What Is a D&O Tail Policy?

Protecting Your Business From Costly Risks

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

The Bottom Line. TL;DR

You sold your company. You have a merger agreement with an indemnification clause. The buyer has D&O coverage. You assume you’re protected.

Eighteen months later, a lawsuit arrives for decisions you made two years before the sale. Your carrier says there’s no coverage. The buyer’s policy doesn’t apply. The indemnification agreement is being disputed.

That’s not a hypothetical. It’s the most predictable outcome when directors skip a tail policy at the exact moment they become the most financially attractive targets.

Two assumptions cause this gap almost every time:

A properly placed tail policy converts six years of personal exposure into covered, non-cancelable protection regardless of what the buyer does next.

Not sure if your situation requires a tail? Contact us for a no-pressure assessment.

What Is a D&O Tail Policy?

A D&O tail policy, officially called an Extended Reporting Period or ERP, is a one-time purchase that extends a company’s ability to report claims to their D&O policy after it’s terminated, for acts that happened while the original policy was in force.

Because D&O insurance is written on a claims-made policy form, it requires that an active policy or a tail be in effect to cover claims when they are made or presented to the insurer. When a policy is terminated without a tail, any claims reported after termination will not be covered.

Here’s an example:

Your company is merged, sold, or acquired on July 1st. You had D&O insurance and do nothing, assuming prior acts are covered past the termination date. The policy has a provision that terminates coverage upon a change in control, meaning 51% or more of the stock changes hands. In October, a shareholder files a lawsuit over a decision the CEO made back in March, when the policy was in force. You present the claim to your insurer, thinking you have coverage. It’s denied. Why? Because coverage terminated, and no tail was purchased.

D&O insurance is written on a claims-made basis, meaning the policy that responds is the one in place when the claim is filed, not when the act occurred. If your policy terminates before a claim is filed, there is nothing to respond. An occurrence-based policy (like general liability) covers the act whenever the claim surfaces. A claims-made policy does not. The tail bridges that gap.

What a tail covers:

What a tail does not cover:

One practical advantage worth noting

A properly purchased tail is non-cancelable. Once it’s in place, the buyer cannot unwind it to recover the premium. That matters more than most directors realize when the post-close relationship sours.

What Events Trigger the Need for a D&O Tail Policy?

The most common trigger is a merger or acquisition, but any event that terminates a claims-made D&O policy while past acts remain unresolved creates the same exposure. Company wind-downs, policy non-renewals, executive departures, and dissolution all open the same gap, and most directors never see them as coverage events until it’s too late.

M&A gets all the attention. The scenarios that actually catch directors off guard are the quieter ones: a non-renewal notice, a wind-down after a fund closes, a board departure that nobody flagged as a coverage event.

The common thread

In every scenario above, a claims-made policy terminates while the window for potential claims remains open. Statutes of limitations on fiduciary and securities claims can run three to six years. The policy gap and the legal exposure don’t close at the same time. For a deeper look at what happens to your D&O coverage when ownership changes, see our breakdown of D&O change in control provisions.

Doesn’t the Buyer’s D&O Policy or the Merger Agreement Cover Me?

No, on both counts. The buyer’s D&O policy covers the new entity’s directors for post-close decisions only. It does not reach back to cover the selling company’s former directors for pre-close acts. And while a merger agreement’s indemnification clause sounds like protection, it is only as reliable as the buyer’s future financial health and willingness to honor it.

Now, what if you had an indemnification clause in your merger agreement and the buyer had D&O insurance? Would you have protection then?

No. The buyer’s policy will not apply for two reasons:

Here’s how the timing works in practice. A decision is made in Year 1. The company sells in Year 3. A claim is filed in Year 4. The policy that responds is the one in place in Year 4. The seller’s original policy lapsed at closing. The buyer’s policy covers Year 3 onward for the buyer’s directors. The former directors have nothing unless a tail was purchased at close.

The table below shows how each scenario plays out when a claim arrives after closing, and where a D&O tail policy is the only option that holds.

A note on “clean” deals

The transactions that feel uneventful are exactly the ones where plaintiffs wait. A liquidity event is public. Former employees, competitors, and shareholders now know there is a payday, and statutes of limitations give them years to file. The quiet period after a sale is not evidence that no claims are coming. It is simply the interval before they surface.

