Search Fund Insurance

Complete Coverage Guide from Due Diligence to Day 1

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

You’ve found your target company. You’re in due diligence. Your lender sends the insurance requirements list and you start reviewing the seller’s program. That’s when you discover gaps, expired policies, and claim issues that should have been flagged earlier.

The Hidden Villains: Coverage gaps that delay closing, claims-made policies with pre-close tail exposure, and missing personal protection that puts your assets at risk the day you become CEO.

This guide walks you through search fund insurance assessment during diligence, what you need to close on time, and Day 1 coverage that protects you personally as the new CEO.

The Bottom Line. TL;DR

Search fund insurance protects across three critical phases:

Success looks like

Close on time, lender-ready COIs delivered, personal assets protected from Day 1, no surprise gaps discovered post-close.

Failure looks like

Closing delays, uninsured claims-made gaps creating personal exposure, employment claims with no EPLI, cyber attacks with inadequate coverage.

Not sure where your deal stands on insurance?

What is search fund insurance?

Definition & Core Purpose

Search fund insurance refers to coverage needed across three phases: (1) D&O protection during your search, (2) insurance due diligence on target companies, and (3) comprehensive business insurance you bind at closing to operate as CEO.

The term covers multiple stages of your acquisition journey:

Phase 1: Search Phase (Optional)

Phase 2: Due Diligence Phase (Critical)

Phase 3: Acquisition & Operations (Required)

This isn’t one policy. It’s a strategic stack that protects investors, satisfies lenders, and shields you personally from lawsuits. The distinction matters because each phase has different priorities, timing, and costs.

What 40+ Years Taught Me About This Risk

In four decades placing commercial insurance for business acquisitions and middle-market companies, the pattern is clear: buyers who treat insurance as a last-minute checkbox discover problems when it’s too late to fix them. The successful ones start due diligence early, use insurance analysis to negotiate better deals, and bind comprehensive coverage that protects them personally as CEO.

Insurance isn’t just a lender requirement. It’s one of your first chances to understand how the business was really managed.

Do I need insurance during the search phase before I buy a company?

Most searchers don’t carry insurance during search, but if you have investor board members or provide advisory services to potential targets, D&O insurance for the search fund entity protects against claims from investors or deal parties.

Typical Cost

Often starts with a minimum premium around $12,000 to $25,000 annually for $5 million D&O coverage during search phase, though pricing varies significantly by market conditions, investor profile, and entity structure.

Most Common Approach

Skip search phase D&O unless investors require it. Focus resources on finding and analyzing deals instead.

Why does insurance due diligence matter before I sign an LOI?

Insurance due diligence reveals hidden risks through loss history, coverage gaps, and claims trends that can influence valuation negotiations, deal structure decisions, and post-close cost planning helping searchers identify material issues before committing to a deal.

Loss runs tell the story that financials don’t. Insurance claims reveal operational issues, management problems, and uninsured exposures that directly impact business value.

A manufacturer with clean financials but 15 workers comp claims in 3 years signals serious safety culture problems. A restaurant with 3 liquor liability claims suggests inadequate training and oversight. These patterns predict future costs and risks that aren’t visible in P&L statements.

This type of review, analyzing loss history, identifying coverage gaps, and arranging run-off for claims-made policies, is what The Coyle Group formally offers as a Risk Diligence Service. It’s a fee-based consulting engagement available to search fund buyers and PE acquirers before they commit to a deal. The deliverable is a clear picture of what the target’s insurance program looks like, what needs to change at close, and what tail or run-off coverage the seller needs to maintain.

What You’re Looking For

How This Affects Deal Value

Scenario 1: Workers Comp Frequency Issue

Potential Negotiation Options:

Scenario 2: Missing Critical Coverage

Critical Claims-Made Policy Issues

The Problem:

The Solution

Negotiate prior acts coverage or require seller to maintain tail coverage. Factor the cost into purchase price.

