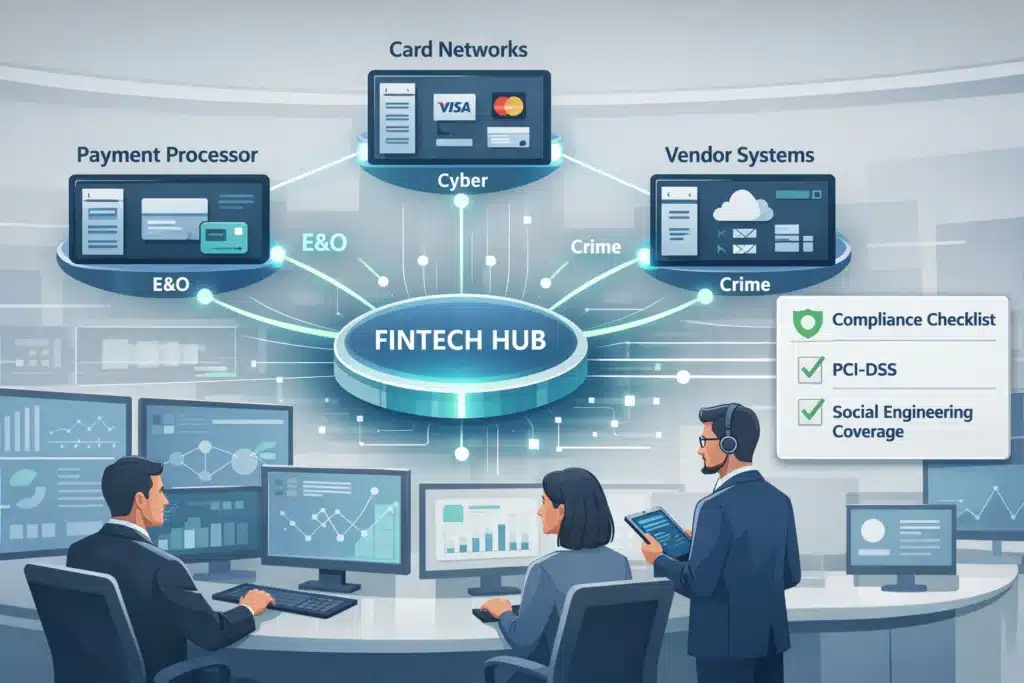

The Fintech Coverage Stack

The right fintech coverage stack depends on whether you custody funds, facilitate transactions, provide financial advice, or build infrastructure. The policies below are the core building blocks, not every fintech needs all of them, but most need at least three working in coordination.

Financial Services E&O / Tech E&O (Professional Liability)

Professional liability insurance addresses errors in your services, processing mistakes, platform failures, and negligence claims. For fintechs, this means protection when your technology or financial services cause customer financial loss.

What it covers:

Fintech-specific considerations:

The distinction between technology E&O and financial services E&O matters. Technology E&O covers failures of products to perform as intended, while financial services E&O addresses errors in providing financial advice or services. Many fintechs need both, or a blended policy that addresses the intersection of tech failures and financial service errors.

Service Level Agreement (SLA) and indemnity language in your contracts can become uninsurable if not carefully managed. Uncapped indemnity provisions-common in enterprise agreements-may fall outside your E&O coverage entirely.

Illustrative Example

A growth-stage fintech launched an investment platform allowing users to trade through a mobile app. A software bug prevented transactions during a multi-hour period. Lawsuits alleged wrongful interference with trading activity. The E&O policy covered defense costs up to policy limits, with the case ultimately settling after early motion to dismiss.

Cyber Liability (First-Party + Third-Party)

Cyber insurance provides crucial protection for data breaches, ransomware attacks, and privacy violations-risks that grow as your platform scales.

Coverage components:

Critical fintech-specific issues:

According to the National Association of Insurance Commissioners, cyber policies are highly customized and standard GL/property policies don’t cover cyber risks. This makes proper policy selection essential rather than optional.

Waiting periods

Create gaps in dependent business interruption coverage. If your payment processor experiences an outage, you may face a 6-12 hour waiting period before coverage kicks in. For high-transaction-volume fintechs, that window can represent significant revenue loss.

Panel vendors / consent requirements

Means you can’t always choose your incident response team. Many policies require using pre-approved vendors for forensics and breach response, which can slow your response time or conflict with your existing security relationships.

Must-discuss subtopics:

Understanding first-party vs. third-party cyber coverages helps you evaluate whether your policy truly protects your business model.

Crime Insurance / Fidelity Bond (The “Money Movement” Protection)

Crime insurance protects against social engineering, funds transfer fraud, employee dishonesty, and computer fraud. For fintechs handling customer funds or facilitating transactions, this coverage is non-negotiable.

What it covers:

According to AIG’s Crime and Fidelity Claims Intelligence Report, social engineering fraud is now the #1 source of crime insurance losses, surpassing traditional employee dishonesty. Organizations with less than $99 million in revenue account for over half of all claims.

