Cyber Insurance Cost Calculator

Why Fast Quotes Can Cost You More Than They Save

How To Get The Best Cyber Insurance Cost Calculator: Fast, Easy, and Totally Wrong

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

Executive Summary

Your search for a cyber insurance cost calculator just brought you here. You want quick answers, a ballpark number, maybe even an instant quote. I get it. You’re busy running a business, and the idea of plugging in a few details to get pricing sounds perfect.

But here’s what 40+ years in commercial insurance has taught me: those calculators promising instant quotes? They’re giving you speed at the expense of accuracy. And in cyber insurance, that gap between the calculator’s number and your actual protection needs can be catastrophic.

At The Coyle Group, we’ve seen businesses devastated not because they lacked cyber insurance, but because they trusted an online calculator that underestimated their real exposure by a wide margin.

TL;DR – The Bottom Line

Investment range

$1,000 to $7,500 annually for most SMBs, but inadequate coverage can leave you exposed to six-figure losses

Why Business Owners Love Online Calculators (And Why That’s the Problem)

Business owners want speed, simplicity, and anonymity when shopping for cyber insurance. That’s completely understandable. You’ve got fires to put out and decisions to make every minute of the day. When a calculator promises a quick quote in just three minutes, it sounds like exactly what you need.

Plug in annual revenue, employee count, maybe your industry. Click submit. Get a number. Done.

The Hidden Problems With Online Quotes

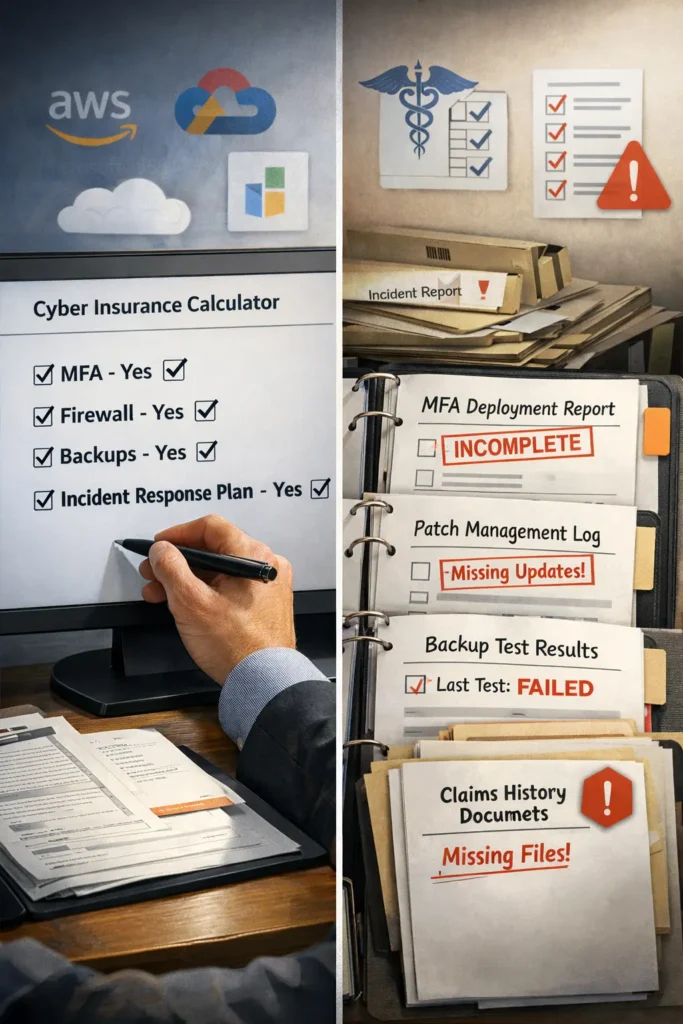

Here’s the consequence nobody mentions: what you get back is often not what you really need. A calculator gives you a number, but it doesn’t think for you or advise you on what limits you need, what sublimits matter for your specific operations, or what endorsements and options protect you from the threats you actually face.

More importantly, it doesn’t give you options. Just one carrier’s quote, designed to make buying from them fast and easy while preventing you from exploring potentially better solutions.

There’s no nuance, no strategy, and like I said, no options. Just a number that’s often inaccurate once you go through actual underwriting.

What 40+ Years Taught Me About This Risk

In four decades of insuring businesses, I’ve seen how a single overlooked exposure can devastate an otherwise thriving operation. The businesses that avoid catastrophic losses treat insurance decisions strategically, not transactionally.