Tail Coverage Cost:

For a business paying $25,000 annually for management liability, tail coverage could cost $50,000 to $75,000. This is often a legitimate topic for purchase price negotiations.

What are the biggest insurance mistakes search fund buyers make?

The three deadliest mistakes are: (1) waiting until 2 weeks before close to start insurance, (2) assuming the seller’s program continues post-close, and (3) not getting personal CEO protection (D&O, EPLI, Cyber).

These mistakes are avoidable with the right broker in your corner early.

Real-World Consequences

Mistake #1 Example: The 2-Week Scramble

A searcher waited until 14 days before close to start insurance. The target was a 45-employee manufacturing company with fleet vehicles.

Result:

Mistake #2 Example: The Coverage Gap

Searcher assumed seller’s cyber insurance would provide coverage continuity. Seller had claims-made cyber policy with 3-year retro date. Ransomware attack 6 weeks post-close revealed vulnerability from 2 years prior.

Result:

What should have happened: Negotiated prior acts coverage or required seller maintain tail coverage, which would have cost a fraction of the potential exposure.

Mistake #3 Example: No D&O Protection

New CEO terminated plant manager 90 days post-close for performance issues. Manager filed age discrimination lawsuit naming CEO personally.

Result:

The cost of the coverage is minimal compared to potential personal exposure from just one employment claim.

What insurance do lenders require to close a search fund acquisition?

SBA and commercial lenders typically require: General Liability ($1 million to $2 million), Workers’ Compensation (if employees), Commercial Auto (if vehicles), Property insurance (if real estate), and Umbrella coverage ($1 million to $5 million), with lender listed as loss payee and additional insured.

Standard Lender Requirements

Cyber Insurance:

According to the SBA, lenders determine insurance requirements based on collateral type and business operations.

What Lenders Don’t Require (But You Need)

Critical Gap:

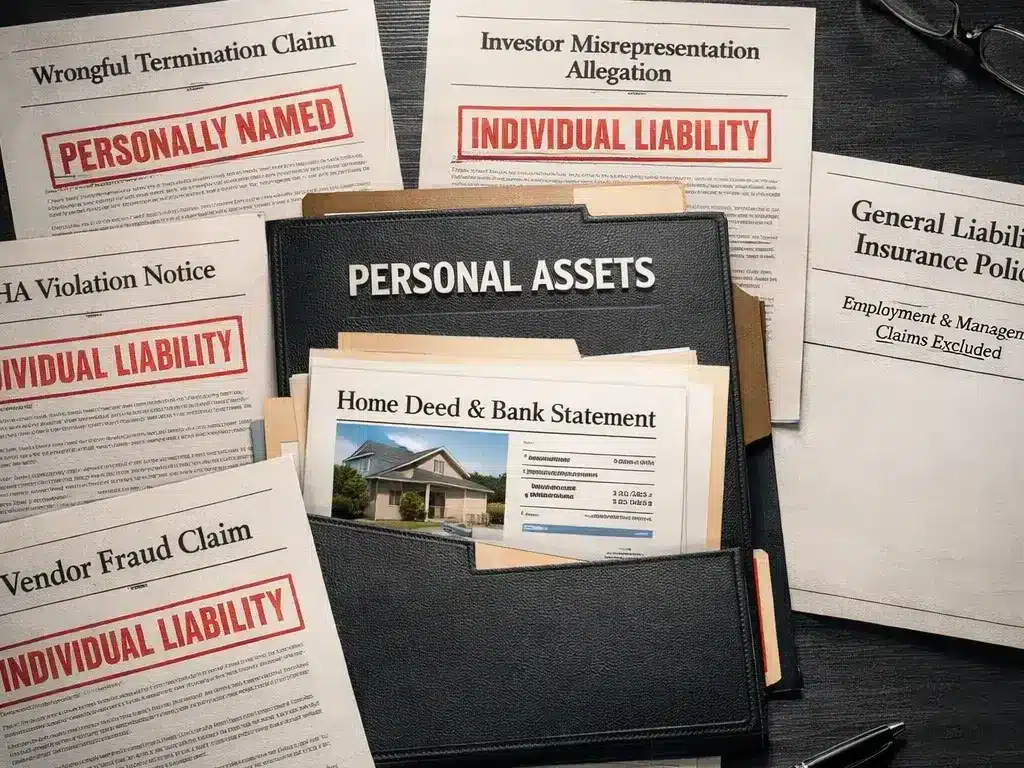

What insurance protects me personally as the new CEO and owner?