When “fidelity bond” is specifically required:

Broker-dealers and certain regulated models face explicit bonding rules. FINRA Rule 4360 requires member firms to maintain fidelity bond coverage with minimum amounts based on securities and funds under custody.

Cyber vs. Crime vs. E&O: Which One Pays When Money Moves?

Scenario |

E&O Response |

Cyber Response |

Crime Response |

|---|---|---|---|

|

Software bug causes incorrect fund transfer |

✅ Covers client financial loss |

❌ Not a cyber event |

❌ Not fraud/theft |

|

Ransomware demands payment |

❌ Not professional services |

✅ Extortion coverage |

⚠️ May have sublimit |

|

Employee embezzles customer funds |

❌ Not negligence |

❌ Not data breach |

✅ Employee dishonesty |

|

Fake CEO email authorizes wire transfer |

❌ Not services error |

✅ Business Email Compromise (BEC) |

✅ Social engineering |

|

Vendor outage causes revenue loss |

⚠️ If contractual liability |

✅ Dependent Business Interruption (after waiting period) |

❌ Not crime |

|

Hacker transfers customer funds |

❌ Not professional error |

✅ If unauthorized access |

✅ Computer fraud (with endorsement) |

The key difference

E&O covers your mistakes, cyber covers attacks, crime covers theft and fraud. Many losses involve overlapping exposures, which is why proper policy coordination matters.

Learn more about cyber insurance versus crime insurance to understand both coverage types.

D&O (Directors & Officers)

Directors and Officers liability insurance protects leadership when they’re sued over management decisions, offering crucial protection for fintech executives navigating regulatory scrutiny and investor pressure.

What it covers

Why fintechs need D&O

In regulated models, the chance of regulatory scrutiny and investor claims is higher – which is why D&O limits tend to climb quickly after Series A. D&O is often required by VC/PE term sheets before funding closes-investors want their board representatives protected.

Coverage triggers for fintechs

Typical limits by stage

Supporting Policies (Only If Relevant)

Insurance by Fintech Type: How Your Business Model Drives Coverage

Fintech insurance isn’t one-size-fits-all; your business model determines your primary exposures. A payments company faces different risks than a robo-advisor or a crypto exchange. The table below maps the four core fintech sub-sectors to their primary coverage needs and key regulatory bodies.

Fintech Type |

Business Examples |

Primary Exposures |

Core Coverage |

Key Regulators |

|---|---|---|---|---|

|

Payments / Transfers |

ACH processors, digital wallets, money transmitters |

Wire fraud, social engineering, funds movement errors |

Crime (high limits), Cyber, E&O |

FinCEN, state money transmitter licenses |

|

Lending / Credit |

Online lenders, BNPL, marketplace lending |

Processing errors, regulatory enforcement, data privacy |

E&O, Cyber, D&O |

CFPB, state banking departments |

|

Wealthtech / Robo-Advisors |

Investment platforms, trading apps, robo-advisors |

Advice errors, fiduciary claims, algorithm failures |

E&O (financial services), D&O |

SEC, FINRA |

|

Crypto / Digital Assets |

Exchanges, custodians, token issuers, DeFi |

Digital asset theft, token launch liability, key loss |

E&O (E&S carriers), D&O, Crime with digital asset endorsement |

SEC, CFTC, state regulators |

Contract-Ready: What Partners, Banks, and Investors Actually Ask For

Contract-ready means your coverage limits, endorsements, and policy wording match your actual agreements. Without this alignment, you’ll face delays closing deals or discover gaps mid-contract.

Contract-ready = limits + endorsements + wording that matches your agreements.

Partner Requirements by Type

1. Bank/BaaS Partner / Sponsor Bank

Banking partners impose the strictest insurance requirements because they bear regulatory liability for your actions.

Typical requirements:

Special considerations:

2. Payment Processor / Card Programs / Vendors

Typical requirements:

3. Enterprise Clients + MSAs

Common requirement list:

Contract Clauses That Blow Up Coverage

Certain contract provisions create uninsurable liability. Review these carefully before signing:

Pricing: What Drives Fintech Insurance Cost

Fintech insurance costs vary based on your business model, transaction volume, data handling, and security controls. There’s no one-size-fits-all premium, but understanding cost drivers helps you budget accurately.

The variables below explain why two fintechs at the same revenue level can pay dramatically different premiums, and what you can control to improve your position.

Pricing Drivers

Factor Category |

Impact on Premium |

Optimization Strategy |

|---|---|---|

|

Annual Revenue + Transaction Volume |

Higher revenue = higher premium |

Bundle coverages for multi-policy discounts |

|

Funds Flow Model |

Custody vs pass-through vs facilitation affects crime/E&O pricing |

Document your actual role in fund movement |

|

Data Types |

NPI/PII/PCI data, geography (international = higher) |

Demonstrate robust data governance |

|

Controls |

MFA, EDR/MDR, wire approval processes, dual control |

Implement and document controls before renewal |

|

Claims History + Incidents |

Prior claims increase rates significantly |

Proactive risk management reduces frequency |

|

Vendor Dependency |

Heavy reliance on third parties increases cyber/BI risk |

Vendor management program + SLA documentation |

According to Secureframe’s analysis, premiums for fintech companies often start in the $5,000–$10,000 per year range for younger startups, with larger or more heavily regulated fintechs paying $15,000–$20,000+ per year.