Successful business owners understand that cyber insurance isn’t about finding the cheapest quote online. It’s about building protection that evolves with your actual risk profile. That requires expertise, not automation.

How Google Rankings Bias Your Options

Many top-ranking cyber insurance cost calculators are owned by carriers and are designed to produce one fast, purchase-ready option. That’s convenient, but it’s not the same as comparing multiple carriers and customizing coverage to your risk profile, industry requirements, and actual claims exposure.

Small businesses typically pay between $1,000 and $7,500 annually for cyber insurance, with significant variation based on industry risk, data sensitivity, and security controls. According to IBM’s 2024 Cost of a Data Breach Report, the global average breach cost reached $4.88 million, highlighting why proper coverage is essential rather than just seeking the cheapest quote.

The Real Cost of Cyber Insurance

Let’s establish baseline expectations. Small businesses pay an average of $145 per month, or about $1,740 annually, for cyber insurance coverage. But that’s just the median, and medians hide significant variation. Industry, data sensitivity, security controls, and claims history can push your actual premium 2x–5x above or below the median, which is why the table below shows ranges, not a single number.

Actual Cost Ranges by Business Size

Key Factors Calculators Can’t Accurately Assess

Industry Risk Profile

Healthcare, financial services, and technology companies face higher premiums due to sensitive data handling. The Health Insurance Portability and Accountability Act (HIPAA) creates substantial liability for medical data breaches, with penalties reaching $1.5 million annually per violation category.

Security Posture

Calculators ask if you have MFA or backups, but they can’t verify documentation. According to industry analysis, approximately 40% of cyber insurance claims are denied, often due to misrepresentation of security controls like multi-factor authentication. Simply checking a box doesn’t prove you have the controls insurers require.

Data Sensitivity

The type of data you handle matters more than the volume. Social Security numbers, financial records, and protected health information each carry different risk weights that calculators oversimplify.

Claims History

Past claims significantly impact premiums, but calculators can’t access this information. A single prior incident can increase rates by 20-40%, a detail you’ll only discover during actual underwriting.

Geographic Factors

State regulations, data protection laws, and regional cybercrime rates affect pricing. California businesses face different requirements than Texas operations, but calculators rarely account for this complexity.

What Calculators Miss: The $200,000 Gap

Here’s the sobering reality: most small businesses buy $1M per-occurrence / $1M aggregate cyber limits. According to IBM’s 2024 Cost of a Data Breach Report, breach costs continue to rise, but the real issue isn’t the average cost per record. It’s how fast response and defense expenses erode your limits before claims even resolve.

Reality check: even with a few thousand records, total breach impact can climb fast. Notification, credit monitoring, legal counsel, forensic investigation, and downtime alone can push losses into the hundreds of thousands, before you factor in extortion demands, lawsuits, or regulatory scrutiny.

True Breach Cost Breakdown

The FBI’s 2024 IC3 Report documented 859,532 complaints with losses exceeding $16.6 billion. Business Email Compromise alone accounted for $2.77 billion in reported losses.

This is why many businesses treat $1M as a floor, not a finish line, because the limit gets eaten by defense costs and response expenses long before the story is over.

Understanding what cyber insurance actually covers helps you recognize when calculator recommendations fall short.

See whether your limits and sublimits actually match your exposure.

Real-World Example: The $300,000 Surprise

Take a 25-person tech firm. They used a popular cyber insurance cost calculator and were thrilled to see a quote for just $2,500 annually. The policy seemed comprehensive at first glance.

But here’s what the calculator didn’t reveal:

Six months later, they were hit with a ransomware attack. Total damages: $312,000. Insurance recovery: $98,000. Out-of-pocket loss: $214,000.

The Broker Solution: Better Coverage, Minimal Cost Difference

Compare that to a client I worked with. Same size, same industry, similar risk profile. We found a broader policy with better coverage, lower deductibles, and no critical exclusions.

That’s the power of advice over automation.

The Calculator’s Biggest Blind Spots

Online calculators ask simple yes/no questions, but underwriters verify documentation. The three areas below are where calculators consistently fail, and where most claim disputes originate.

Security Control Documentation

Calculators ask if you have multi-factor authentication. But do you have it deployed across all systems? Can you prove it? Do you have documentation showing implementation dates and coverage percentages?

According to Microsoft security research, MFA blocks 99.9% of automated account attacks. Yet many businesses check “yes” on calculator forms while having MFA on only 30% of accounts.