D&O (Directors & Officers) insurance, EPLI (Employment Practices Liability), and Fiduciary Liability protect you personally from lawsuits related to management decisions, employment claims, and 401(k) administration coverage that the company’s general liability policy excludes.

Common Personal Liability Scenarios:

In each case, you’re named personally. Your personal assets are at risk. General liability won’t help.

The Personal Protection Stack

D&O / Management Liability Insurance

Coverage

$1 million to $5 million

Protects Against:

Annual Cost

$3,000 to $15,000 depending on revenue and industry

Small businesses typically pay $1,650 to $2,500 annually for basic D&O coverage, with costs increasing based on revenue, industry risk, and coverage limits.

EPLI (Employment Practices Liability Insurance)

Coverage

$1 million to $2 million

Protects Against:

Why It Matters

Employment claims average $160,000 to defend and settle. EPLI covers defense costs, settlements, and judgments.

Fiduciary Liability Insurance

Coverage

$1 million to $3 million

Protects Against:

Required If

You inherit or establish retirement plans with employee contributions.

Do small private companies really need D&O insurance?

Yes, if you have investors, board members, bank debt, or employees. D&O insurance protects personal assets when lawsuits allege mismanagement, financial reporting errors, employment violations, or breach of fiduciary duty claims excluded from general liability policies.

Common Triggers in Small Companies

Employment Claims Naming CEO:

Lender Disputes:

Regulatory Investigations:

Real-World Example

Scenario

Searcher acquires 45-employee manufacturing company without D&O insurance. Two months post-close, terminated plant manager files discrimination lawsuit naming CEO personally.

Defense Cost

$175,000

Settlement

$225,000

Total

$400,000 out of pocket

With D&O

Insurer pays defense costs and settlement. CEO’s personal assets protected.

Cost of Coverage

$4,200 annually

What is the minimum insurance program for Day 1 after closing?

The minimum Day 1 insurance program includes: General Liability, Workers’ Compensation, Commercial Auto (if vehicles), Property (if real estate/inventory), EPLI, Cyber, and Umbrella coverage ensuring lender compliance and personal CEO protection simultaneously.

The Day 1 Stack

Operational Foundation (Lender-Required):

CEO Protection (Non-Negotiable):

What insurance can wait 60 to 90 days after closing?

Pollution Liability, Product Recall, enhanced Cyber limits, and specialty coverages can typically phase in 60 to 90 days post-close if no immediate exposure exists but never delay coverage required by contracts, lenders, or regulatory compliance.

Reasonable Phase-In (60 to 90 Days)

Specialty Coverages (If Low/No Exposure):

NEVER Delay These Coverages

How do I avoid coverage gaps when transitioning from the seller’s insurance?

To avoid gaps, bind new policies effective at closing (not after), negotiate retro dates on claims-made policies to cover pre-close acts, obtain 60-day loss run updates before binding, and confirm all seller policies cancel at closing to prevent coverage disputes.

Critical Claims-Made Issues

Claims-made policies only cover claims made DURING the policy period for acts that occurred AFTER the retroactive date. Here’s a common gap scenario:

Example Situation:

Protection Options:

Typical Cost Impact

Prior acts coverage often adds 10% to 40% to premium, while tail coverage typically costs 200% to 300% of annual premium. Your broker can help you evaluate which option makes most sense for your situation.

Tail Coverage Consideration

What Is Tail Coverage?