Typical Packages by Stage

Stage |

Annual Premium Range |

Coverage Stack |

Notes |

|---|---|---|---|

|

Pre-Revenue / Seed |

$3,000–$8,000 |

E&O ($1M), Cyber ($1M), D&O ($1M–$2M) |

Light underwriting, higher deductibles acceptable |

|

Growth (Series A/B) |

$8,000–$25,000 |

E&O ($2M–$5M), Cyber ($2M–$5M), Crime ($1M–$2M), D&O ($2M–$5M) |

Partner requirements drive limits |

|

Scale (Series C+) |

$25,000–$75,000+ |

Full stack with higher limits across all lines |

Complex risk profile, multiple carrier layers |

|

Regulated Model |

$50,000–$150,000+ |

Enhanced limits + regulatory coverage endorsements |

BD/RIA/crypto face premium increases |

Cost Levers You Control

Control |

Underwriter Impact |

Claim Impact |

Implementation Effort |

|---|---|---|---|

|

Multi-Factor Authentication |

Required by most carriers |

Prevents 99.9% of account attacks |

Medium – requires rollout across systems |

|

EDR/MDR Deployment |

Often improves terms (and can reduce premiums) in many markets |

Early threat detection |

Medium – ongoing monitoring required |

|

Wire Transfer Dual Approval |

Crime premium reduction |

Prevents social engineering |

Low – policy/procedure change |

|

Security Awareness Training |

Cyber underwriting credit |

Reduces human error (95% of breaches) |

Low – quarterly training sessions |

|

Vendor Risk Management |

E&O/cyber credits |

Third-party incident prevention |

High – requires ongoing assessment |

|

Incident Response Plan (tested) |

Required for coverage |

Faster recovery = lower losses |

Medium – annual tabletop exercises |

Real-World Scenarios

The four scenarios below map common fintech losses to the specific policy that should respond, and the gotchas that determine whether a claim actually gets paid. Each involves overlapping exposures across E&O, cyber, and crime, which is where most coverage gaps live.

Scenario A: Social Engineering / Fraudulent Wire

What happened

The finance team received an email appearing to be from the CEO requesting an urgent wire transfer to a “new vendor account” for $250,000. Email was sophisticated, had a proper signature, and referenced a real internal project.

The loss:

Which policy should respond

Crime insurance with social engineering coverage.

The gotcha

Many crime policies have “voluntary parting exclusion”-if the employee knowingly authorized the transfer (even if deceived), coverage may be denied. Policies with explicit social engineering endorsements cover this exposure. Additionally, some policies require “out-of-band” verification (confirming requests through separate communication channel) as a condition of coverage.

Scenario B: Vendor Outage Causes Revenue Loss + Breach Allegations

What happened

Payment processor experienced an 18-hour outage. Your platform couldn’t process transactions. During the outage, breach notification indicated potential data exposure.

The loss:

Which policy should respond

Cyber policy’s dependent business interruption coverage + third-party privacy liability.

The gotcha

Most cyber policies have 6-12 hour waiting periods for dependent BI. The first 6-12 hours of outage losses aren’t covered. Additionally, if the breach resulted from your vendor’s security failure (not yours), coverage may be limited or excluded.

Scenario C: Processing Error Triggers Client Financial Loss

What happened

A software update introduced a bug in your lending platform’s interest calculation. Over 30 days, 500 customers were overcharged by an average of $300 each ($150,000 total).

The loss

Which policy should respond

E&O insurance.

The gotcha

If your services agreement included a limitation of liability clause capping damages at fees paid, but you agreed to indemnify for regulatory violations, the indemnification may fall outside your E&O policy. Many E&O policies exclude regulatory fines (though defense costs may be covered).

Scenario D: Regulatory Inquiry After Incident

What happened

State AG opened an investigation into your data security practices following a phishing attack that exposed customer information. Investigation requires substantial legal response and potential remediation requirements.

The loss

Which policy should respond

Cyber policy’s regulatory defense coverage + D&O (for individual officer liability).

The gotcha

Not all cyber policies cover regulatory fines; many exclude fines but cover defense costs. D&O policies often include regulatory investigation coverage for individual directors/officers, but may exclude entity-level fines. The interplay between cyber and D&O creates coverage gaps if not properly coordinated.

Questions about Fintech Insurance?

Your Next Step: Stop Guessing, Start Protecting

The risk isn’t buying insurance. It’s buying the wrong kind.

Most fintechs discover coverage gaps during a partnership negotiation, a funding round, or after a claim. By then, it’s too late to fix it affordably.

What You Get on the Call

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping fintech companies, technology firms, and financial services businesses develop comprehensive insurance programs that protect their operations while satisfying partner and investor requirements.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

Tech E&O vs. Cyber Insurance: What You Need to Know

Life Sciences – Business Interruption Insurance

What is Clinical Trails Insurance