What Is Search Fund D&O Insurance and How Do You Get It Right?

Protect Yourself Before and After the Deal Closes

Search Fund D&O Insurance: What You Need To Know

Index

Gordon B. Coyle

CEO, The Coyle Group

845-474-2924

How to get started

If you are buying a business through a search fund or ETA model, you are about to become the CEO of a company you did not build. That means you are inheriting its risks, its people, and its past decisions. And if a board member, investor, or employee decides to point the finger at you, your personal assets are on the line unless you have the right protection in place.

That protection starts with search fund D&O insurance.

TL;DR. Executive summary

Search fund D&O insurance is a Directors and Officers liability policy that shields searchers, board members, and acquired company officers from personal financial loss if a claim alleges mismanagement, breach of fiduciary duty, or wrongful acts.

The Coyle Group has structured search fund D&O programs for ETA buyers from search phase through post-close. Everything in this article reflects what 40-plus years of placement experience looks like in practice, not theory.

The search fund model and the broader ETA (Entrepreneurship Through Acquisition) model share the same core D&O risk: a new CEO steps into a leadership role at an established business, inherits its history, and immediately becomes personally accountable for every decision going forward. Whether you raised capital from a group of search fund investors or structured a self-funded ETA deal, the liability exposure is real from day one.

Search fund D&O insurance is the mechanism that keeps that exposure from becoming a personal financial catastrophe.

What Is Search Fund D&O Insurance and Why Does It Matter to Searchers?

Search fund D&O insurance is a Directors and Officers liability policy built for the unique risk profile of a search fund or ETA acquisition. It protects the searcher, investor board members, and any officers of the acquired company from personal financial loss when a claim alleges mismanagement, breach of fiduciary duty, or other wrongful acts in their capacity as leaders. It is not a business policy. It is personal protection for the people running the business.

When you form a search fund, you immediately take on a board of investors. Those investors are relying on your decisions. If a deal falls through, if a target company feels misled during due diligence, or if an investor believes you breached your fiduciary duty during the search process, they can come after you personally. No LLC structure fully shields you from that. Search fund D&O insurance is what does.

In the insurance by industry world, search funds sit in a unique position because the exposure changes dramatically across two distinct phases: the search phase and the post-acquisition operating phase. A policy that works for one may leave you exposed in the other. Getting this right from the start is what separates searchers who close deals confidently from those who scramble at the last minute because an investor or lender demands proof of coverage.

The key benefits of search fund D&O insurance:

With The Coyle Group to get search fund D&O insurance reviewed by an expert who has structured coverage for searchers at every stage.

When Should You Get Search Fund D&O Coverage: Search Phase or Post-Acquisition?

You need search fund D&O insurance in two phases, and they are not the same policy. During the search phase, coverage should be in place as soon as you have investors on your board. Post-acquisition, the policy must be restructured to reflect the acquired company’s size, industry, employee count, and specific risk profile. Waiting until after close to think about D&O is one of the most common and costly mistakes searchers make.

Here is why timing matters so much.

During the Search Phase:

At the Acquisition Close:

After the Acquisition (Operating Phase):

The biggest gap searchers create is treating D&O as a one-time purchase at close. The right approach is to structure coverage for the search phase first, then rebuild the policy around the acquired business as part of your post-close insurance stack.

What Does Search Fund D&O Insurance Actually Cover?

Search fund D&O insurance covers personal liability of directors and officers for claims alleging wrongful acts in their management capacity. This includes fiduciary duty breaches, misrepresentation, failure to supervise, errors in business judgment, and employment-related wrongful acts when EPLI is bundled in. It pays defense costs, settlements, and judgments up to the policy limit, shielding personal assets from covered claims.

The three coverage parts you need to understand:

Side A (Individual Coverage):

Side B (Company Reimbursement):

Side C (Entity Coverage):

What is typically covered:

What is typically excluded:

Not sure if your current policy has Side A? Contact us, and we will review your coverage at no charge.

What Are the Biggest D&O Coverage Gaps for Search Fund CEOs?

The most dangerous D&O gaps for search fund CEOs are claims-made timing gaps, missing tail coverage at acquisition close, absent EPLI bundling, and no Side A protection for individual board members. These four gaps can leave a CEO personally liable for six-figure claims that a properly structured search fund D&O insurance policy would have fully absorbed.