Extended reporting period for claims-made policies. Allows claims to be reported after policy expires for acts that occurred during policy period.

Cost

200% to 300% of annual premium

Protection Strategy:

What does search fund insurance cost, and what drives the price?

Search fund insurance typically ranges from $15,000 to $150,000+ annually depending on industry, revenue, employee count, and risk profile, with service businesses (low physical risk) often at the lower end and manufacturing/logistics/construction operations at the higher end.

Understanding what business insurance costs helps you budget accurately during LOI negotiations and avoid post-close surprises. These are ballpark ranges based on typical market conditions.

Typical Cost Ranges by Business Type

Primary Cost Drivers

Revenue & Employees:

Industry & Operations:

Loss History:

Geography:

Controls & Safety:

Cost Control Strategies

Timing Your Purchase:

Strategic Deductibles:

Program Design:

Want an accurate number for your specific deal?

We’ll give you a price based on what you’re buying.

What documents do I need to get accurate insurance quotes quickly?

Essential documents include: 5-year loss runs (all coverages), current policy declarations, business description with revenue projections, employee count by classification, vehicle list with driver information, property schedules, and signed applications.

Document Checklist

From Seller:

Business Information:

Operations Data:

Target Timeline: Allow 30 to 45 days for complete quote process from initial submission to binding.

What are the industry-specific insurance landmines that derail search fund deals?

Industry-specific insurance issues that surprise searchers include: restaurant liquor liability and assault and battery exclusions, construction additional insured requirements and high GL limits, manufacturing product liability and recall exposure, healthcare professional liability tail costs, and logistics fleet driver qualification gaps.

Common Industry Landmines

Restaurants/Bars:

Construction:

Manufacturing:

Healthcare:

Distribution/Logistics:

Technology/SaaS:

How to Navigate Industry-Specific Issues

During Due Diligence:

At LOI:

What questions should I ask my broker to avoid buying the wrong coverage?

Critical broker questions include: (1) What’s your timeline to bind at close? (2) How many search fund deals have you completed? (3) Which claims-made policies need prior acts coverage? (4) Are defense costs inside or outside limits? and (5) What’s your lender COI turnaround time?

Essential Questions

Timing & Process:

Coverage Design:

Experience:

Lender Coordination:

What’s the step-by-step plan to get lender-ready coverage without slowing my deal?

Start insurance 60 to 90 days before close: (1) Week 1-2 assess current program and gather documents, (2) Week 3-4 design coverage and market competitively, (3) Week 5-6 bind policies with closing-date effective dates, (4) Post-close optimize based on operations.

90-Day Timeline

What Slows Deals Down

Can The Coyle Group help if I’m already in due diligence or close to closing?

Yes. We’ve guided dozens of search fund buyers through insurance due diligence and Day 1 coverage. Starting early produces better pricing, but we can work with your timeline whether you’re 90 days out or 2 weeks from close.

How We Help

We guide you through the entire insurance process for your acquisition:

Our Search Fund Experience

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

Questions about search fund Insurance?

Ready to get lender-ready insurance for your search fund acquisition?

The path to a successful close

Start early, identify gaps during diligence, bind comprehensive coverage that protects both the business and you personally.

The path to problems

Wait until the last minute, discover coverage gaps at closing, face personal liability exposure without D&O/EPLI protection.

Get your insurance due diligence assessment.

No cost. No obligation. Just clarity on what the deal really costs and where the landmines hide.

Use our assessment to improve your LOI negotiations. Identify deal-breakers before you’re committed. Budget accurate post-close insurance costs. No commitment required.

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping search fund buyers and private equity groups conduct insurance due diligence and structure comprehensive programs that protect operations and personal assets post-acquisition.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

Protecting Non-Profit Board Members with D&O Insurance

Rippling PEO Review: EPLI Coverage Risks Explained

The Ultimate Guide to D&O Insurance: Everything You Need to Know in 2025