Facing a transaction or change in control?

Before assuming you’re covered.

What Is a Naked Tail D&O Policy?

A naked tail is a D&O tail policy purchased by a company that never carried D&O insurance before the transaction. It’s common in private company M&A where owners operated for years without D&O coverage, then face a contractual requirement from the buyer at closing. Naked tails are now widely available, but the window to obtain one is tight, and the underwriting process differs from a standard tail.

Most private company sellers don’t learn this is a requirement until they’re three or four weeks from closing. By then, underwriting options narrow, and there is no time to shop the market properly.

How naked tail underwriting works:

The non-negotiable:

This must be placed before or at closing. Once the transaction closes without a tail in place, the window is gone. There is no retroactive option.

How Much Does a D&O Tail Policy Cost?

D&O tail premiums typically run 100%-300% of the annual D&O premium, paid upfront in a lump sum and non-refundable. For most private middle-market companies, a 6-year tail costs $20,000-$50,000. Larger or higher-risk companies can face multi-million dollar premiums. The cost is almost always negotiable, but only before the transaction closes. That calculation is why most sellers who understand the exposure view the D&O tail policy premium not as a cost but as a transaction line item.

Key cost drivers:

On the “too expensive” objection: a single uncovered D&O claim runs $100,000-$500,000+ in defense costs alone, before any settlement. A 6-year tail for a mid-market company costs a fraction of that. The question isn’t whether you can afford the tail. It’s whether you can afford to personally fund your own defense for six years after the sale closes.

Need a tail cost estimate before negotiations close?

What Happens If You Miss the Tail Election Window?

If you miss the window to elect tail coverage, typically at or before the closing date, the option is gone permanently. There is no retroactive fix. Former directors and officers are personally exposed for any claim that surfaces after the policy terminates, with no insurance backstop and no way to recover the coverage after the fact.

It is not a soft deadline. When the window closes, it closes for good. Lawsuits don’t follow a convenient timeline.

Standard election window

most policies require tail election at or before the closing date. Some carriers allow a short post-termination window, typically 30-60 days, but this varies by carrier and policy language and cannot be assumed. Verify before closing, not after.