In my experience, most searchers who face personal liability exposure did not have a bad insurance broker. They had a broker who did not understand the search fund model and applied a standard small business D&O framework to a structure that demands something different.

Here is where the gaps stack up:

1. Claims-Made Timing Gaps

D&O policies are claims-made, not occurrence-based. As the D&O Diary documents across hundreds of case studies, coverage only applies when the claim is made during the active policy period, not when the act occurred. If you buy a business in January and an employee files a discrimination claim in November for conduct that happened in March (before you owned the company), you need prior acts coverage or a seller’s tail policy. Without it, you pay out of pocket.

Tail policies for sellers typically cost 200-300% of the annual premium, and they are negotiable at close. Many searchers do not know to ask.

2. No EPLI Bundling

Employment Practices Liability covers claims for discrimination, harassment, wrongful termination, and wage disputes. These are among the most common claims a new CEO faces in the first 12-24 months post-acquisition. Lenders do not require EPLI. They require GL, workers compensation, and property. That leaves a gap that costs $3,000-$15,000 per year to fill but can result in $160,000-$400,000 in defense and settlement costs if left open.

3. Missing Investor-Side Side A Protection

If your investor board members do not have Side A coverage in the policy, they will decline board service or pull back from active involvement. This is a real deal-risk that surfaces during the capital raise. Confirm that Side A is explicitly included and that limits are sufficient relative to your investor profile.

4. Lender Minimums as the Coverage Standard

Lenders set minimum requirements based on their collateral protection, not your personal protection. Meeting lender minimums on GL, property, and workers compensation does not mean you are covered. D&O, EPLI, cyber, and fiduciary liability are all outside standard lender checklists. Structure your policy around your actual exposure, not the lender’s minimum checklist.

Real-World Example: What No D&O Looks Like

A searcher closed on a service business and skipped D&O during the search phase to save on premiums. Eight months post-close, a former employee filed a discrimination lawsuit. Without D&O or EPLI in place, the searcher paid $400,000 out of pocket in legal defense and settlement costs. A properly structured search fund D&O insurance policy with EPLI bundled in would have been $4,200-$6,000 per year. The math is not close.

How Much Does Search Fund D&O Insurance Cost?

Search fund D&O insurance costs between $12,000 and $25,000 annually during the search phase for a $5 million limit, and $3,000 to $15,000 per year post-acquisition for small businesses, depending on industry, revenue, and employee count. Total annual insurance spend for a search fund across all required coverages typically ranges from $15,000 to $150,000-plus, driven primarily by the acquired company’s risk profile.

Here is a breakdown by phase:

Phase |

Typical D&O Limit |

Annual Premium Range |

Key Driver |

|---|---|---|---|

|

Search Phase |

$1M – $5M |

$12,000 – $25,000 |

Investor count, entity structure |

|

Post-Acquisition (small biz) |

$1M – $5M |

$3,000 – $15,000 |

Revenue, employee count, industry |

|

Post-Acquisition (mid-market) |

$5M – $10M |

$15,000 – $40,000+ |

Revenue, litigation exposure, industry |

|

Seller Tail Policy |

N/A |

200-300% of annual D&O premium |

Policy limit, retroactive date |

Factors that move the needle on your premium:

To get a phased D&O cost estimate built around your specific search fund structure and target industry.