Required security controls for 2025 coverage:

MoneyGeek’s 2025 cyber insurance requirements guide notes that 82% of denied claims involved organizations without proper MFA documentation.

Industry-Specific Requirements

Healthcare organizations face HIPAA compliance requirements that standard calculators don’t address. Financial services firms need specific coverage for SEC regulatory response. Technology companies require errors and omissions coverage integrated with cyber policies.

Calculators use generic industry dropdowns, but they can’t assess your specific regulatory environment.

Third-Party Risk

Do you use cloud services? Payment processors? Managed service providers? Each vendor relationship creates potential liability that calculators can’t evaluate.

The 2024 IC3 Report from the FBI showed that supply chain compromises and third-party breaches were among the fastest-growing attack vectors, yet calculators rarely ask detailed vendor questions.

Claims History Details

Have you had cyber incidents that didn’t result in insurance claims? Near-misses? Security events that you resolved internally? This history affects underwriting, but calculators can’t access it.

A clean claims record typically qualifies for preferred rates with 15-25% discounts, but you need to prove it through proper documentation, not just checking boxes.

The Cost of Getting It Wrong

Let’s talk about what inadequate cyber insurance actually costs businesses. Not the premium you pay, but the exposure you carry when your policy doesn’t match your risk. The three scenarios below are composite examples from real claims, each started with a calculator quote that looked reasonable on paper.

Scenario 1: The Underinsured Manufacturer

Manufacturing companies face unique cyber risks that generic calculators can’t properly assess. Operational technology vulnerabilities, supply chain complexity, and intellectual property exposure create layered risks.

Scenario 2: The Professional Services Firm

Scenario 3: The Healthcare Practice

These aren’t theoretical scenarios. These are composite examples based on real claims I’ve handled over four decades.

No calculators. No pressure. Just a clear view of your coverage options.

Investment Fraud: The Fastest-Growing Cyber Threat

Most calculators focus on ransomware and data breaches, the two threats they’re built to protect against. Investment fraud, AI-enabled social engineering, and supply chain attacks fall outside their models entirely, yet they now account for the majority of dollar losses.

According to the FBI’s 2024 IC3 Report, investment fraud, particularly involving cryptocurrency, generated $6.5 billion in victim losses, the highest loss category. People over 60 suffered nearly $5 billion in losses across all cybercrime categories.

While calculators focus on traditional cyber risks like ransomware and data breaches, they rarely address emerging threats like:

The cyber threat landscape evolves faster than calculator algorithms can adapt.

The Cyber Insurance Market Reality

The cyber insurance market has stabilized after significant volatility in 2021-2022. Premiums moderated in 2024-2025, with some sectors seeing flat or even decreased rates for businesses with strong security controls. Businesses that documented strong controls in 2023–2024 are now seeing competitive options that weren’t available two years ago, but only if they know how to position their risk properly.

Market conditions that favor prepared businesses:

But only for businesses that can demonstrate:

Calculators can’t help you navigate this market. They can only show you one carrier’s standard offering.

How The Coyle Group Approaches Cyber Insurance The Right Way

We don’t process quotes. We assess risk. When clients come to us for cyber insurance, we start with understanding your operations, not plugging numbers into a calculator.

Our Process Is Simple But Thorough

Understanding the difference between first-party and third-party cyber coverage is essential for evaluating whether any proposal truly protects your business. Many calculators don’t properly distinguish between these coverage types, leading to gaps that only become apparent after a claim.

Why This Matters

Calculators show you one carrier’s price. We show you your best options across multiple markets, including carriers that specialize in your industry, whether that’s healthcare, financial services, technology, manufacturing, or professional services.

The process doesn’t have to be painful. With just a few pieces of information, we can start the conversation. No endless forms, no pressure, and no obligation.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

Questions about Cyber Insurance Cost Calculators?

Taking Control of Your Cyber Insurance Decision

Your cyber insurance is too important to trust to an algorithm. Online calculators serve the insurance company’s efficiency goals, not your protection needs.

Strategic cyber insurance requires:

Why Work With The Coyle Group

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US, solving their insurance challenges. Gordon specializes in helping businesses develop comprehensive cyber insurance programs that protect their operations and support their growth objectives.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

The Crowdstrike Debacle and Cyber Insurance

Tech E&O vs. Cyber Insurance: What You Need to Know

First Party vs Third Party Cyber Insurance: What’s Covered, What’s Missing, and What You Actually Need