A Real-World Consequence

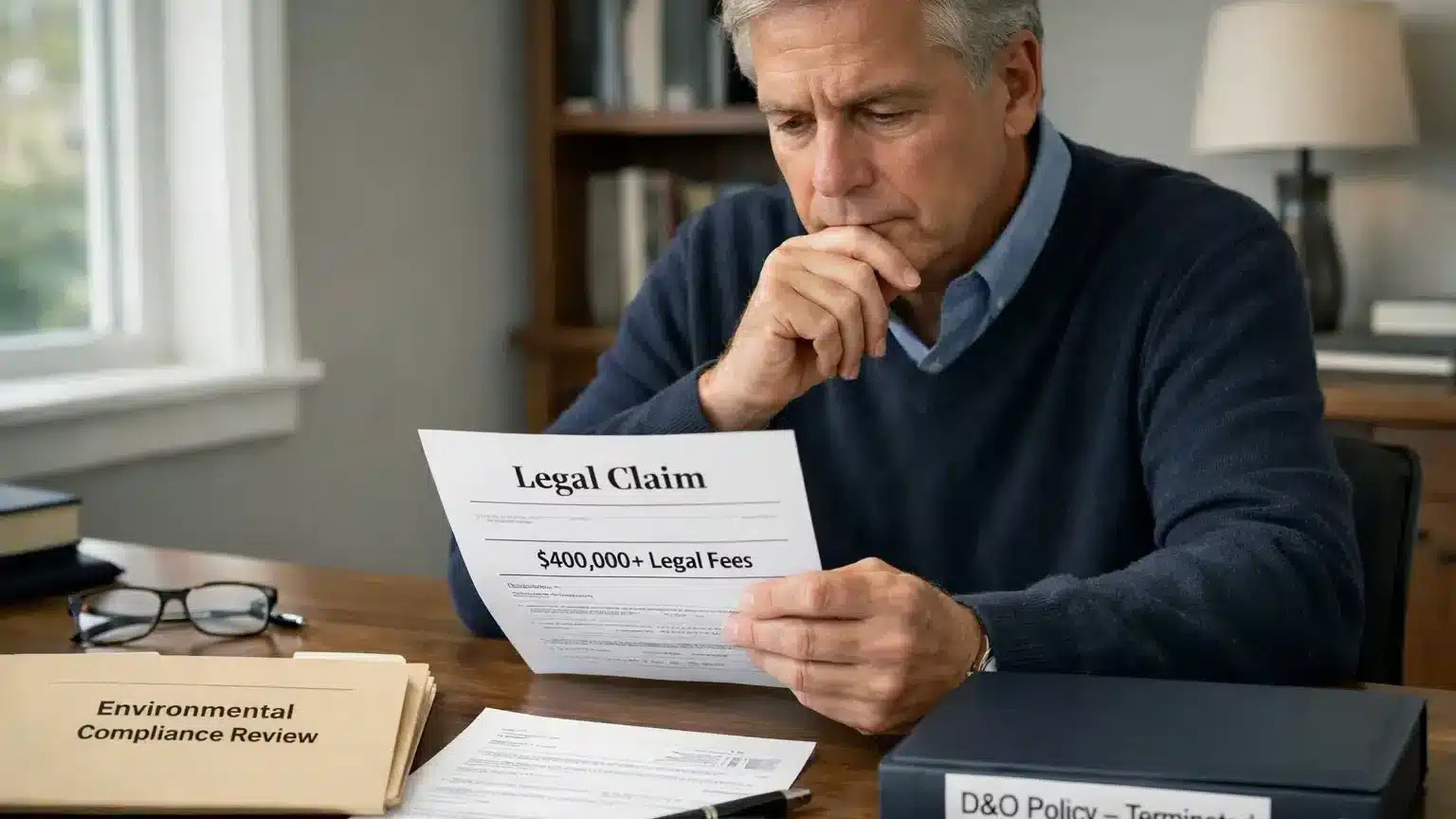

A manufacturing company was sold to a private equity buyer in 2022. The seller’s directors and officers assumed they were protected because the buyer purchased new D&O coverage.

Eighteen months post-close, the buyer discovered environmental compliance issues dating back three years and filed claims against the former directors for misrepresentation during due diligence.

The former directors had canceled their original policy at closing without purchasing a tail. The buyer’s new policy did not cover pre-acquisition acts. Legal defense costs exceeded $400,000, paid personally by the directors.

The Straddle Claim Trap

One post-close coverage risk that almost no one plans for: the straddle claim.

A straddle claim alleges misconduct spanning both before and after the tail’s effective date. Many tail policies include exclusions that bar coverage for any claim touching post-close conduct, even when part of the alleged wrongdoing is pre-close. This is one of the most frequently litigated coverage disputes following acquisitions.

Reviewing the D&O tail policy exclusions before placement, not after a claim, is the only way to know where you actually stand. Hunton Andrews Kurth’s breakdown of coverage cutoffs in M&A transactions covers the straddle claim exclusion and four other common post-close traps in detail, worth reading before placing any tail.

The seller should always place the tail, not the buyer. The broker who places the tail typically manages all future claims under it. That relationship should belong to the people whose personal assets are protected by the policy.

Should You Also Buy EPLI and Fiduciary Tail Policies at Closing?

In most transactions, yes. EPLI and Fiduciary Liability policies are also written on a claims-made basis.

If terminated at closing without a tail, the same coverage gap opens. Employment claims, wrongful termination, discrimination, and harassment routinely surface months or years after a transaction, especially when the buyer restructures the workforce post-close.

A D&O tail without an EPLI tail is a partial solution.

The exposure it leaves open is one of the most frequently filed post-close claim types.

Covering all your claims-made exposures at close?

Questions About D&O Tail Policies?

How The Coyle Group Approaches D&O Tail Coverage

We have guided directors and officers through hundreds of transactions, leadership changes, and wind-downs. We know what sellers miss, what buyers push for, and where the gaps turn into six-figure personal exposure. Our job is not to sell you a policy. It is to make sure you understand exactly what you are and are not covered for through the close and for the six years that follow it.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

Tell us where you are in the transaction and we’ll map out exactly what you need.

This article was written by the CEO of The Coyle Group, Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

Protecting Non-Profit Board Members with D&O Insurance

Rippling PEO Review: EPLI Coverage Risks Explained

The Ultimate Guide to D&O Insurance: Everything You Need to Know in 2025