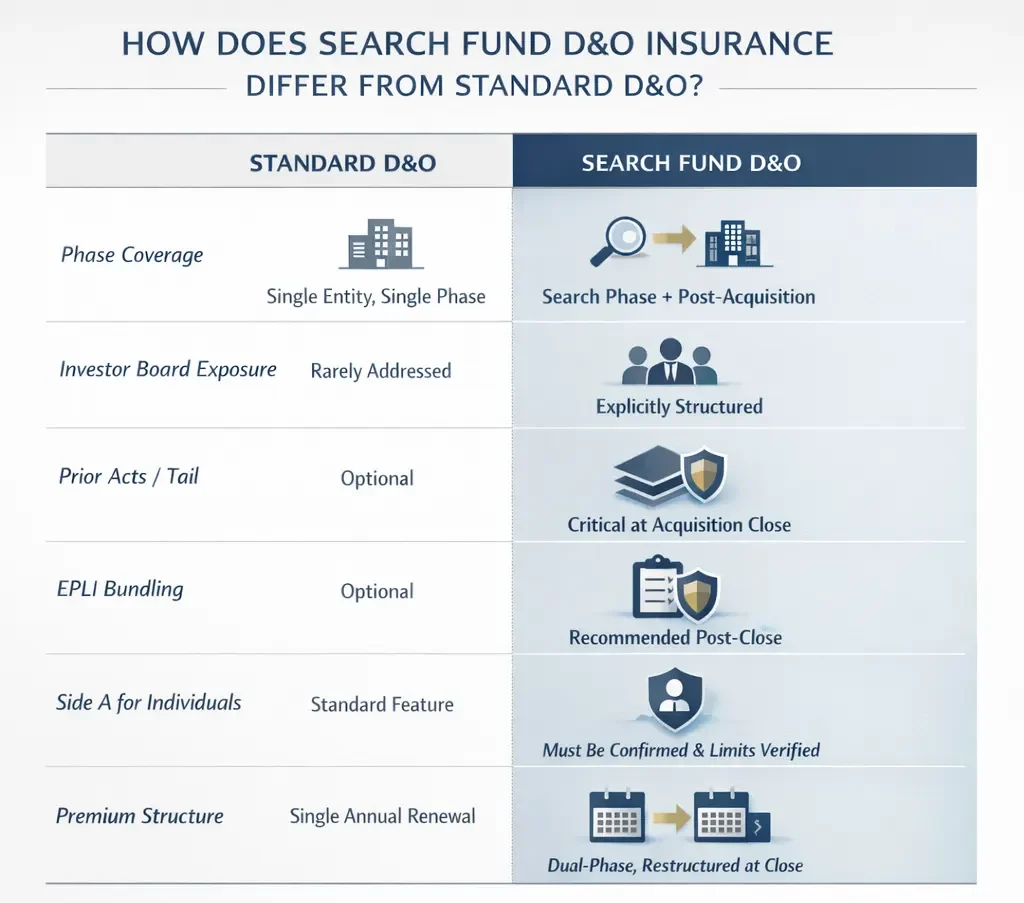

How Does Search Fund D&O Insurance Differ from Standard D&O?

Standard D&O insurance is built for operating companies with established leadership, defined revenue, and known claim history. Search fund D&O insurance addresses a two-phase structure where the insured entity changes at acquisition, the leadership is brand new, and the risk profile shifts significantly between the search and operating phases. Standard policies applied to search funds routinely miss phase-transition gaps, tail coverage needs, and the investor board liability exposure unique to the search model.

The table below shows the key structural differences:

Feature |

Standard D&O |

Search Fund D&O |

|---|---|---|

|

Phase coverage |

Single entity, single phase |

Search phase plus post-acquisition |

|

Investor board exposure |

Rarely addressed |

Explicitly structured |

|

Prior acts / tail |

Optional |

Critical at acquisition close |

|

EPLI bundling |

Optional |

Recommended at post-close |

|

Side A for individuals |

Standard |

Must confirm and verify limits |

|

Premium structure |

Single annual renewal |

Dual-phase, restructured at close |

The insurance by coverage considerations for a search fund go well beyond D&O alone. A complete risk stack for an ETA buyer also includes general liability, commercial property, workers compensation, cyber liability, fiduciary liability, and key person life insurance. D&O is the most personal of those protections, and also the most frequently misunderstood.

Working with a broker who specializes in the search fund and ETA market is not optional. The nuances of phase-transition coverage, tail negotiation at close, and investor board structuring require someone who has done this before. A generalist broker applying a standard SMB D&O template to your search fund will miss things that cost you later.

What 40+ years in commercial insurance has taught me is that search fund buyers consistently underestimate how different their risk profile is from a traditional business owner. A traditional SMB owner built the company and knows its history. A searcher buys into an existing risk profile on day one. The right search fund D&O insurance policy accounts for that distinction explicitly. It does not assume continuity. It builds in protection for the transition itself.

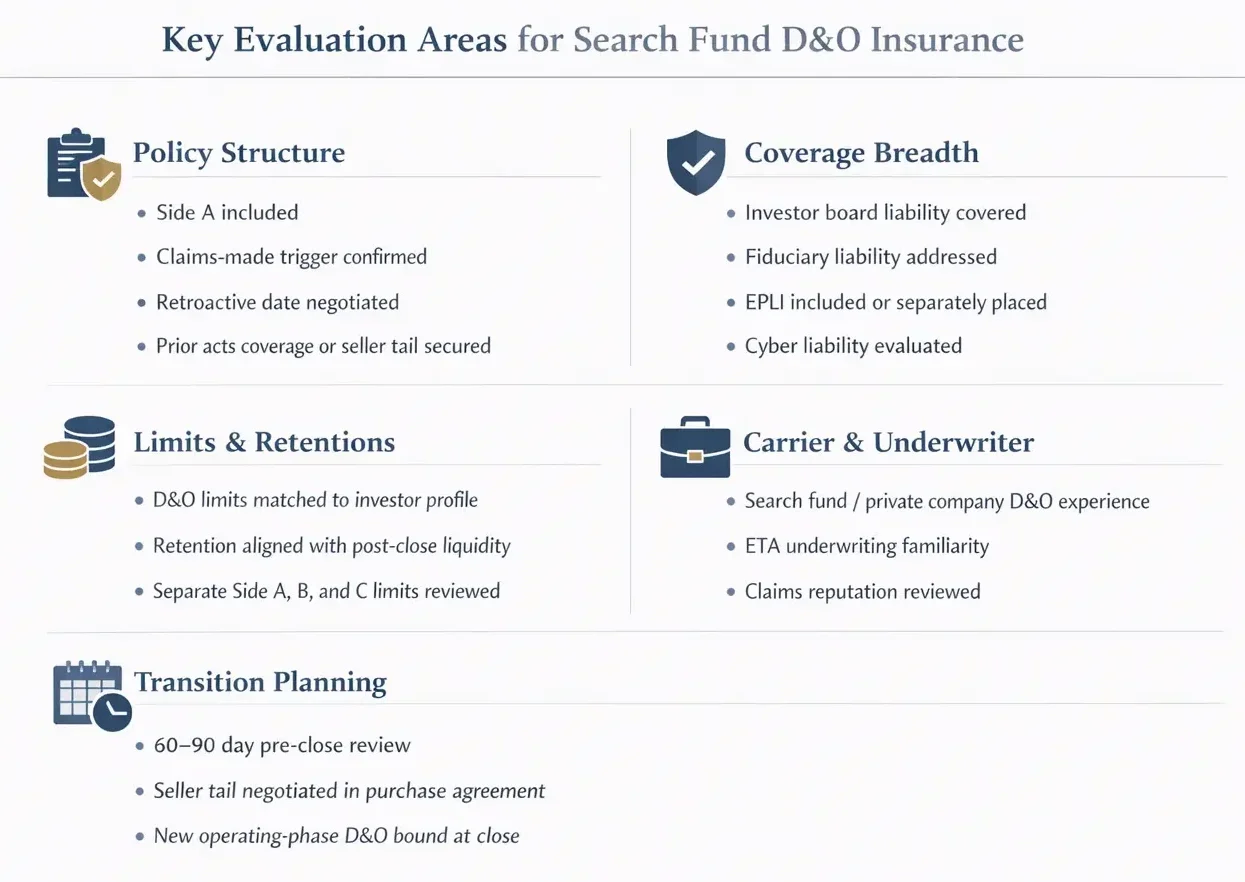

What Should You Look for When Buying a Search Fund D&O Policy?

When buying search fund D&O insurance, confirm five things before binding: Side A is explicitly included, the policy covers investor board liability during the search phase, prior acts coverage or a seller tail is secured at close, EPLI is in place post-acquisition, and policy limits reflect your investor profile rather than a generic small business minimum.

Here is the full evaluation checklist:

Policy Structure:

Coverage Breadth:

Limits and Retentions:

Carrier and Underwriter:

Transition Planning:

The Coyle Group has structured search fund D&O insurance for buyers at every stage of the ETA process. Contact us to get a coverage review before your next deal.

What Does a Complete Search Fund Insurance Stack Look Like?

Search fund D&O insurance is the most personal coverage in your risk stack, but it does not stand alone. A complete search fund insurance program addresses entity-level and individual-level exposures across every phase of the deal. Buying only what lenders require leaves significant gaps that personal assets will fill if a claim hits.

Here is what a properly structured post-acquisition stack looks like for a typical search fund acquisition:

Coverage |

What It Covers |

Required By |

|---|---|---|

|

D&O with EPLI |

Personal liability for management decisions, employment claims |

Investors, lenders (increasingly) |

|

General Liability |

Third-party bodily injury and property damage |

Lenders, landlords |

|

Commercial Property |

Physical assets, equipment, inventory |

Lenders |

|

Employee injury and lost wages |

State law |

|

|

Data breaches, ransomware, tech failures |

Best practice |

|

|

401(k) and benefit plan mismanagement |

Recommended with any retirement plan |

|

|

Key Person Life |

Revenue and loan protection if CEO is lost |

SBA and some lenders |

Search fund D&O insurance belongs at the top of that list, not as an afterthought. It is the only coverage in the stack that protects you personally, not just the business entity. Every other line on this table protects the company or satisfies a lender. D&O with EPLI protects you.

When building your post-close stack, start with D&O and work outward. The coverages that follow from it (EPLI, fiduciary, cyber) should be sized and structured in relation to your D&O limits and retentions, not in isolation. A well-built search fund insurance program reads as a coherent system, not a collection of individual policies grabbed from different brokers.

Contact us to get a complete search fund insurance stack review, from D&O to cyber to key person coverage, before you close.

Questions About Search Fund D&O Insurance?

Get the Right Search Fund D&O Coverage

The Coyle Group has been structuring commercial insurance programs for business owners for over 40 years. Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, built this practice around one belief: business owners deserve the same clarity and rigor in their insurance decisions that they apply to every other part of their business.

When it comes to search fund D&O insurance, we understand that the risk profile of an ETA buyer is unlike any other client. You are inheriting an unknown history, leading a company you did not build, and managing investor relationships from day one. We structure coverage that accounts for all of it, across both phases of your deal.

Whether you are still in the search phase or preparing to close, the time to build your coverage stack is now. We work directly with your legal and financial advisors to ensure your D&O, EPLI, and full insurance program are in place before you need them.

95+

Years of Family Legacy in Insurance

40+

Years Personal Experience

95%

Client Retention Rate

600+

Educational Videos

This article was written by Gordon B. Coyle, CPCU, ARM, AMIM, PWCA, CEO of The Coyle Group, who has over 40 years of experience working with business owners of all sizes and industries across the US. Gordon specializes in helping search fund buyers and ETA entrepreneurs structure insurance programs that protect them personally and operationally, from the first investor conversation through post-close operations.

Here’s how to take the next step

Schedule Your Insurance Confidence Assessment

In our 30-minute call, you’ll discover:

Not ready for a call?

Get Free Access to Our Gated Video:

“How to Finally Feel Confident in Your Coverage. “

And discover the exact system we use to help business owners eliminate hidden coverage gaps, stop overpaying, and finally feel confident in their protection.

What Peace of Mind Looks Like

Trusted by business owners across the U.S.

The Coyle Group is 1st class! Gordon and his team are knowledgeable, responsive, and attentive to detail. Gordon is that rare breed of professional who genuinely cares for his clients and works hard to exceed their expectations. I highly recommend them.

The insurance brokerage service was truly tailored to my needs, nothing like those big brokers who steer you toward random policies that don’t fit your profile. Thank you to the team for your help.

I was working with another broker and having difficulty acquiring General Liability coverage. A colleague recommended The Coyle Group. They were able to get coverage bound in just a couple of business days and a policy issued in ten days, and with a solid carrier at a competitive premium. Truly impressive results, plus it was a pleasure working with them. I highly recommend the Coyle Group!

If any business is looking to work with an insurance brokerage firm that is not only excellent at what the firm does, but one that deeply values the needs of the clients, then The Coyle Group is the firm for you. Give them a call and see for yourself. I can assure that you will quickly agree.

Want to know more?

See related blogs

Protecting Non-Profit Board Members with D&O Insurance

Rippling PEO Review: EPLI Coverage Risks Explained

The Ultimate Guide to D&O Insurance: Everything You Need to Know in 2025